Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:8035

Tokyo Electron (TSE:8035) Is Up 12.9% After Raising Dividend and Earnings Outlook Has The Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- Tokyo Electron’s Board of Directors announced on October 31, 2025, that it would pay an increased interim dividend of ¥264 per share for the first half of FY2026, up from ¥245 previously, and raised its full-year earnings guidance following an improved financial performance in the July-September period.

- The company’s upward revision of both dividend and profit forecasts signals strengthened business momentum and highlights management’s commitment to linking shareholder returns directly with business results.

- We’ll examine how Tokyo Electron’s improved profit outlook and dividend hike could reshape the company’s investment narrative and sector positioning.

Find companies with promising cash flow potential yet trading below their fair value.

Tokyo Electron Investment Narrative Recap

To be a shareholder in Tokyo Electron right now, you need to believe that structural technology drivers like AI and digital transformation will outweigh industry cyclicality and exposure to market slowdowns, particularly in China. While the recent dividend hike and raised earnings guidance strengthen confidence in short-term momentum, the biggest catalyst, renewed capital spending for next-generation chips due late 2026, remains unchanged; risks from possible export controls and erratic equipment demand are still present, and the latest news does not meaningfully alter that risk-reward balance.

Among recent updates, the company’s upward revision of full-year profit guidance is most relevant, reflecting improved operational performance and a higher operating profit forecast for the year. This creates a stronger backdrop for near-term shareholder returns, but does not reduce the headwinds from unpredictable customer investments and increasing competition in China that still shape the stock’s risk profile.

In contrast, investors should be mindful that even with the latest results, shifts in customer capital spending patterns could still quickly alter Tokyo Electron's outlook if...

Read the full narrative on Tokyo Electron (it's free!)

Tokyo Electron's outlook anticipates ¥2,966.7 billion in revenue and ¥666.1 billion in earnings by 2028. This scenario is based on a 6.9% annual revenue growth rate and a ¥130.4 billion increase in earnings from the current ¥535.7 billion.

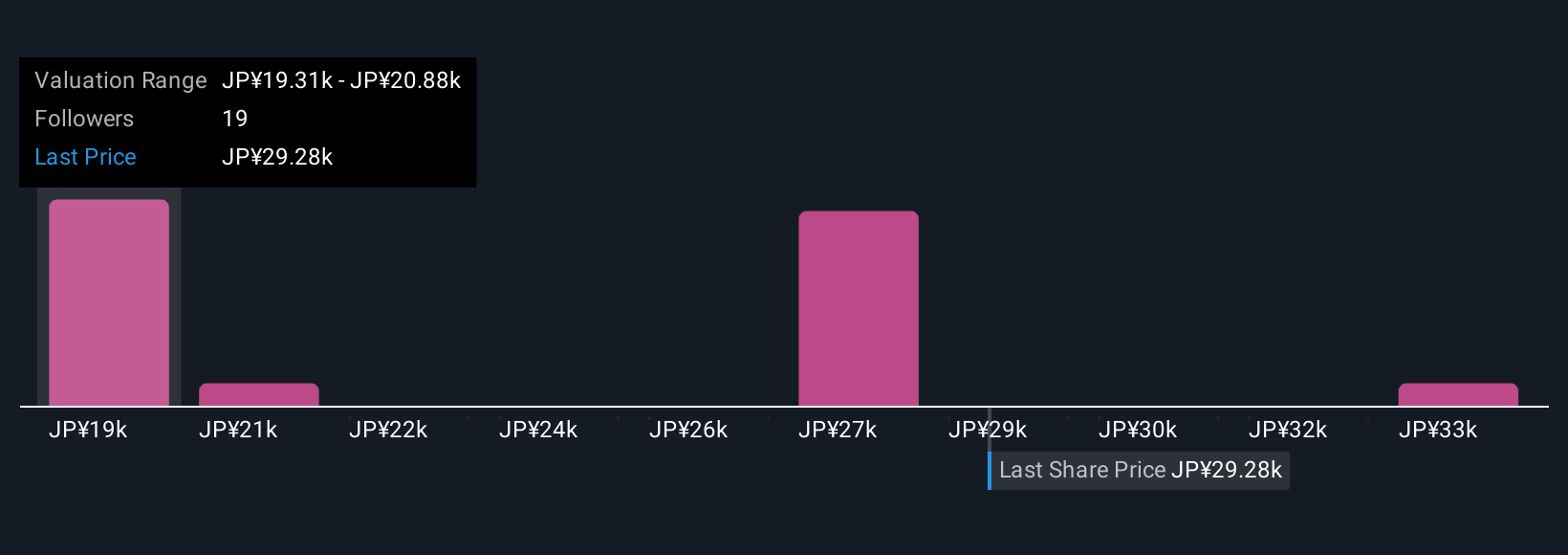

Uncover how Tokyo Electron's forecasts yield a ¥29351 fair value, a 14% downside to its current price.

Exploring Other Perspectives

Six individual retail investors from the Simply Wall St Community have placed their fair value estimates for Tokyo Electron between ¥17,858 and ¥35,063 per share. While expectations around a coming wave of advanced chip spending is fueling optimism, recurring concerns over cyclical equipment demand remind you that community perspectives can diverge sharply and are worth comparing.

Explore 6 other fair value estimates on Tokyo Electron - why the stock might be worth 48% less than the current price!

Build Your Own Tokyo Electron Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tokyo Electron research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Tokyo Electron research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tokyo Electron's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tokyo Electron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8035

Tokyo Electron

Develops, manufactures, and sells semiconductor production equipment in Japan, South Korea, Taiwan, China, North America, Europe, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor