Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:7735

Is SCREEN Holdings Still Attractive After a 35% Rally and Recent Global Expansion?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if SCREEN Holdings is the kind of stock that’s genuinely worth your money, or just the latest name everyone’s talking about? You’re not alone. There’s more than meets the eye when it comes to its current price.

- The stock has climbed 35.3% year-to-date and boasts a remarkable 208.1% return over three years, but also saw a recent dip of 11.4% in the past month. This shows just how quickly sentiment can shift.

- SCREEN Holdings recently caught investor attention after expanding its semiconductor equipment business globally, and the company has maintained momentum with new partnerships in Asia and North America. These moves are adding interesting layers of growth potential, but also raise questions about how sustainable these results may be.

- When we look at the numbers, SCREEN Holdings lands a 4/6 valuation score, indicating it’s undervalued on four key checks. We’ll get into the details behind this score, explore the valuation models most investors rely on, and wrap up with a perspective that could give you an even sharper edge.

Find out why SCREEN Holdings's 31.1% return over the last year is lagging behind its peers.

Approach 1: SCREEN Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future free cash flows and discounting them back to their present value. This method allows investors to assess whether a stock is trading above or below its calculated “fair value” today, based on expected performance.

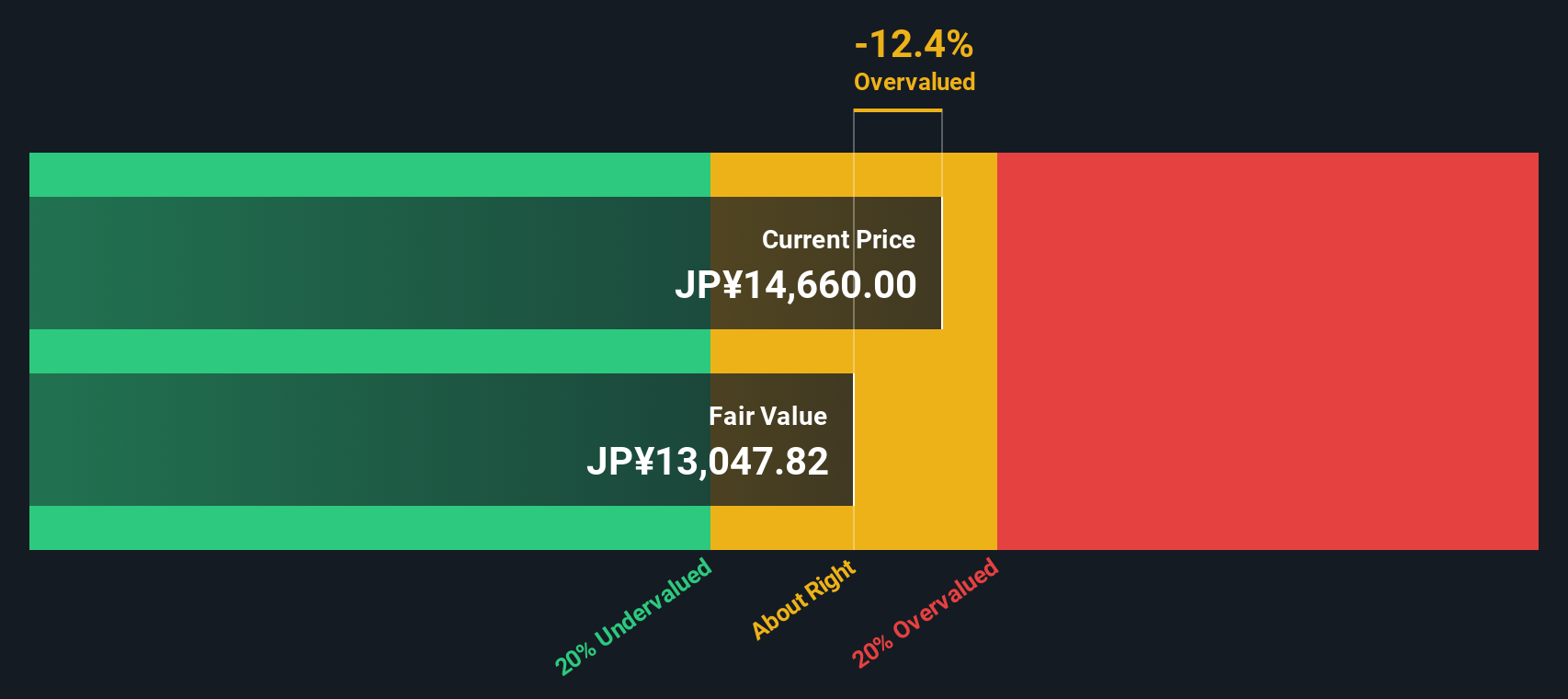

For SCREEN Holdings, the current Free Cash Flow stands at ¥34,907 million. Analyst projections, available for the next five years, show continued strong performance, with expected cash flow reaching ¥73,216 million by 2026. By 2030, Simply Wall St’s extrapolated numbers anticipate Free Cash Flow could rise as high as ¥107,635 million. After discounting all future cash flows, the DCF model estimates a fair value of ¥14,339 per share.

At current prices, this DCF analysis suggests SCREEN Holdings is trading at roughly a 9.3% discount compared to its intrinsic value. While not a massive gap, it indicates the market may be slightly underappreciating SCREEN Holdings’ future cash generation power.

Result: ABOUT RIGHT

SCREEN Holdings is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

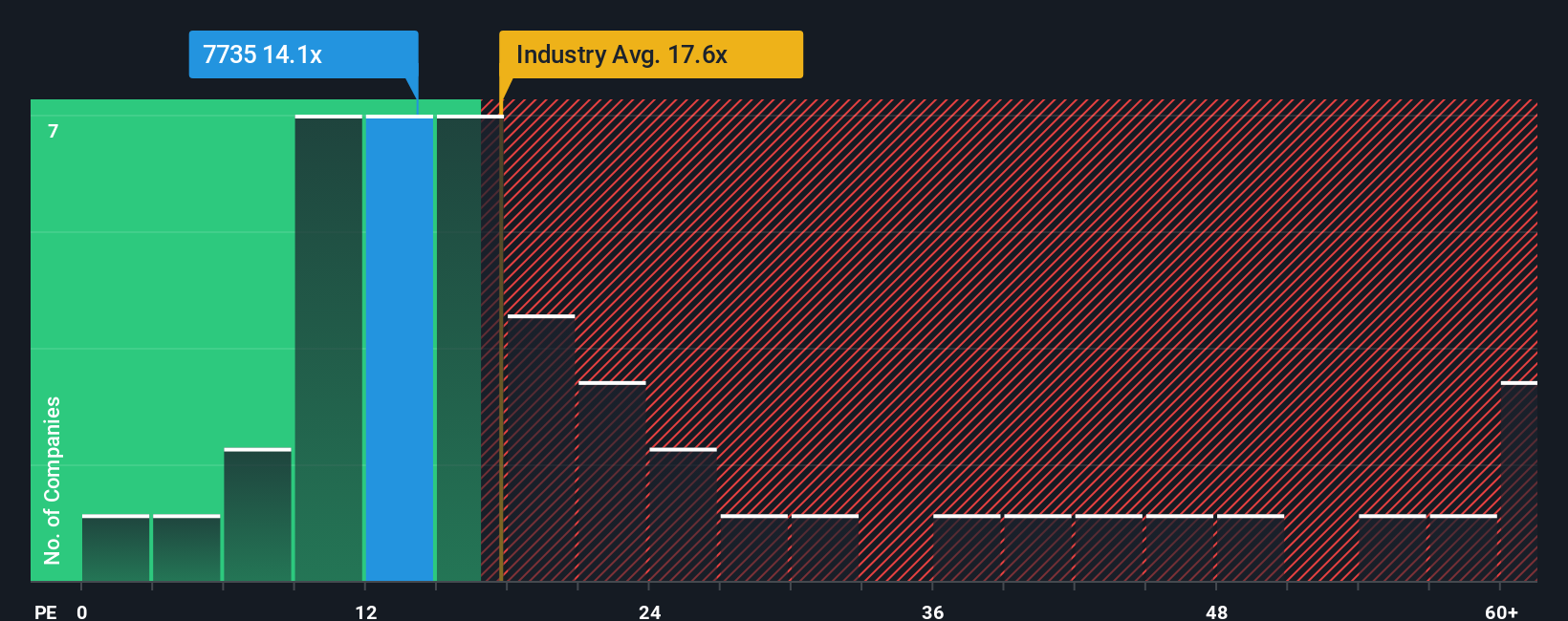

Approach 2: SCREEN Holdings Price vs Earnings

For profitable companies like SCREEN Holdings, the Price-to-Earnings (PE) ratio is a widely accepted valuation tool. It allows investors to quickly gauge how much the market is willing to pay for each yen of net income. This approach is especially useful when the company has a consistent track record of earnings. However, what counts as a “fair” PE ratio depends not just on raw profits, but also on expectations for future growth and the perceived risks facing the business.

Currently, SCREEN Holdings trades at a PE ratio of 13.3x. This is notably below both the average for its semiconductor industry peers at 20.3x and the peer group average of 24.0x. At first glance, this might suggest that the stock is undervalued compared to companies with similar business models, growth prospects, and market conditions.

Simply Wall St’s “Fair Ratio” for SCREEN Holdings stands at 21.0x. This proprietary metric weighs the company’s earnings growth potential, profit margins, sector characteristics, overall risk, and size in the market. This method offers a more tailored picture of value than generic industry or peer comparisons. Because it incorporates so many factors, the Fair Ratio is a more nuanced benchmark for investors evaluating their options.

Comparing the current PE of 13.3x to the Fair Ratio of 21.0x indicates that SCREEN Holdings is trading well below where its fundamentals suggest. There is a significant gap between how the company is valued today and its fair value based on underlying business strength and outlook.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your SCREEN Holdings Narrative

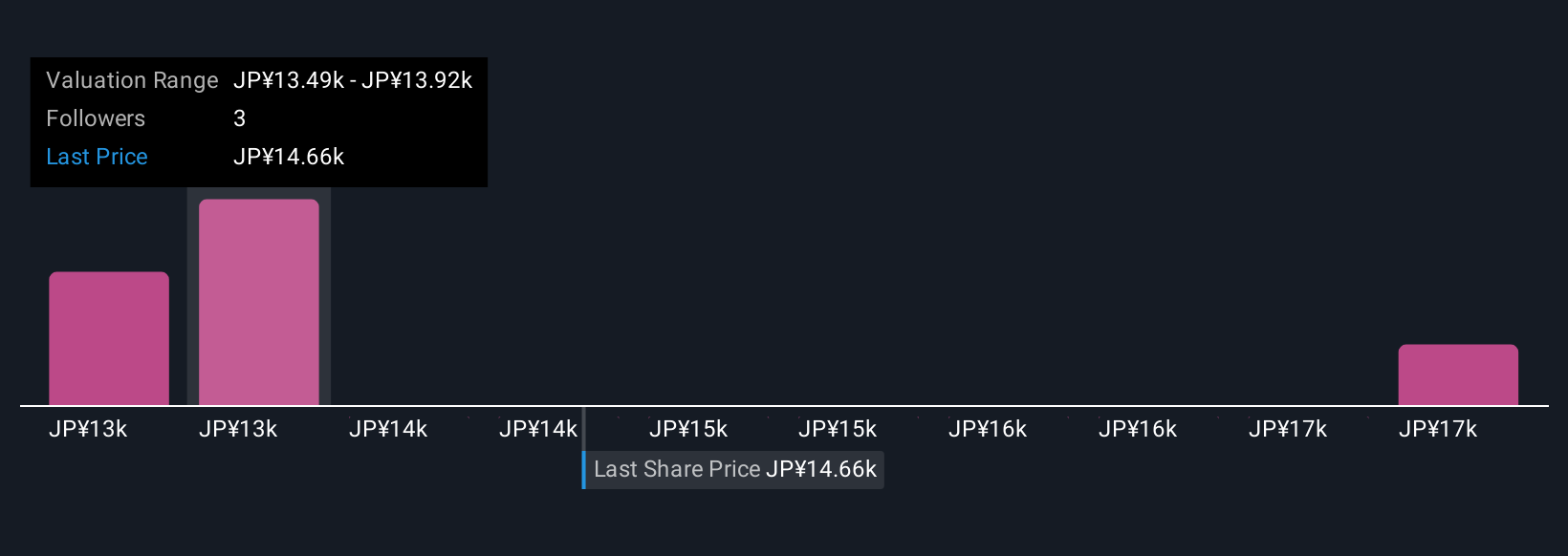

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is your personal story about a company, where you connect the dots between its business drivers, risks, and future outlook, and then translate these ideas into estimates for future revenue, earnings, margins, and ultimately, fair value.

Narratives make investing more approachable. They link the company’s story to a financial forecast, and from that forecast to a single fair value estimate. This helps you move beyond the numbers and see how your investment perspective stacks up. Narratives are simple and accessible to create or explore on the Simply Wall St Community page, where millions of investors share and update their own views.

With Narratives, you can quickly see if your fair value is above or below the current price by making comparisons, and because Narratives automatically update when news or new earnings come in, you are always working with the latest outlook. For SCREEN Holdings, for example, some users see a bright future, forecasting a fair value as high as ¥17,800, while more conservative investors set theirs at ¥11,500, demonstrating how your story can shape your strategy.

Do you think there's more to the story for SCREEN Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7735

SCREEN Holdings

Develops, manufactures, and markets semiconductor production equipment in Japan, Taiwan, South Korea, China, the United States, Europe, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative