Advertisement

- South Korea

- /

- Paper and Forestry Products

- /

- KOSDAQ:A025900

We Think Dongwha EnterpriseLtd (KOSDAQ:025900) Has A Fair Chunk Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Dongwha Enterprise Co.,Ltd (KOSDAQ:025900) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Dongwha EnterpriseLtd

What Is Dongwha EnterpriseLtd's Debt?

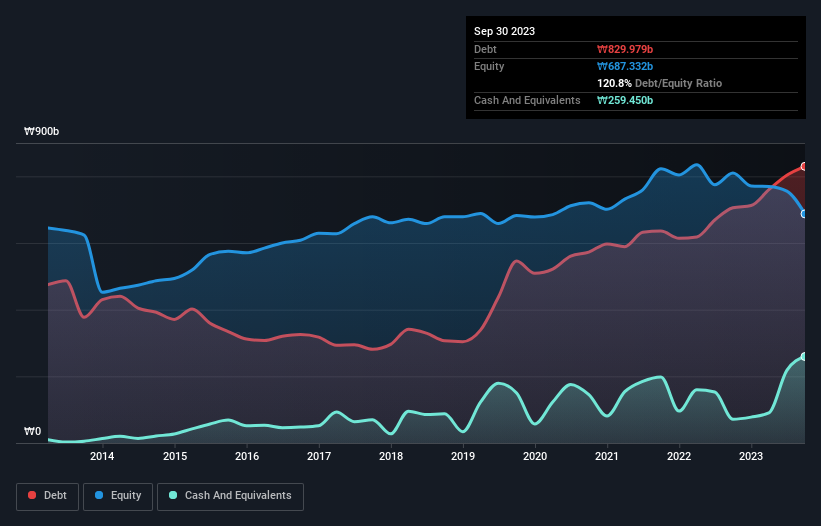

The image below, which you can click on for greater detail, shows that at September 2023 Dongwha EnterpriseLtd had debt of ₩830.0b, up from ₩705.5b in one year. On the flip side, it has ₩259.4b in cash leading to net debt of about ₩570.5b.

A Look At Dongwha EnterpriseLtd's Liabilities

Zooming in on the latest balance sheet data, we can see that Dongwha EnterpriseLtd had liabilities of ₩686.2b due within 12 months and liabilities of ₩559.4b due beyond that. Offsetting this, it had ₩259.4b in cash and ₩113.4b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩872.8b.

This deficit is considerable relative to its market capitalization of ₩1.08t, so it does suggest shareholders should keep an eye on Dongwha EnterpriseLtd's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Dongwha EnterpriseLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Dongwha EnterpriseLtd had a loss before interest and tax, and actually shrunk its revenue by 12%, to ₩978b. We would much prefer see growth.

Caveat Emptor

While Dongwha EnterpriseLtd's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at ₩16b. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. For example, we would not want to see a repeat of last year's loss of ₩74b. So we do think this stock is quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Dongwha EnterpriseLtd (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A025900

Dongwha EnterpriseLtd

Manufactures and sells wood materials in South Korea.

Slightly overvalued with minimal risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor