Stock Analysis

- South Korea

- /

- General Merchandise and Department Stores

- /

- KOSE:A057050

Hyundai Home Shopping Network Corporation (KRX:057050) Surges 28% Yet Its Low P/E Is No Reason For Excitement

Hyundai Home Shopping Network Corporation (KRX:057050) shares have continued their recent momentum with a 28% gain in the last month alone. Looking further back, the 22% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

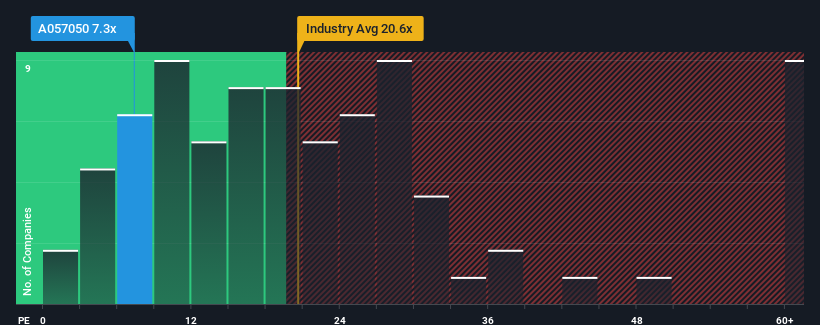

Even after such a large jump in price, Hyundai Home Shopping Network's price-to-earnings (or "P/E") ratio of 7.3x might still make it look like a buy right now compared to the market in Korea, where around half of the companies have P/E ratios above 14x and even P/E's above 27x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Hyundai Home Shopping Network certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Hyundai Home Shopping Network

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Hyundai Home Shopping Network would need to produce sluggish growth that's trailing the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 63% last year. However, this wasn't enough as the latest three year period has seen a very unpleasant 28% drop in EPS in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 7.3% per annum during the coming three years according to the three analysts following the company. That's shaping up to be materially lower than the 19% each year growth forecast for the broader market.

In light of this, it's understandable that Hyundai Home Shopping Network's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Hyundai Home Shopping Network's P/E?

Despite Hyundai Home Shopping Network's shares building up a head of steam, its P/E still lags most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Hyundai Home Shopping Network's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for Hyundai Home Shopping Network that you should be aware of.

You might be able to find a better investment than Hyundai Home Shopping Network. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're helping make it simple.

Find out whether Hyundai Home Shopping Network is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A057050

Hyundai Home Shopping Network

Operates an online shopping company in South Korea.

Flawless balance sheet, undervalued and pays a dividend.