- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6762

TDK (TSE:6762) Earnings Call Set for Nov 1, 2024; Strong Growth Despite Supply Chain Risks

Reviewed by Simply Wall St

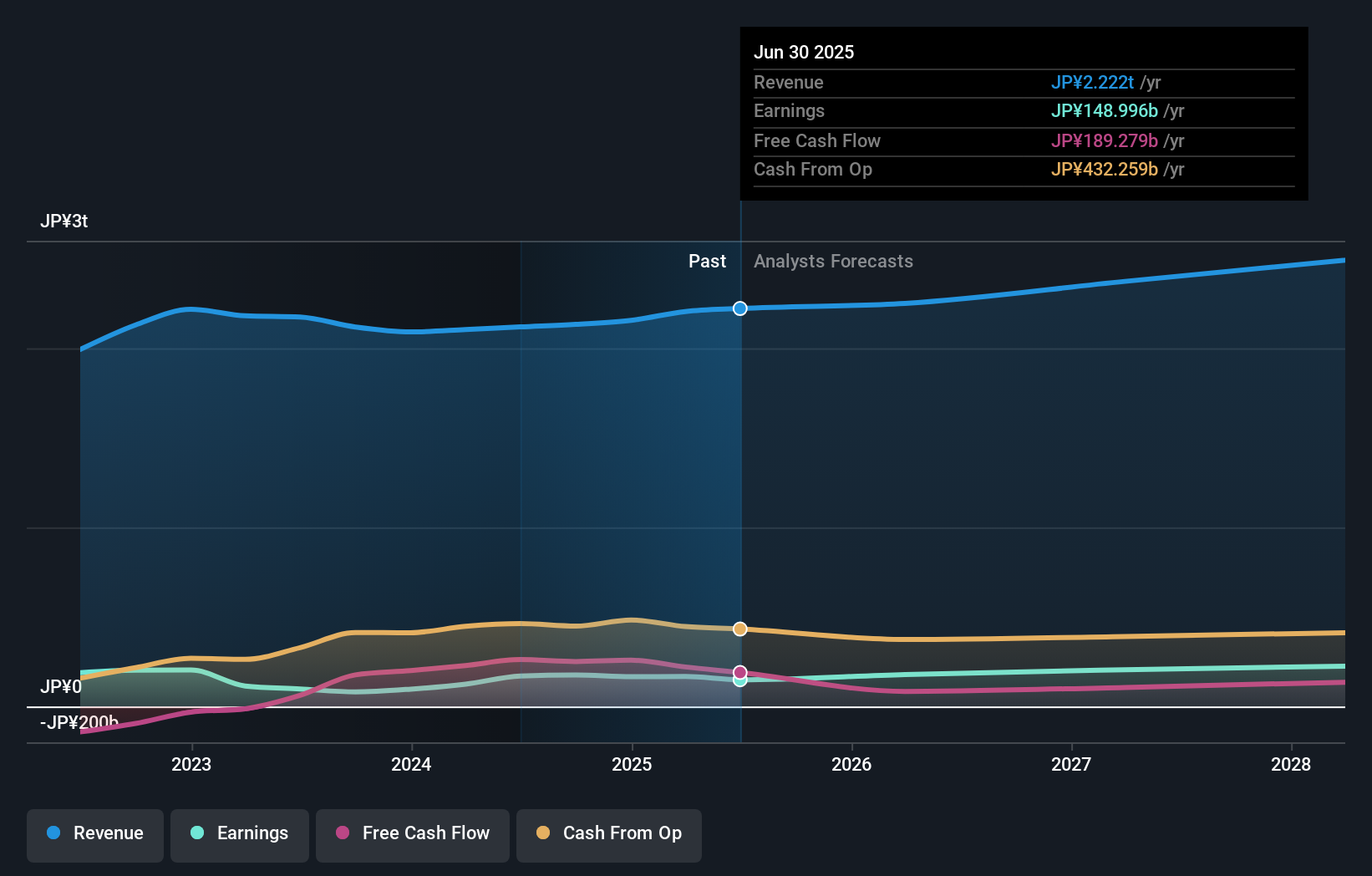

TDK (TSE:6762) is set to announce its Q2 2025 earnings on November 1, 2024, following a year of remarkable earnings growth at 116.4%, far surpassing its five-year average. Investors should look for insights into how TDK plans to sustain its operational efficiency and navigate challenges such as premium valuation concerns and supply chain disruptions. The upcoming report may also shed light on TDK's strategic innovations and alliances, which are crucial for maintaining its competitive edge in emerging markets.

Click here and access our complete analysis report to understand the dynamics of TDK.

Innovative Factors Supporting TDK

TDK's earnings growth of 116.4% over the past year significantly surpasses its 5-year average of 16% per year, demonstrating strong financial performance. The company's ability to report high-quality earnings and improve net profit margins from 3.8% to 8.3% highlights its operational efficiency and strategic prowess. TDK's strong financial health is underscored by its cash reserves exceeding total debt, ensuring sufficient earnings to cover interest payments. The management's experience, with an average tenure of 3.7 years, plays a crucial role in steering the company towards sustained growth and innovation. Additionally, while the Price-To-Earnings Ratio (21.1x) is higher than the industry average, it trades below its SWS fair value of ¥2002.03, making it an attractive option at ¥1960.

Challenges Constraining TDK's Potential

The company's Price-To-Earnings Ratio of 21.1x, compared to the JP Electronic industry average of 12.7x, suggests a premium valuation that may deter some investors. Return on Equity stands at 10.3%, which is below the desirable 20% threshold, indicating a need for improved capital efficiency. Volatile dividend payments over the past decade raise concerns about reliability, potentially impacting investor confidence. Furthermore, the board's average tenure of 2.9 years suggests a lack of seasoned oversight, which could hinder strategic decision-making and long-term planning.

Emerging Markets or Trends for TDK

TDK is poised for growth with an expected annual profit increase of 9.1%, outpacing the JP market's forecast of 8.9%. Revenue growth is projected at 5.5% per year, surpassing the JP market's 4.2%, indicating strong market positioning. The potential for dividend growth, backed by increased payments over the past decade, offers additional appeal to investors. Strategic product innovations, as highlighted in recent earnings calls, and alliances could further enhance TDK's market position and capitalize on emerging opportunities.

Key Risks and Challenges That Could Impact TDK's Success

Despite positive forecasts, TDK's revenue growth projection of 5.5% is below the industry standard of 20%, potentially limiting its competitive edge. The modest target price increase of less than 20% above the current share price suggests limited upside potential. Additionally, supply chain disruptions, as noted in recent earnings calls, pose a threat to meeting demand, necessitating robust risk management strategies. Economic headwinds and aggressive market competition further compound these challenges, requiring strategic vigilance to maintain market share.

See what the latest analyst reports say about TDK's future prospects and potential market movements.Conclusion

TDK's impressive earnings growth and improved net profit margins signify its strong operational efficiency and strategic acumen, positioning it well for continued success. Despite a Price-To-Earnings Ratio of 21.1x, which is higher than the industry average of 12.7x and may deter some investors, the company's current trading price of ¥1960 is below its estimated fair value of ¥2002.03, suggesting potential for appreciation. However, challenges such as supply chain disruptions and a lower-than-industry-standard revenue growth projection of 5.5% highlight the need for robust risk management and strategic planning to maintain its competitive edge. With a focus on strategic product innovations and alliances, TDK is poised to capitalize on emerging market opportunities, though it must address capital efficiency and board oversight to ensure sustained investor confidence and long-term growth.

Key Takeaways

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if TDK might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSE:6762

TDK

Engages in manufacture and sale of electronic components in Japan, Europe, China, Asia, the Americas, and internationally.

Flawless balance sheet with solid track record.