Advertisement

- South Korea

- /

- Chemicals

- /

- KOSE:A120110

Why Investors Shouldn't Be Surprised By Kolon Industries, Inc.'s (KRX:120110) Low P/S

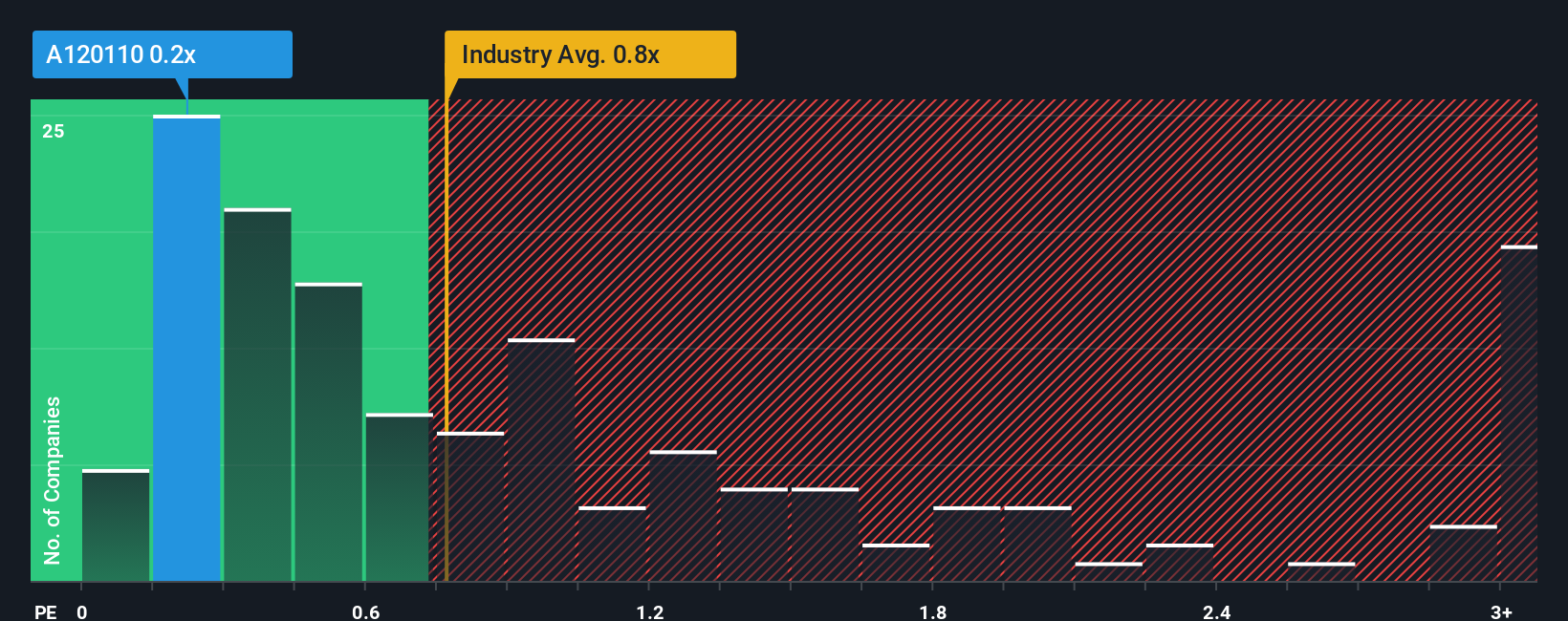

Kolon Industries, Inc.'s (KRX:120110) price-to-sales (or "P/S") ratio of 0.2x may look like a pretty appealing investment opportunity when you consider close to half the companies in the Chemicals industry in Korea have P/S ratios greater than 0.8x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Kolon Industries

What Does Kolon Industries' Recent Performance Look Like?

There hasn't been much to differentiate Kolon Industries' and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. Those who are bullish on Kolon Industries will be hoping that this isn't the case.

Keen to find out how analysts think Kolon Industries' future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Kolon Industries?

Kolon Industries' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a decent 5.2% gain to the company's revenues. Still, lamentably revenue has fallen 3.2% in aggregate from three years ago, which is disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 1.4% as estimated by the three analysts watching the company. With the industry predicted to deliver 12% growth, the company is positioned for a weaker revenue result.

With this information, we can see why Kolon Industries is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Kolon Industries maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Kolon Industries (2 are a bit unpleasant!) that you should be aware of before investing here.

If you're unsure about the strength of Kolon Industries' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Kolon Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A120110

Kolon Industries

Engages in industrial materials, chemicals, films/electronic materials, and fashion businesses in South Korea and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor