Advertisement

- South Korea

- /

- Auto Components

- /

- KOSDAQ:A041930

Dong-A Hwa SungLtd (KOSDAQ:041930) Seems To Use Debt Quite Sensibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Dong-A Hwa Sung Co.,Ltd. (KOSDAQ:041930) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Dong-A Hwa SungLtd

What Is Dong-A Hwa SungLtd's Net Debt?

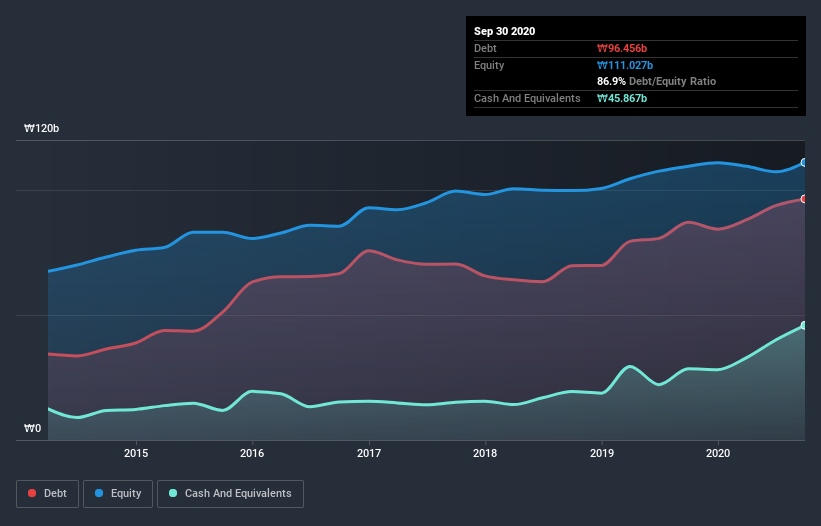

As you can see below, at the end of September 2020, Dong-A Hwa SungLtd had ₩96.5b of debt, up from ₩87.1b a year ago. Click the image for more detail. However, it does have ₩45.9b in cash offsetting this, leading to net debt of about ₩50.6b.

A Look At Dong-A Hwa SungLtd's Liabilities

The latest balance sheet data shows that Dong-A Hwa SungLtd had liabilities of ₩130.1b due within a year, and liabilities of ₩14.7b falling due after that. Offsetting this, it had ₩45.9b in cash and ₩71.9b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₩27.0b.

Of course, Dong-A Hwa SungLtd has a market capitalization of ₩193.6b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Dong-A Hwa SungLtd's net debt of 2.1 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 8.0 times interest expense) certainly does not do anything to dispel this impression. If Dong-A Hwa SungLtd can keep growing EBIT at last year's rate of 13% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Dong-A Hwa SungLtd will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Dong-A Hwa SungLtd recorded free cash flow of 42% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Both Dong-A Hwa SungLtd's ability to to cover its interest expense with its EBIT and its EBIT growth rate gave us comfort that it can handle its debt. Having said that, its conversion of EBIT to free cash flow somewhat sensitizes us to potential future risks to the balance sheet. Considering this range of data points, we think Dong-A Hwa SungLtd is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Dong-A Hwa SungLtd (of which 1 is a bit concerning!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade Dong-A Hwa SungLtd, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KOSDAQ:A041930

Dong-A Hwa SungLtd

Engages in the production and sale of automotive rubber parts in Korea and internationally.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor