Advertisement

- South Korea

- /

- Healthcare Services

- /

- KOSDAQ:A067630

HLB Life Science Co., Ltd.'s (KOSDAQ:067630) 25% Share Price Surge Not Quite Adding Up

Despite an already strong run, HLB Life Science Co., Ltd. (KOSDAQ:067630) shares have been powering on, with a gain of 25% in the last thirty days. The last 30 days bring the annual gain to a very sharp 76%.

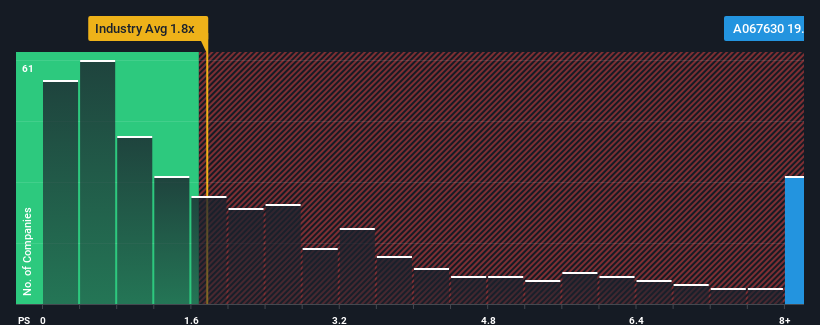

After such a large jump in price, when almost half of the companies in Korea's Healthcare industry have price-to-sales ratios (or "P/S") below 2.8x, you may consider HLB Life Science as a stock not worth researching with its 19.9x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for HLB Life Science

What Does HLB Life Science's Recent Performance Look Like?

Revenue has risen firmly for HLB Life Science recently, which is pleasing to see. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on HLB Life Science will help you shine a light on its historical performance.How Is HLB Life Science's Revenue Growth Trending?

In order to justify its P/S ratio, HLB Life Science would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered an exceptional 16% gain to the company's top line. Still, revenue has barely risen at all from three years ago in total, which is not ideal. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 17% shows it's an unpleasant look.

In light of this, it's alarming that HLB Life Science's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

HLB Life Science's P/S has grown nicely over the last month thanks to a handy boost in the share price. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that HLB Life Science currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Having said that, be aware HLB Life Science is showing 3 warning signs in our investment analysis, and 1 of those is a bit unpleasant.

If these risks are making you reconsider your opinion on HLB Life Science, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if HLB Life Science might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A067630

HLB Life Science

Develops and manufactures in vitro diagnostic medical devices and quasi-drugs in South Korea and internationally.

Imperfect balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor