Advertisement

- South Korea

- /

- Chemicals

- /

- KOSDAQ:A097870

HyosungONBCo.Ltd (KOSDAQ:097870) Seems To Use Debt Rather Sparingly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies HyosungONBCo.,Ltd (KOSDAQ:097870) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for HyosungONBCo.Ltd

How Much Debt Does HyosungONBCo.Ltd Carry?

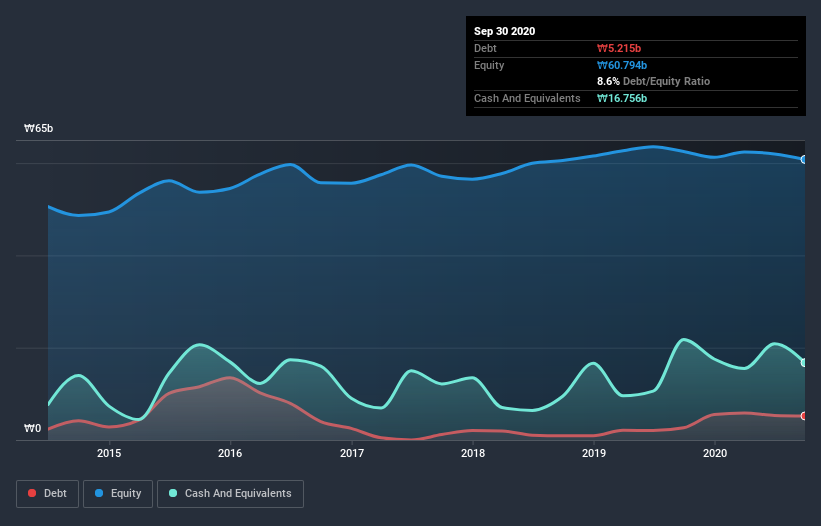

You can click the graphic below for the historical numbers, but it shows that as of September 2020 HyosungONBCo.Ltd had ₩5.21b of debt, an increase on ₩2.64b, over one year. However, it does have ₩16.8b in cash offsetting this, leading to net cash of ₩11.5b.

A Look At HyosungONBCo.Ltd's Liabilities

The latest balance sheet data shows that HyosungONBCo.Ltd had liabilities of ₩8.37b due within a year, and liabilities of ₩1.48b falling due after that. Offsetting this, it had ₩16.8b in cash and ₩10.1b in receivables that were due within 12 months. So it actually has ₩17.0b more liquid assets than total liabilities.

This surplus suggests that HyosungONBCo.Ltd is using debt in a way that is appears to be both safe and conservative. Due to its strong net asset position, it is not likely to face issues with its lenders. Succinctly put, HyosungONBCo.Ltd boasts net cash, so it's fair to say it does not have a heavy debt load!

Also good is that HyosungONBCo.Ltd grew its EBIT at 11% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since HyosungONBCo.Ltd will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. HyosungONBCo.Ltd may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, HyosungONBCo.Ltd actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that HyosungONBCo.Ltd has net cash of ₩11.5b, as well as more liquid assets than liabilities. The cherry on top was that in converted 128% of that EBIT to free cash flow, bringing in -₩3.9b. So we don't think HyosungONBCo.Ltd's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that HyosungONBCo.Ltd is showing 2 warning signs in our investment analysis , and 1 of those doesn't sit too well with us...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading HyosungONBCo.Ltd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HyosungONBCo.Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About KOSDAQ:A097870

HyosungONBCo.Ltd

Produces and supplies organic fertilizers in South Korea and internationally.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor