Advertisement

- Japan

- /

- Entertainment

- /

- TSE:9602

How Investors May Respond To Toho (TSE:9602) Completing Its ¥14.9 Billion Share Buyback Program

Simply Wall St

Reviewed by Sasha Jovanovic

- Toho recently completed its share repurchase program, buying back 1,700,000 shares, equivalent to 1% of its outstanding stock, for ¥14,929.4 million between October 15 and November 13, 2025.

- This move signals management’s confidence in the company’s direction and can enhance value for existing shareholders by reducing the share count.

- We’ll examine how Toho’s buyback completion reinforces its investment narrative and underscores management’s commitment to shareholder returns.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

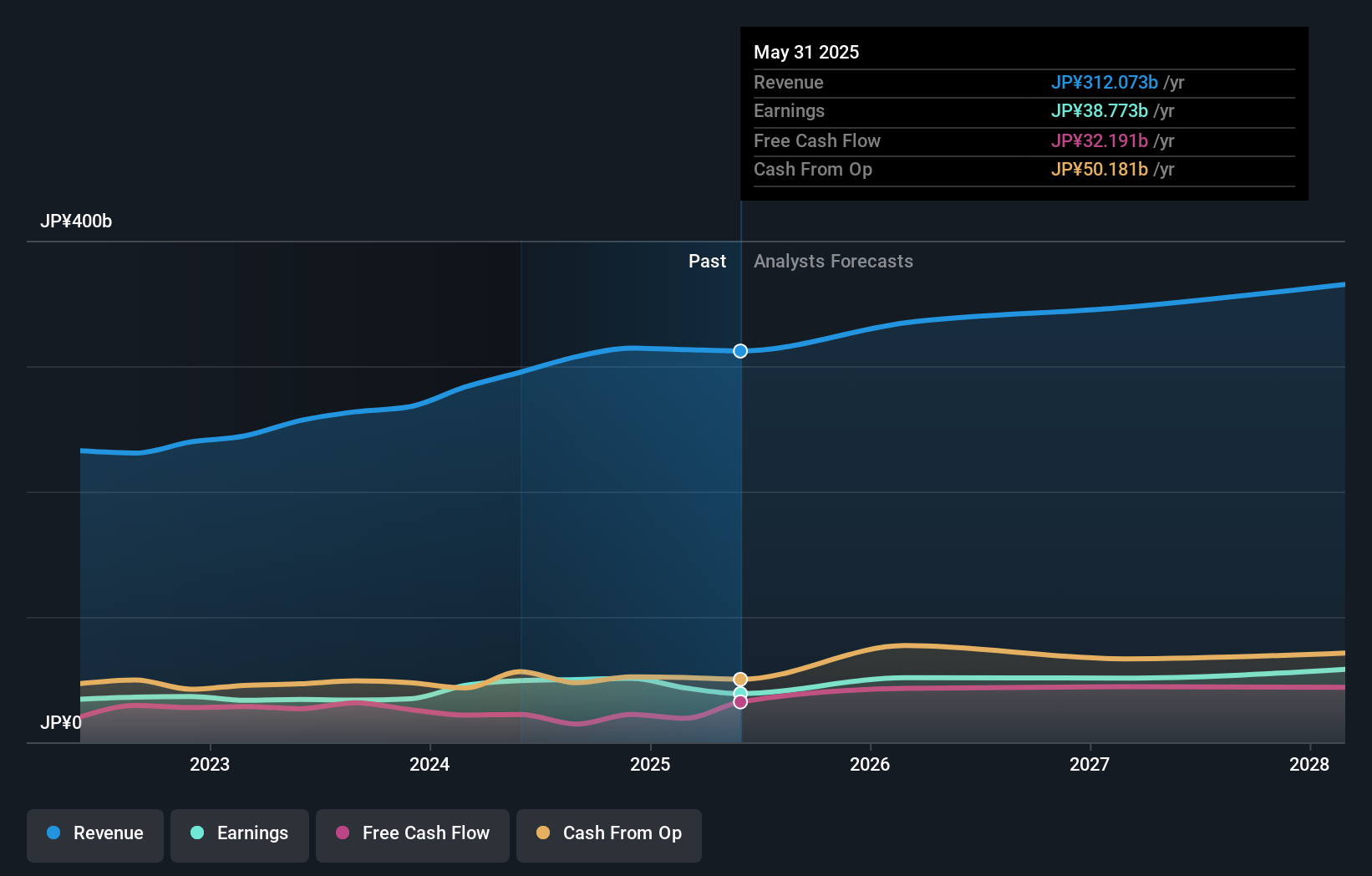

What Is Toho's Investment Narrative?

To be a shareholder in Toho right now, it helps to believe in the company’s ability to sustain its core entertainment and real estate businesses, while carefully managing profitability and capital allocation. The recently completed share buyback offers a near-term signal of management’s commitment to shareholder returns, but its impact on major short-term catalysts is likely limited, given the existing trajectory of steady, though not rapid, earnings and revenue growth. With Toho’s earnings guidance already revised upward prior to the buyback news, much of the optimism appears reflected in consensus expectations. The biggest risks remain the company’s relatively high valuation compared to peers and the broader market, alongside weaker profit margins and slowing earnings momentum. The buyback does reaffirm Toho’s willingness to support its share price, but it doesn’t fundamentally change the risk that future profit growth may lag behind industry peers.

But investors should not overlook concerns about Toho’s expensive valuation compared to the industry. Toho's share price has been on the slide but might be dropping deeper into value territory. Find out whether it's a bargain at this price.Exploring Other Perspectives

Explore another fair value estimate on Toho - why the stock might be worth as much as 7% more than the current price!

Build Your Own Toho Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Toho research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Toho research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Toho's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toho might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9602

Toho

Engages in the motion picture, theatrical production, and real estate businesses in Japan.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor