Advertisement

- South Korea

- /

- Food

- /

- KOSDAQ:A189980

We Think HYUNGKUK F&B (KOSDAQ:189980) Is Taking Some Risk With Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that HYUNGKUK F&B Co., Ltd. (KOSDAQ:189980) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for HYUNGKUK F&B

What Is HYUNGKUK F&B's Debt?

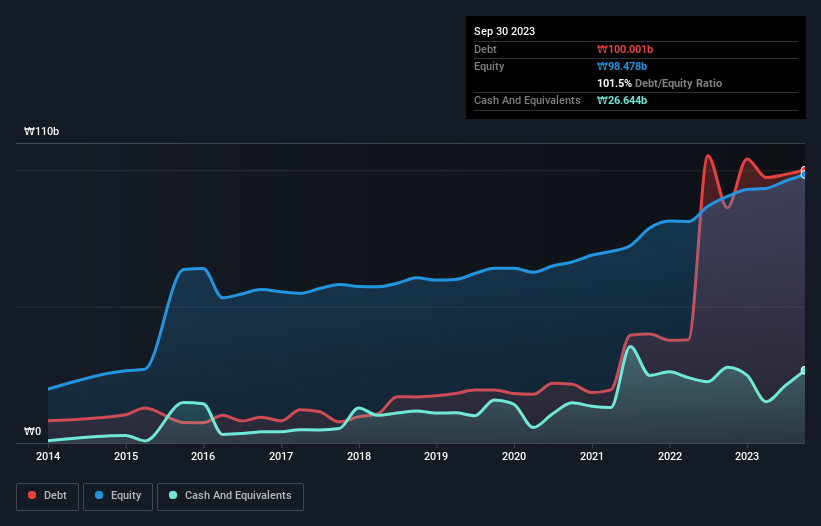

As you can see below, at the end of September 2023, HYUNGKUK F&B had ₩100.0b of debt, up from ₩86.3b a year ago. Click the image for more detail. However, it does have ₩26.6b in cash offsetting this, leading to net debt of about ₩73.4b.

How Strong Is HYUNGKUK F&B's Balance Sheet?

The latest balance sheet data shows that HYUNGKUK F&B had liabilities of ₩35.9b due within a year, and liabilities of ₩78.3b falling due after that. On the other hand, it had cash of ₩26.6b and ₩14.4b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩73.2b.

This deficit is considerable relative to its market capitalization of ₩95.2b, so it does suggest shareholders should keep an eye on HYUNGKUK F&B's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

HYUNGKUK F&B has a debt to EBITDA ratio of 4.1 and its EBIT covered its interest expense 4.6 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Notably HYUNGKUK F&B's EBIT was pretty flat over the last year. We would prefer to see some earnings growth, because that always helps diminish debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is HYUNGKUK F&B's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, HYUNGKUK F&B saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

We'd go so far as to say HYUNGKUK F&B's conversion of EBIT to free cash flow was disappointing. But at least its EBIT growth rate is not so bad. We're quite clear that we consider HYUNGKUK F&B to be really rather risky, as a result of its balance sheet health. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for HYUNGKUK F&B you should be aware of, and 1 of them is potentially serious.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if HYUNGKUK F&B might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A189980

HYUNGKUK F&B

Engages in the manufacture and sale of foods and beverages in South Korea.

Slight risk with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor