Advertisement

- South Korea

- /

- Construction

- /

- KOSDAQ:A045100

Hanyang ENG Co., Ltd. (KOSDAQ:045100) Looks Interesting, And It's About To Pay A Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Hanyang ENG Co., Ltd. (KOSDAQ:045100) is about to trade ex-dividend in the next three days. You will need to purchase shares before the 29th of December to receive the dividend, which will be paid on the 22nd of April.

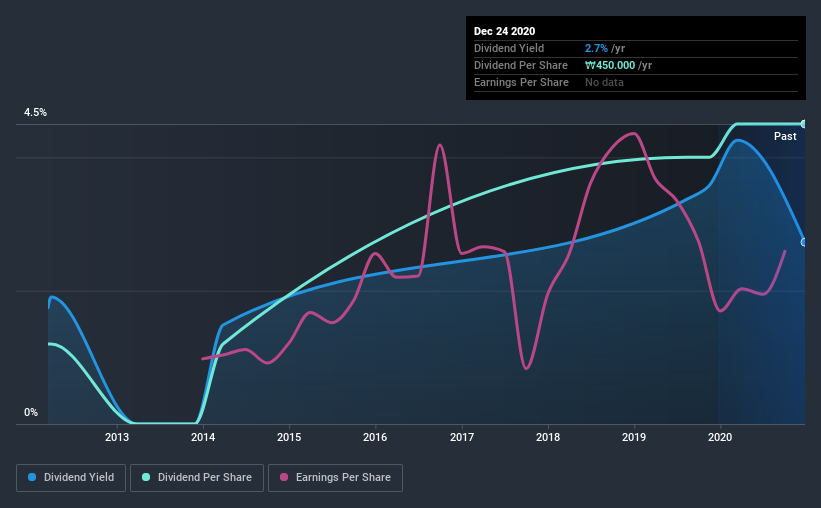

Hanyang ENG's upcoming dividend is ₩450 a share, following on from the last 12 months, when the company distributed a total of ₩450 per share to shareholders. Looking at the last 12 months of distributions, Hanyang ENG has a trailing yield of approximately 2.7% on its current stock price of ₩16500. If you buy this business for its dividend, you should have an idea of whether Hanyang ENG's dividend is reliable and sustainable. So we need to investigate whether Hanyang ENG can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Hanyang ENG

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Hanyang ENG has a low and conservative payout ratio of just 17% of its income after tax. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. What's good is that dividends were well covered by free cash flow, with the company paying out 17% of its cash flow last year.

It's positive to see that Hanyang ENG's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Hanyang ENG paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. For this reason, we're glad to see Hanyang ENG's earnings per share have risen 16% per annum over the last five years. The company has managed to grow earnings at a rapid rate, while reinvesting most of the profits within the business. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the past nine years, Hanyang ENG has increased its dividend at approximately 16% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

The Bottom Line

Should investors buy Hanyang ENG for the upcoming dividend? Hanyang ENG has grown its earnings per share while simultaneously reinvesting in the business. Unfortunately it's cut the dividend at least once in the past nine years, but the conservative payout ratio makes the current dividend look sustainable. There's a lot to like about Hanyang ENG, and we would prioritise taking a closer look at it.

So while Hanyang ENG looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. In terms of investment risks, we've identified 2 warning signs with Hanyang ENG and understanding them should be part of your investment process.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Hanyang ENG or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HANYANG ENGLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A045100

HANYANG ENGLtd

Hanyang ENG Co.,Ltd engages in the construction of semiconductor facilities in South Korea and internationally.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor