- South Korea

- /

- Pharma

- /

- KOSE:A009420

Discovering 3 Stocks That May Be Priced Below Their Estimated Value

Reviewed by Simply Wall St

As global markets have recently experienced broad-based gains, with U.S. indexes approaching record highs and smaller-cap indexes outperforming large-caps, investors are keenly focused on identifying opportunities that may be undervalued amidst the positive sentiment driven by strong labor market reports and stabilizing economic indicators. In this context of cautious optimism, discerning investors often seek stocks that are priced below their estimated value, offering potential for growth as market conditions evolve.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HangzhouS MedTech (SHSE:688581) | CN¥62.11 | CN¥124.14 | 50% |

| NBT Bancorp (NasdaqGS:NBTB) | US$50.08 | US$99.93 | 49.9% |

| Truecaller (OM:TRUE B) | SEK47.98 | SEK95.84 | 49.9% |

| Nordic Waterproofing Holding (OM:NWG) | SEK172.40 | SEK344.25 | 49.9% |

| Kitron (OB:KIT) | NOK31.18 | NOK62.32 | 50% |

| Power Root Berhad (KLSE:PWROOT) | MYR1.46 | MYR2.92 | 50% |

| Intermedical Care and Lab Hospital (SET:IMH) | THB4.94 | THB9.86 | 49.9% |

| Neosperience (BIT:NSP) | €0.57 | €1.14 | 50% |

| BATM Advanced Communications (LSE:BVC) | £0.188 | £0.38 | 50% |

| Audinate Group (ASX:AD8) | A$8.79 | A$17.54 | 49.9% |

Let's uncover some gems from our specialized screener.

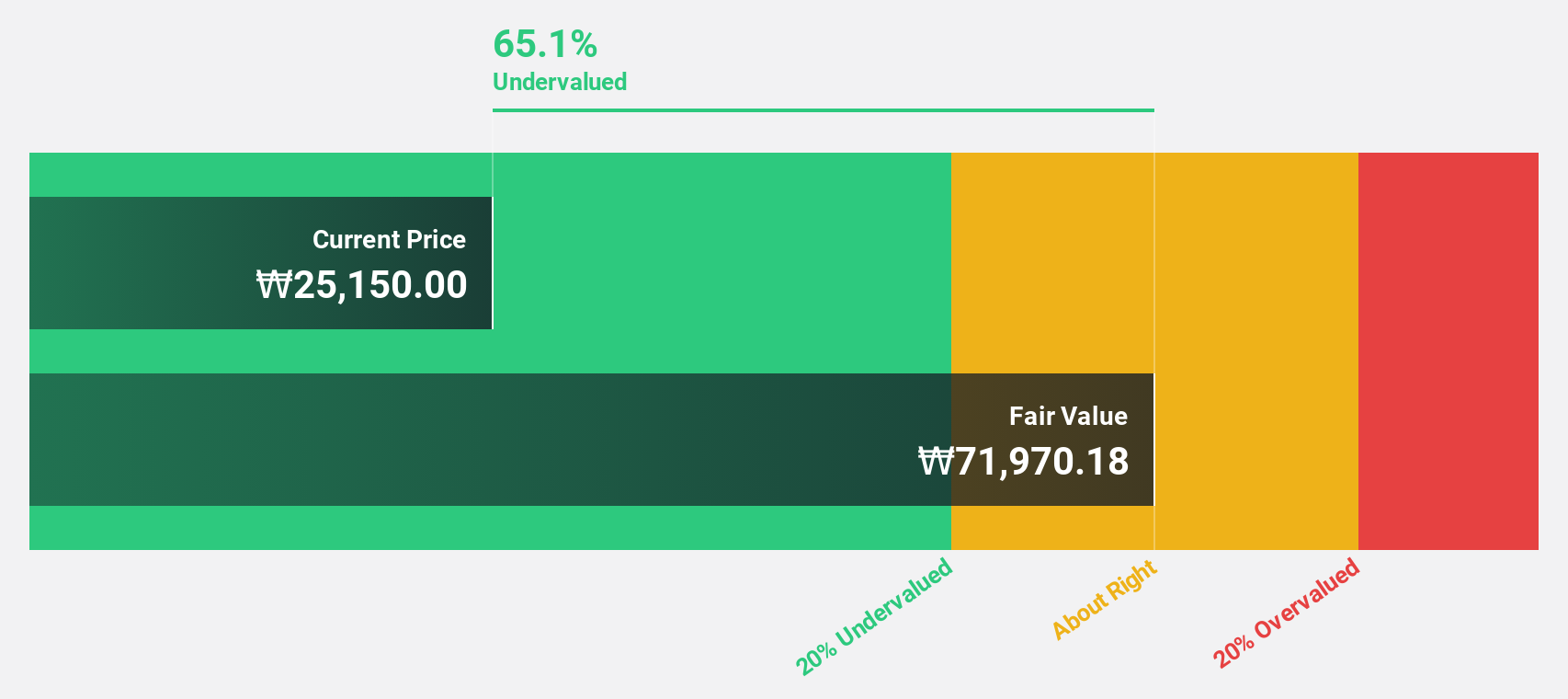

Hotel ShillaLtd (KOSE:A008770)

Overview: Hotel Shilla Co., Ltd is a hospitality company operating in South Korea and internationally, with a market capitalization of ₩1.51 trillion.

Operations: The company generates revenue primarily from its Travel Retail (TR) segment, amounting to ₩3.30 trillion, and its Hotel & Leisure Sector, Etc., contributing ₩707.79 billion.

Estimated Discount To Fair Value: 47.1%

Hotel Shilla Ltd. is trading at ₩40,050, significantly below its estimated fair value of ₩75,702.96, representing a 47.1% discount. Despite interest payments not being well covered by earnings and a forecasted low return on equity of 15.2%, the company is expected to become profitable in the next three years with earnings growing at 113.19% annually and revenue growth outpacing the Korean market at 10.9% per year.

- According our earnings growth report, there's an indication that Hotel ShillaLtd might be ready to expand.

- Unlock comprehensive insights into our analysis of Hotel ShillaLtd stock in this financial health report.

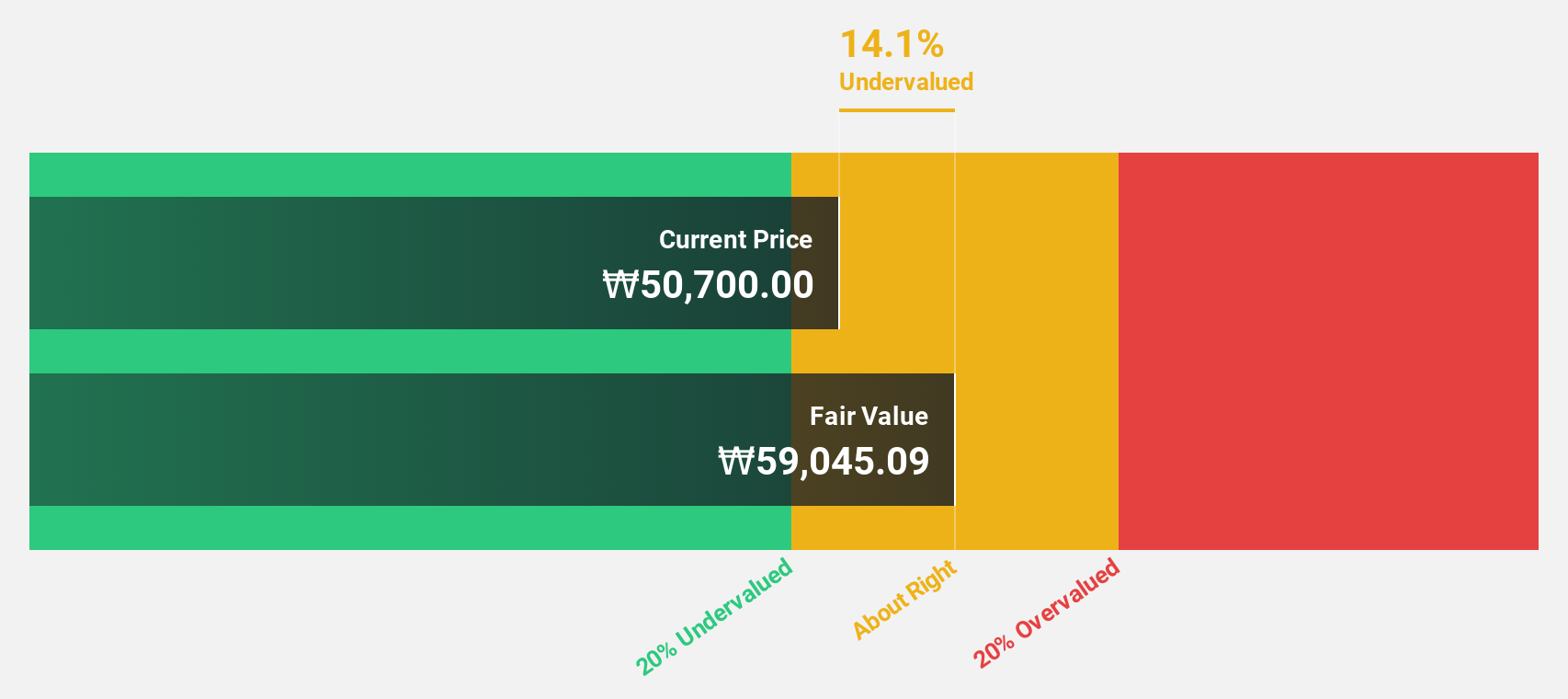

Hanall Biopharma (KOSE:A009420)

Overview: Hanall Biopharma Co., Ltd. is a pharmaceutical company that manufactures and sells pharmaceutical products both in South Korea and internationally, with a market cap of ₩1.78 trillion.

Operations: Revenue Segments (in millions of ₩):

Estimated Discount To Fair Value: 31.2%

Hanall Biopharma is trading at ₩37,150, about 31.2% below its estimated fair value of ₩54,016.97. Despite a volatile share price and a recent net loss of KRW 3,424.95 million for the first nine months of 2024, earnings are projected to grow annually by 66.79%, with revenue expected to increase by 18.1%, surpassing market growth rates in Korea. The company anticipates profitability within three years amidst ongoing clinical advancements.

- Upon reviewing our latest growth report, Hanall Biopharma's projected financial performance appears quite optimistic.

- Get an in-depth perspective on Hanall Biopharma's balance sheet by reading our health report here.

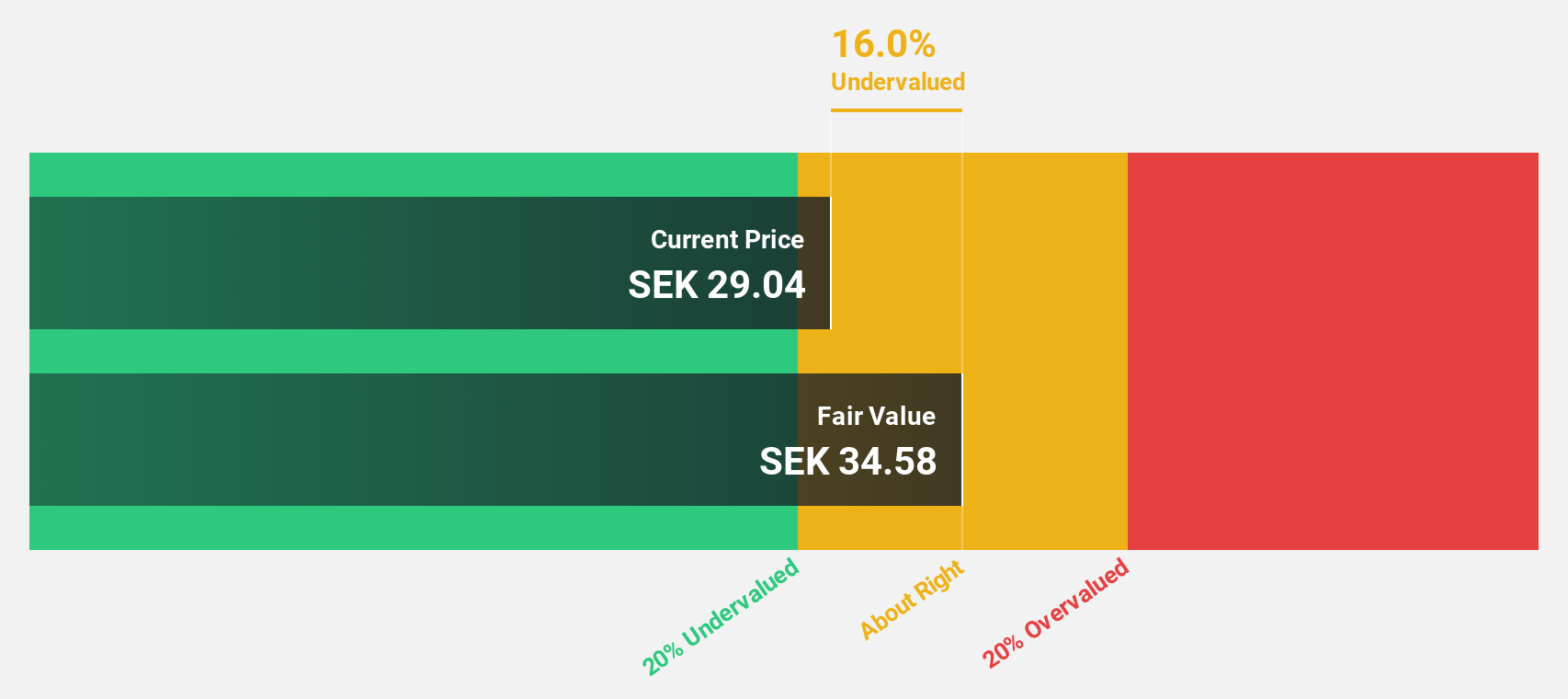

Sinch (OM:SINCH)

Overview: Sinch AB (publ) offers cloud communications services and solutions for enterprises and mobile operators across various countries, including Sweden, France, the United Kingdom, Germany, Brazil, India, Singapore, and the United States; it has a market cap of approximately SEK16.98 billion.

Operations: Sinch's revenue segments primarily consist of cloud communications services and solutions provided to enterprises and mobile operators across multiple international markets, including Sweden, France, the United Kingdom, Germany, Brazil, India, Singapore, and the United States.

Estimated Discount To Fair Value: 40.9%

Sinch is trading at SEK 20.11, significantly below its estimated fair value of SEK 34.01, representing a good relative value compared to peers. Despite recent volatility and a net loss due to impairment charges, Sinch's earnings are forecast to grow substantially by 113.16% annually, with profitability expected within three years. Recent strategic appointments and M&A intentions could bolster growth prospects as the company expands its North American market presence and enhances emergency communication technologies.

- Our expertly prepared growth report on Sinch implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of Sinch with our comprehensive financial health report here.

Where To Now?

- Click here to access our complete index of 926 Undervalued Stocks Based On Cash Flows.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanall Biopharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A009420

Hanall Biopharma

A pharmaceutical company, manufactures and sells pharmaceutical products in South Korea and internationally.

Flawless balance sheet with reasonable growth potential.