Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6779

Not Many Are Piling Into Nihon Dempa Kogyo Co., Ltd. (TSE:6779) Stock Yet As It Plummets 26%

The Nihon Dempa Kogyo Co., Ltd. (TSE:6779) share price has fared very poorly over the last month, falling by a substantial 26%. For any long-term shareholders, the last month ends a year to forget by locking in a 51% share price decline.

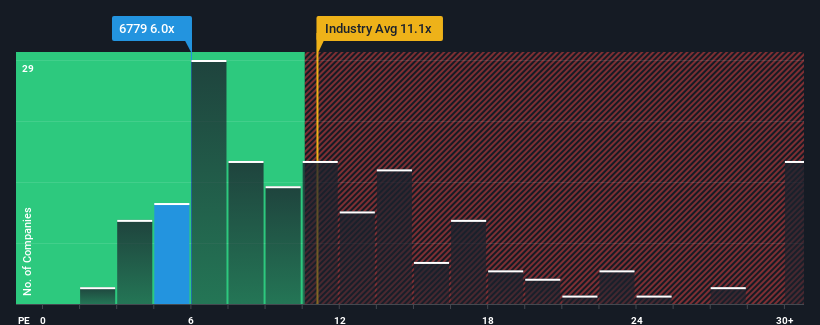

Even after such a large drop in price, Nihon Dempa Kogyo may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 6x, since almost half of all companies in Japan have P/E ratios greater than 13x and even P/E's higher than 19x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

Nihon Dempa Kogyo could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for Nihon Dempa Kogyo

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Nihon Dempa Kogyo's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 18% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 34% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 33% as estimated by the three analysts watching the company. With the market only predicted to deliver 10%, the company is positioned for a stronger earnings result.

With this information, we find it odd that Nihon Dempa Kogyo is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From Nihon Dempa Kogyo's P/E?

Nihon Dempa Kogyo's P/E looks about as weak as its stock price lately. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Nihon Dempa Kogyo's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Nihon Dempa Kogyo , and understanding these should be part of your investment process.

If you're unsure about the strength of Nihon Dempa Kogyo's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Nihon Dempa Kogyo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6779

Nihon Dempa Kogyo

Engages in the manufacture and sale of crystal-related products in Japan, China, the United States, Germany, Korea, Mexico, Hungary, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor