Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6645

OMRON (TSE:6645): Assessing Valuation Following Recent Share Price Decline

Simply Wall St

Reviewed by Simply Wall St

OMRON (TSE:6645) shares have seen muted action recently, drawing the attention of investors curious about what is driving the current stock trajectory. Various indicators suggest there could be opportunities for those taking a closer look.

See our latest analysis for OMRON.

OMRON’s share price has taken a notable slide lately, falling over 13% in the past week and more than 25% year-to-date, as investors reassess the company’s outlook amid shifting market sentiment. The latest 1-year total shareholder return of -26.7% highlights ongoing challenges. However, long-term performance hints that momentum has cooled and the valuation story remains a key theme.

Curious what else is in play right now? Now could be the perfect time to broaden your search and discover fast growing stocks with high insider ownership.

With its recent slump and long-term underperformance, is OMRON now trading below its true value, or are investors simply adjusting to a slower growth outlook, leaving little room for upside? Could there be a buying opportunity, or is the market already pricing in future gains?

Price-to-Earnings of 26.5x: Is it justified?

OMRON’s shares last closed at ¥3,864, reflecting a valuation that is considerably higher than sector peers when measured by the price-to-earnings (P/E) ratio. Despite recent declines, this multiple signals that investors are still willing to pay a premium for future earnings.

The price-to-earnings ratio is a key gauge of how much investors are willing to pay today for a company’s future profits. For an established player in the electronic sector, it helps indicate whether expectations for growth or quality are elevated relative to the broader market.

Currently, OMRON’s P/E of 26.5x far exceeds the Japanese electronic industry average of 14.9x. This suggests that the shares are trading at a significant premium to immediate peers. The implied fair P/E of 23.4x is also lower than the current multiple, highlighting a gap that could close if market sentiment shifts or earnings growth does not materialize as expected.

Explore the SWS fair ratio for OMRON

Result: Price-to-Earnings of 26.5x (OVERVALUED)

However, slower revenue growth or unexpected earnings pressure could quickly reshape investor sentiment and challenge the premium valuation currently assigned to OMRON’s shares.

Find out about the key risks to this OMRON narrative.

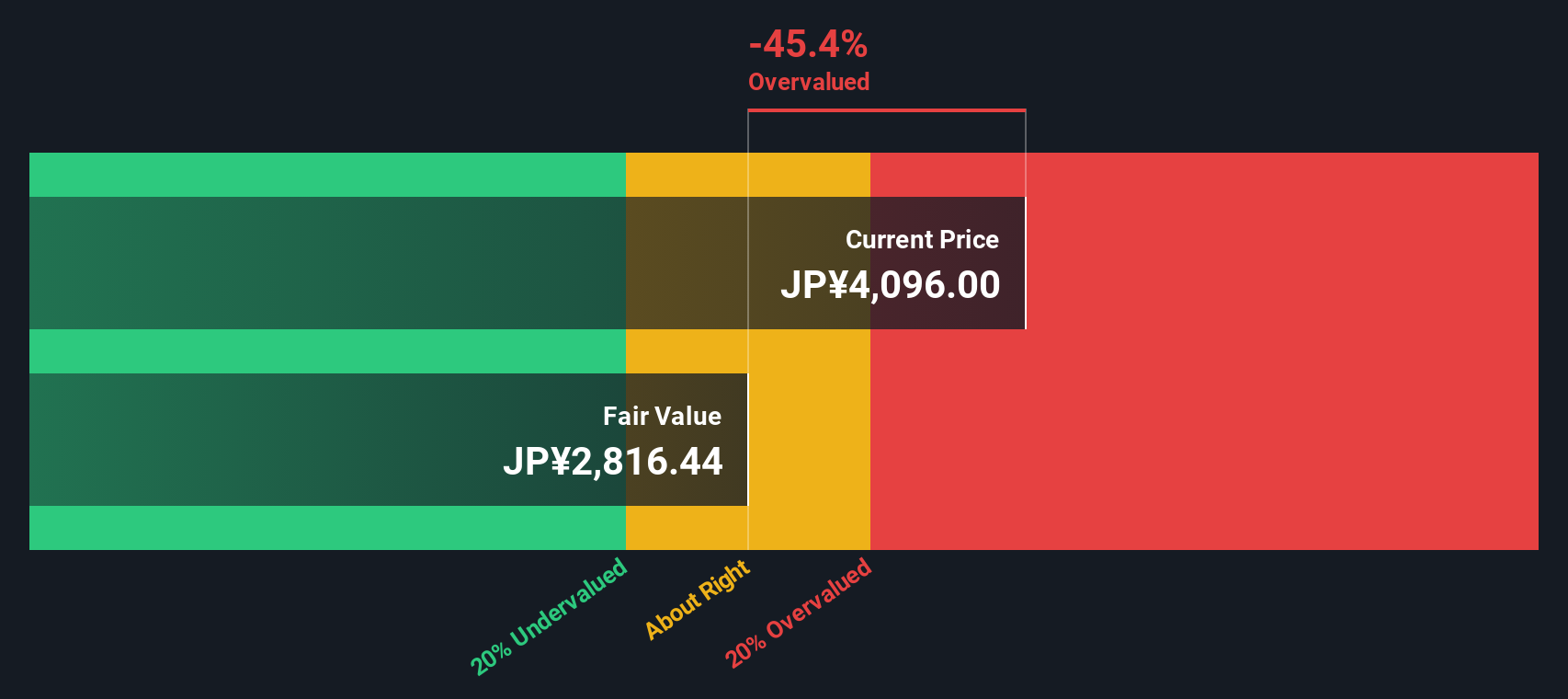

Another View: Discounted Cash Flow Model

While the premium price-to-earnings ratio paints OMRON as overvalued, our SWS DCF model offers a different perspective. Based on projected future cash flows, it suggests the shares are trading above fair value, at a price significantly higher than our intrinsic valuation estimate. Could this indicate that the current valuation remains too high, or does it overlook OMRON’s long-term earnings potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OMRON for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 867 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OMRON Narrative

If you see the numbers differently, or would rather chart your own course through OMRON's data, you can build your own narrative in just a few minutes: Do it your way.

A great starting point for your OMRON research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you want to stay ahead in today’s market, don’t settle for the obvious. Powerful opportunities await smart investors willing to look beyond the headline stocks.

- Unlock the potential of stocks positioned for strong cash flow and future gains by researching these 867 undervalued stocks based on cash flows where hidden value can translate into strong returns.

- Benefit from steady income streams and boost your portfolio with these 16 dividend stocks with yields > 3%, which offers higher than average yields for income-focused investors.

- Seize the rise of AI-driven innovation and spot tomorrow’s tech leaders by examining these 25 AI penny stocks before everyone else catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6645

OMRON

Engages in industrial automation, device and module solutions, data solutions, social systems, and healthcare businesses in Japan and internationally.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor