Advertisement

- South Korea

- /

- Auto Components

- /

- KOSE:A161390

Is Hankook Tire & Technology (KRX:161390) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Hankook Tire & Technology Co., Ltd. (KRX:161390) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

What Is Hankook Tire & Technology's Net Debt?

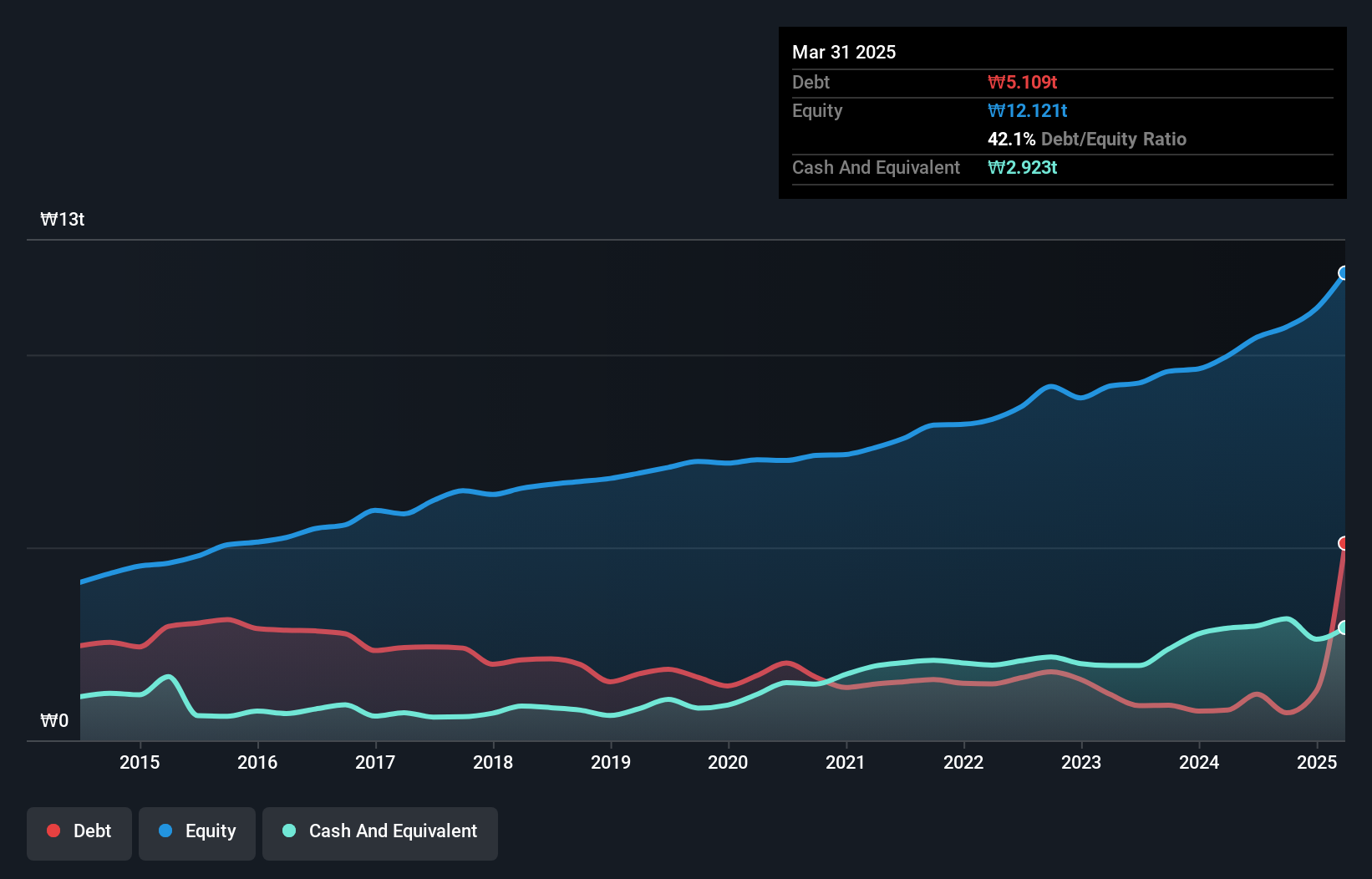

The image below, which you can click on for greater detail, shows that at March 2025 Hankook Tire & Technology had debt of ₩5.11t, up from ₩784.9b in one year. However, because it has a cash reserve of ₩2.92t, its net debt is less, at about ₩2.19t.

How Healthy Is Hankook Tire & Technology's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Hankook Tire & Technology had liabilities of ₩7.80t due within 12 months and liabilities of ₩4.23t due beyond that. Offsetting these obligations, it had cash of ₩2.92t as well as receivables valued at ₩3.80t due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩5.31t.

Given this deficit is actually higher than the company's market capitalization of ₩4.70t, we think shareholders really should watch Hankook Tire & Technology's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

Check out our latest analysis for Hankook Tire & Technology

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Hankook Tire & Technology has a low debt to EBITDA ratio of only 0.98. And remarkably, despite having net debt, it actually received more in interest over the last twelve months than it had to pay. So it's fair to say it can handle debt like a hotshot teppanyaki chef handles cooking. Also good is that Hankook Tire & Technology grew its EBIT at 12% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hankook Tire & Technology can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Hankook Tire & Technology produced sturdy free cash flow equating to 50% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

On our analysis Hankook Tire & Technology's interest cover should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. In particular, level of total liabilities gives us cold feet. Looking at all this data makes us feel a little cautious about Hankook Tire & Technology's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Hankook Tire & Technology is showing 1 warning sign in our investment analysis , you should know about...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Hankook Tire & Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSE:A161390

Hankook Tire & Technology

Manufactures and sells tires in South Korea and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor