Advertisement

Fuji Media Holdings (TSE:4676) Valuation in Focus After Buyback, Upgraded Earnings, and Capital Efficiency Targets

Simply Wall St

Reviewed by Simply Wall St

Fuji Media Holdings (TSE:4676) just announced a sizeable stock buyback program, with board approval for repurchasing up to 9.5% of outstanding shares. This move is accompanied by an upgraded full-year earnings forecast and updated long-term capital efficiency targets.

See our latest analysis for Fuji Media Holdings.

Momentum has been building for Fuji Media Holdings throughout the year, with recent buyback news, improved earnings forecasts, and board-level changes all helping to shine a spotlight on the stock. Over the past year, Fuji’s total shareholder return has surged an impressive 107%. The 2025 year-to-date share price return is now just under 100%, reflecting renewed confidence amid decisive management actions and improving fundamentals.

If bold moves like this buyback inspire you, it could be the perfect chance to broaden your search and discover fast growing stocks with high insider ownership

But with shares hovering near analyst price targets after an extraordinary rally, investors may wonder whether all the good news has already been priced in or if there is still a buying opportunity as Fuji Media enters its next phase of growth.

Price-to-Sales of 1.3x: Is it justified?

Fuji Media Holdings is currently trading at a price-to-sales (P/S) ratio of 1.3x, positioning it as good value compared to its peer average of 1.5x. However, it is pricier than the broader JP Media industry average of 0.9x. With the last close at ¥3,408, this makes the company attractive among similar peers but more expensive in the context of the wider market.

The price-to-sales ratio measures how much investors are willing to pay per yen of revenue. For a media company like Fuji, this metric is useful when earnings are negative or volatile, as is currently the case. A lower P/S ratio can indicate the market is not fully appreciating the revenue potential. However, it may also signal caution over future profitability.

Looking further, Fuji’s P/S multiple sits below the peer group but is well above what is typical for the Japanese media sector. The estimated fair P/S ratio is 2.1x, suggesting room for further rerating if the company's fundamentals continue to improve.

Explore the SWS fair ratio for Fuji Media Holdings

Result: Price-to-Sales of 1.3x (UNDERVALUED)

However, risks remain if market enthusiasm fades or if revenue growth underperforms. This could potentially put pressure on shares following such a rapid rally.

Find out about the key risks to this Fuji Media Holdings narrative.

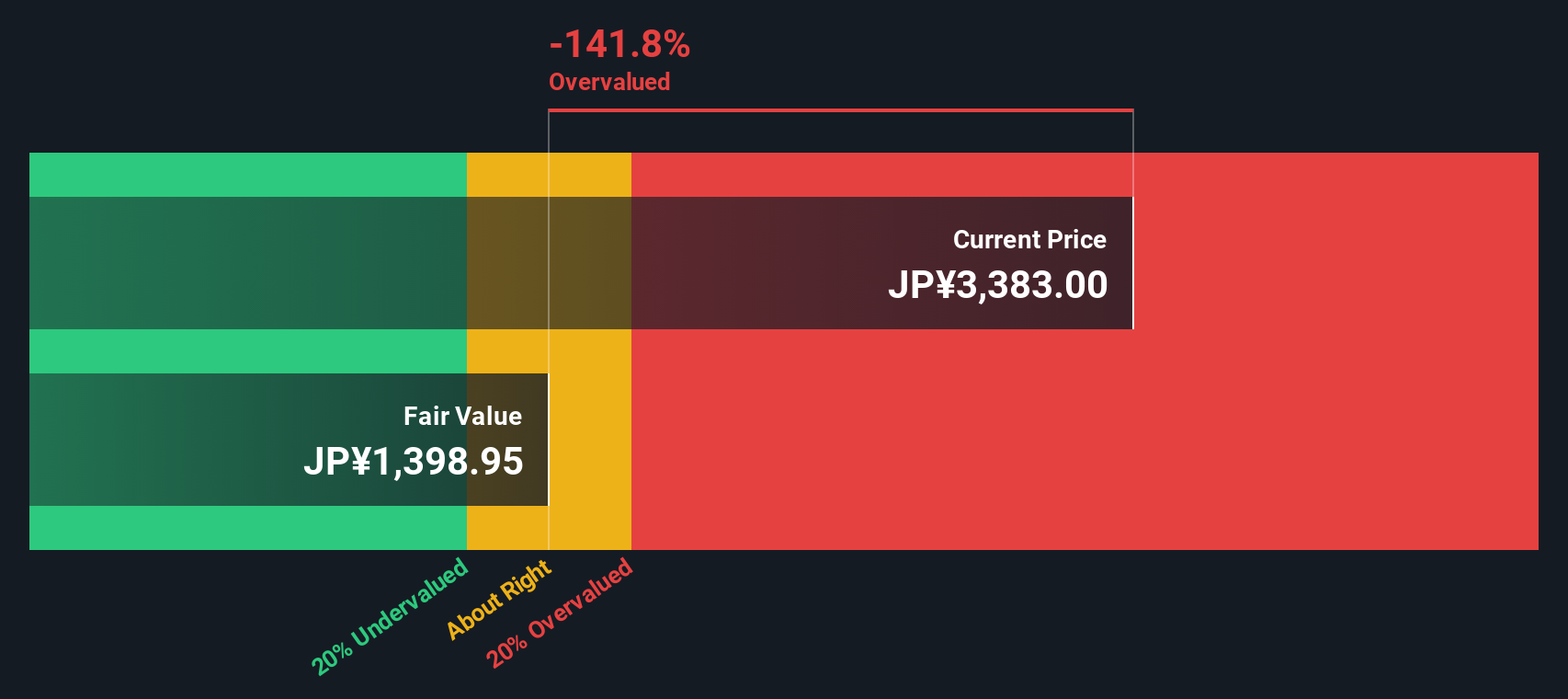

Another View: Discounted Cash Flow Paints a Different Picture

While the price-to-sales ratio points toward undervaluation compared to peers and a favorable fair ratio, our DCF model reaches a less optimistic conclusion. Fuji Media Holdings is trading well above the SWS DCF fair value, which suggests the stock could be overvalued at current prices based on its expected cash flows.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Fuji Media Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 856 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Fuji Media Holdings Narrative

If you have a different perspective or want to dig deeper into Fuji Media Holdings yourself, you can craft your own research-driven narrative in just a few minutes: Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Fuji Media Holdings.

Looking for Your Next Smart Investment?

Why limit yourself to just one opportunity? Grow your potential by tapping into other standout ideas on Simply Wall Street’s powerful Screener. Don’t let these promising options pass you by. See what else could boost your portfolio today.

- Boost your income potential by checking out these 15 dividend stocks with yields > 3% featuring companies offering attractive yields above 3%.

- Ride the wave of artificial intelligence trends through these 25 AI penny stocks and discover which innovators are shaping tomorrow’s tech landscape.

- Strengthen your gains with these 856 undervalued stocks based on cash flows and spot stocks selling for less than their cash flow potential suggests.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4676

Fuji Media Holdings

Through its subsidiaries, engages in the broadcasting activities in Japan.

Reasonable growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor