Advertisement

- South Korea

- /

- Metals and Mining

- /

- KOSDAQ:A005160

Not Many Are Piling Into Dongkuk Industries Co., Ltd. (KOSDAQ:005160) Stock Yet As It Plummets 27%

Dongkuk Industries Co., Ltd. (KOSDAQ:005160) shareholders won't be pleased to see that the share price has had a very rough month, dropping 27% and undoing the prior period's positive performance. The last month has meant the stock is now only up 3.0% during the last year.

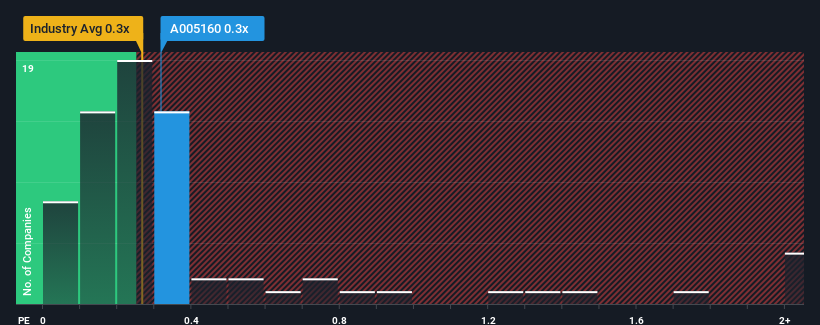

Even after such a large drop in price, it's still not a stretch to say that Dongkuk Industries' price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Metals and Mining industry in Korea, seeing as it matches the P/S ratio of the wider industry. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Dongkuk Industries

What Does Dongkuk Industries' P/S Mean For Shareholders?

Recent times have been pleasing for Dongkuk Industries as its revenue has risen in spite of the industry's average revenue going into reverse. Perhaps the market is expecting its current strong performance to taper off in accordance to the rest of the industry, which has kept the P/S contained. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Dongkuk Industries.What Are Revenue Growth Metrics Telling Us About The P/S?

In order to justify its P/S ratio, Dongkuk Industries would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 10% gain to the company's revenues. The latest three year period has also seen a 15% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 8.9% during the coming year according to the lone analyst following the company. With the industry only predicted to deliver 6.8%, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Dongkuk Industries' P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

What We Can Learn From Dongkuk Industries' P/S?

With its share price dropping off a cliff, the P/S for Dongkuk Industries looks to be in line with the rest of the Metals and Mining industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Dongkuk Industries currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. Perhaps uncertainty in the revenue forecasts are what's keeping the P/S ratio consistent with the rest of the industry. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

You need to take note of risks, for example - Dongkuk Industries has 3 warning signs (and 2 which are a bit unpleasant) we think you should know about.

If these risks are making you reconsider your opinion on Dongkuk Industries, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A005160

Dongkuk Industries

Operates as a cold rolled steel company in South Korea and internationally.

Mediocre balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor