Advertisement

The latest analyst coverage could presage a bad day for TKP Corporation (TSE:3479), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue estimates were cut sharply as analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well. Investors however, have been notably more optimistic about TKP recently, with the stock price up a notable 19% to JP¥1,471 in the past week. Whether the downgrade will have a negative impact on demand for shares is yet to be seen.

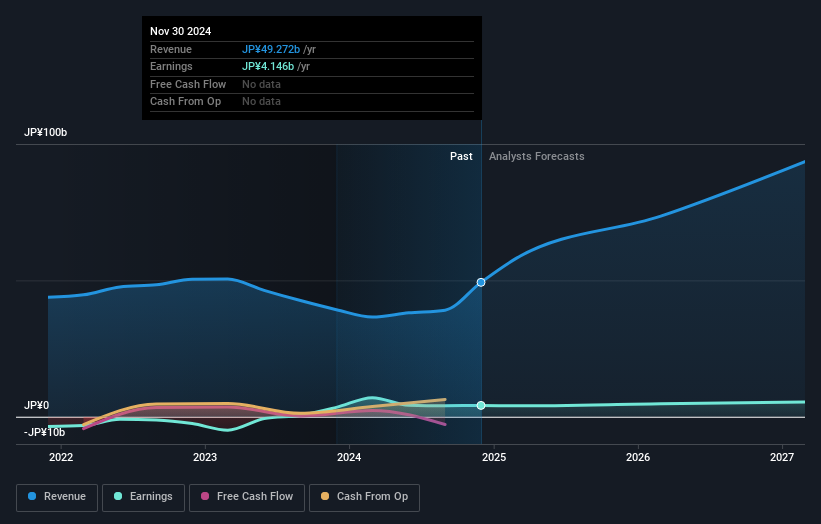

Following the downgrade, the current consensus from TKP's three analysts is for revenues of JP¥74b in 2026 which - if met - would reflect a substantial 49% increase on its sales over the past 12 months. Statutory earnings per share are presumed to expand 17% to JP¥115. Before this latest update, the analysts had been forecasting revenues of JP¥82b and earnings per share (EPS) of JP¥125 in 2026. Indeed, we can see that analyst sentiment has declined measurably after the new consensus came out, with a substantial drop in revenue estimates and a small dip in EPS estimates to boot.

See our latest analysis for TKP

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the TKP's past performance and to peers in the same industry. One thing stands out from these estimates, which is that TKP is forecast to grow faster in the future than it has in the past, with revenues expected to display 38% annualised growth until the end of 2026. If achieved, this would be a much better result than the 4.1% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 4.2% per year. So it looks like TKP is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for TKP. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on TKP after today.

In light of the downgrade, our automated discounted cash flow valuation tool suggests that TKP could now be moderately overvalued. Learn why, and examine the assumptions that underpin our valuation by visiting our free platform here to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

Valuation is complex, but we're here to simplify it.

Discover if TKP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3479

TKP

Engages in the space revitalization and distribution business in Japan and internationally.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor