Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:5713

The Bull Case For Sumitomo Metal Mining (TSE:5713) Could Change Following Higher Dividend and New Earnings Outlook

Simply Wall St

Reviewed by Sasha Jovanovic

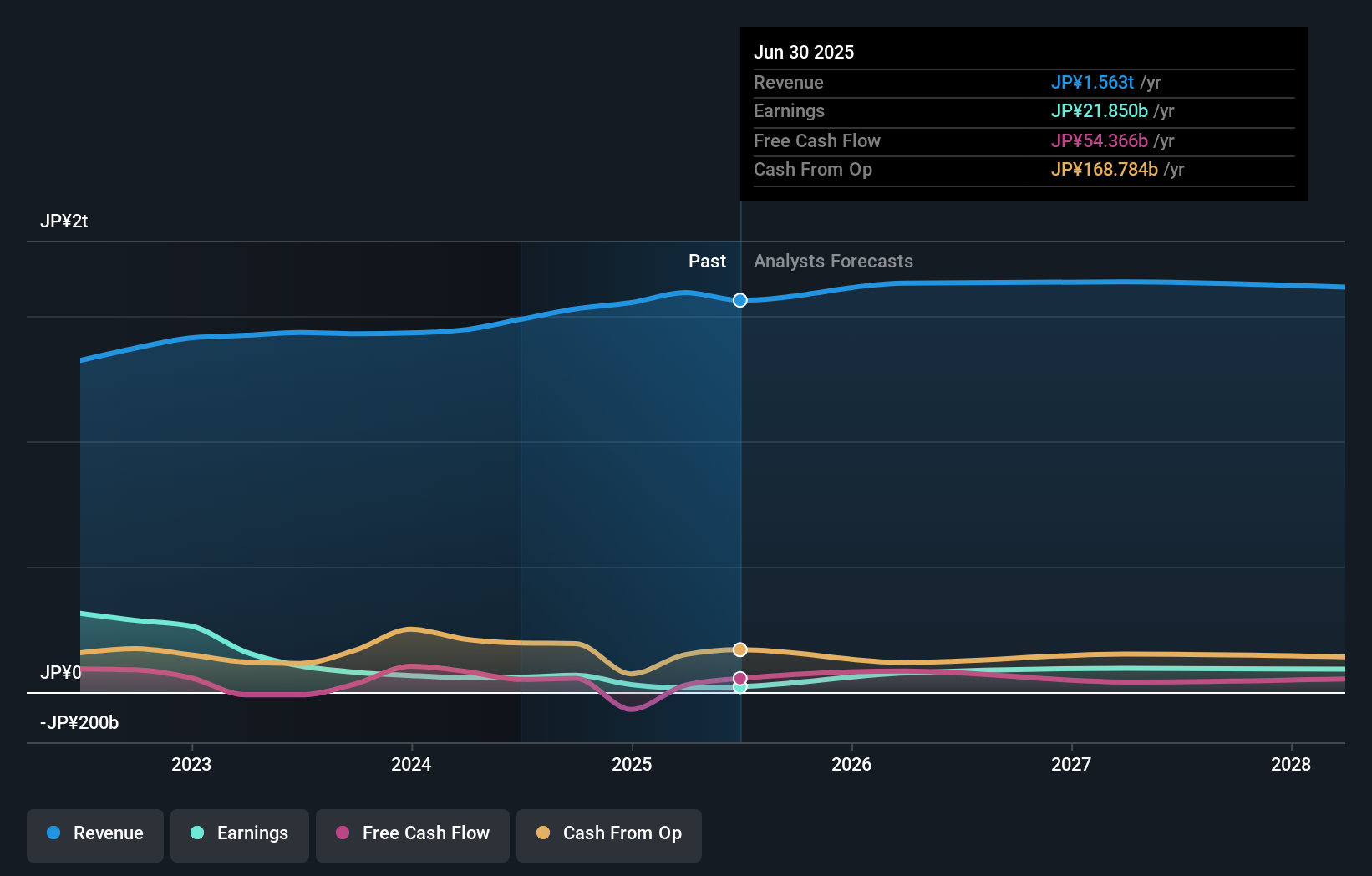

- Sumitomo Metal Mining Co., Ltd. announced an increase in its interim dividend to ¥65.00 per share for the second quarter ended September 30, 2025, up from ¥49.00 a year earlier, and revised its full-year consolidated earnings guidance with projected net sales of ¥1.55 trillion and basic earnings per share of ¥272.66.

- This combination of a higher dividend and updated profit outlook highlights the company's focus on shareholder returns and forward-looking communication.

- We will explore how Sumitomo Metal Mining's increased interim dividend and refreshed earnings forecast enhance its investment narrative.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is Sumitomo Metal Mining's Investment Narrative?

For those considering Sumitomo Metal Mining, the big picture comes down to belief in the company’s ability to deliver value from its mix of resource development, battery materials, and joint venture investments such as the Winu copper-gold project. The recent interim dividend increase and upgraded full-year earnings guidance are positive signals for shareholder returns and reflect strong operational momentum in the near term. While this may ease some immediate concerns about earnings quality and capital allocation, it does not completely resolve key risks highlighted by previous analysis, such as valuation concerns, relatively low return on equity, and questions about the sustainability of earnings growth. The improved guidance could shift short-term catalysts by reigniting market attention, but higher earnings and dividends won’t necessarily address challenges like board turnover, new management, and the stock’s premium to industry peers.

But while dividends are higher, board turnover and management changes still carry weight for investors.

Exploring Other Perspectives

Explore another fair value estimate on Sumitomo Metal Mining - why the stock might be worth just ¥7022!

Build Your Own Sumitomo Metal Mining Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sumitomo Metal Mining research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Sumitomo Metal Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sumitomo Metal Mining's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 38 companies in the world exploring or producing it. Find the list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5713

Sumitomo Metal Mining

Engages in mining, smelting, and refining non-ferrous metals in Japan and internationally.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor