Advertisement

- Japan

- /

- Real Estate

- /

- TSE:8802

Mitsubishi Estate (TSE:8802) Valuation in Focus After Buyback Completion and Dividend Hike

Simply Wall St

Reviewed by Simply Wall St

Mitsubishi Estate (TSE:8802) has just wrapped up its planned share buyback, repurchasing nearly 2.7% of outstanding shares. At the same time, it increased its quarterly dividend and provided guidance for even higher payouts in the future.

See our latest analysis for Mitsubishi Estate.

All this comes as Mitsubishi Estate’s share price has built impressive momentum, climbing nearly 60% year-to-date and delivering a total shareholder return of 68% over the past year. Alongside the completed buyback and dividend hike, these gains suggest investors are increasingly seeing growth ahead and valuing the company’s shareholder-friendly moves more highly.

If Mitsubishi Estate’s recent run has you wondering what else might be out there, now is a great time to broaden your search and discover fast growing stocks with high insider ownership

With Mitsubishi Estate’s shares hitting new highs and management signaling optimism with higher dividends and buybacks, the key question now is whether the stock remains undervalued or if the market has already priced in future growth. Is there still a buying opportunity, or are investors now chasing momentum?

Price-to-Earnings of 21.4x: Is it justified?

Mitsubishi Estate is currently trading on a price-to-earnings (P/E) ratio of 21.4x, which is well above its direct competitors and broader market averages. With shares recently hitting new highs, this lofty valuation stands out in the context of its recent buyback and guidance upgrades.

The price-to-earnings ratio measures how much investors are willing to pay for each yen of earnings the company generates. It is especially relevant for real estate management and development companies like Mitsubishi Estate, as it reflects long-term profit expectations in a capital-intensive sector.

Right now, the P/E ratio sits much higher than both the estimated fair P/E of 19.8x and the peer average of just 13.2x. This suggests the market is pricing in strong earnings resilience and future growth. However, compared to the broader Japanese real estate industry’s average P/E of 11.4x, this premium is even more significant. If the market’s optimism fades or company performance slows, the ratio could ultimately move closer to the fair level projected by fundamentals.

Explore the SWS fair ratio for Mitsubishi Estate

Result: Price-to-Earnings of 21.4x (OVERVALUED)

However, any slowdown in revenue growth or weaker net income could quickly shift sentiment and put pressure on Mitsubishi Estate’s elevated valuation.

Find out about the key risks to this Mitsubishi Estate narrative.

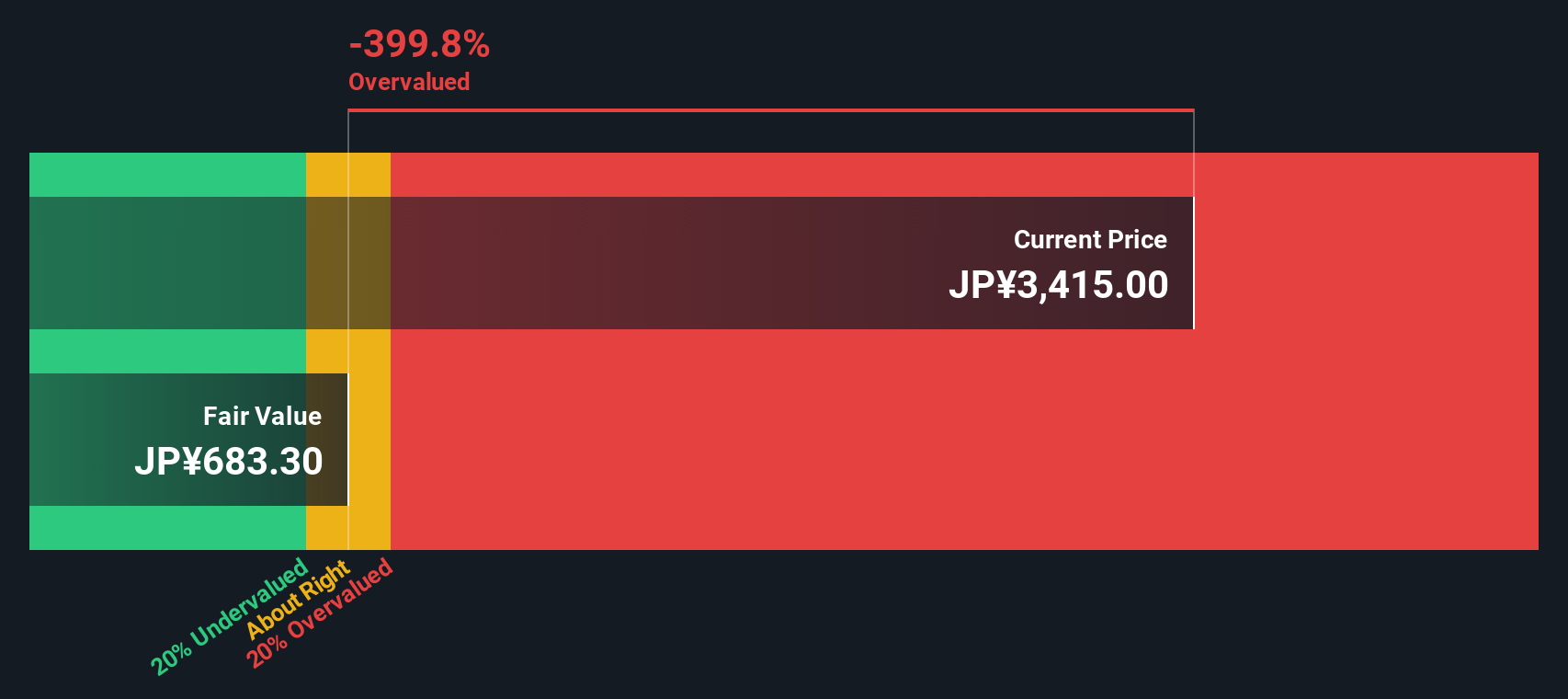

Another View: What Does the DCF Model Say?

While the current price-to-earnings ratio paints Mitsubishi Estate as expensive, the SWS DCF model takes a different approach by focusing on the company’s future cash flow potential. According to this model, the shares appear significantly overvalued and are trading far above the DCF-derived fair value.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mitsubishi Estate for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 918 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mitsubishi Estate Narrative

For those who want a second opinion or believe there’s another side to the story, it only takes a few minutes to dive into the numbers yourself and build your own narrative. Do it your way

A great starting point for your Mitsubishi Estate research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Missing out on tomorrow's winners is never fun. Use the Simply Wall Street Screener now for opportunities tailored to your goals and find your next advantage before the crowd catches on.

- Seize the chance to target steady returns with these 17 dividend stocks with yields > 3% offering attractive yields above 3%.

- Uncover rapid innovation by checking out these 25 AI penny stocks powering breakthroughs in artificial intelligence and automation.

- Stay ahead of the market with these 3603 penny stocks with strong financials packed with financially strong companies primed for growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8802

Mitsubishi Estate

Engages in the real estate activities in Japan and internationally.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor