Advertisement

- South Korea

- /

- Metals and Mining

- /

- KOSE:A008970

Dong Yang Steel Pipe Co., Ltd.'s (KRX:008970) 25% Jump Shows Its Popularity With Investors

Dong Yang Steel Pipe Co., Ltd. (KRX:008970) shares have had a really impressive month, gaining 25% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 78%.

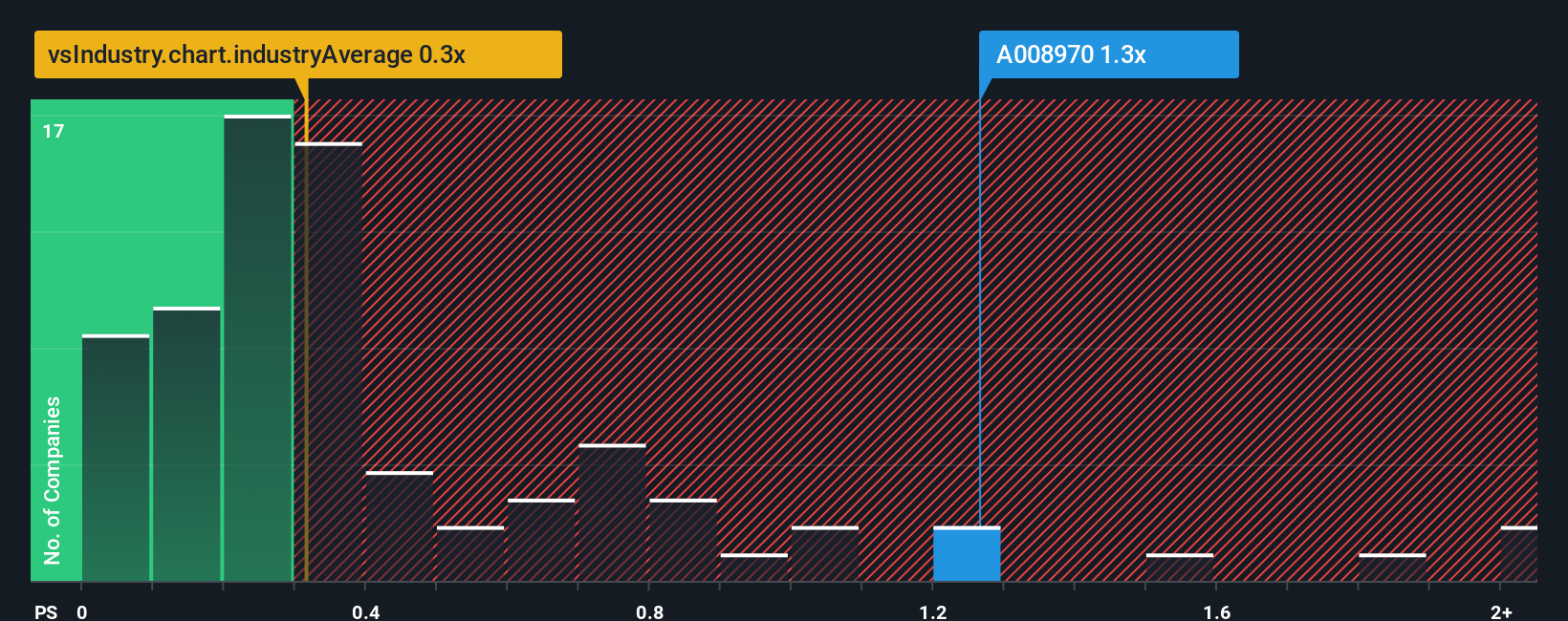

Since its price has surged higher, given close to half the companies operating in Korea's Metals and Mining industry have price-to-sales ratios (or "P/S") below 0.3x, you may consider Dong Yang Steel Pipe as a stock to potentially avoid with its 1.3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Dong Yang Steel Pipe

What Does Dong Yang Steel Pipe's P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Dong Yang Steel Pipe over the last year, which is not ideal at all. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Dong Yang Steel Pipe will help you shine a light on its historical performance.How Is Dong Yang Steel Pipe's Revenue Growth Trending?

Dong Yang Steel Pipe's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 22%. Regardless, revenue has managed to lift by a handy 19% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 2.8% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this information, we can see why Dong Yang Steel Pipe is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Key Takeaway

The large bounce in Dong Yang Steel Pipe's shares has lifted the company's P/S handsomely. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Dong Yang Steel Pipe maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Dong Yang Steel Pipe that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kbi Dong Yang Steel PipeLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A008970

Kbi Dong Yang Steel PipeLtd

Manufactures and sells steel pipes in South Korea, the United States, rest of Asia, Europe, the Middle East, and internationally.

Excellent balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor