Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:5411

A Fresh Look at JFE Holdings (TSE:5411) Valuation Following New Guidance and Dividend Reduction

Simply Wall St

Reviewed by Simply Wall St

JFE Holdings (TSE:5411) shared fresh guidance for the year ahead and announced a reduction in its dividend payout. These changes are likely to shape how investors think about the stock’s outlook and income profile.

See our latest analysis for JFE Holdings.

JFE Holdings’ announcement comes just as momentum appears to be simmering down. A 1-day share price gain of 2.53% contrasts with a 1-year total shareholder return of -1.97%. Despite recent softness, long-term investors have still seen their positions grow substantially, with the total shareholder return reaching 158.67% over five years.

If you’re weighing where opportunities might emerge next, now’s an ideal time to broaden your search and discover fast growing stocks with high insider ownership

But with updated guidance and a trimmed dividend, is JFE Holdings trading at a price that offers true value? Or has the market already accounted for any future growth in its share price?

Price-to-Earnings of 15.7x: Is it justified?

JFE Holdings currently trades at a price-to-earnings (P/E) ratio of 15.7x, putting it above both its sector peers and the broader industry. The recent close at ¥1,765.5 signals that investors are still pricing in expectations for growth or resilience.

The price-to-earnings multiple is a widely followed valuation yardstick, showing how much markets are willing to pay for each yen of current earnings. For large steel producers like JFE Holdings, the P/E can reflect forecasts around cyclical demand, profit margins, and recovery potential. In JFE’s case, the relatively high multiple raises questions about whether forward-looking earnings justify the premium versus metals and mining peers.

Compared to its peer group’s average of 13.2x and the broader industry’s even lower average of 12.9x, JFE Holdings stands out as expensive. However, notably, it does appear attractively valued against its estimated fair price-to-earnings ratio of 20.9x. This is a level the market could move toward if optimistic forecasts play out.

Explore the SWS fair ratio for JFE Holdings

Result: Price-to-Earnings of 15.7x (OVERVALUED)

However, risks such as muted revenue growth and a steep premium to intrinsic value could challenge expectations for JFE Holdings if market sentiment changes.

Find out about the key risks to this JFE Holdings narrative.

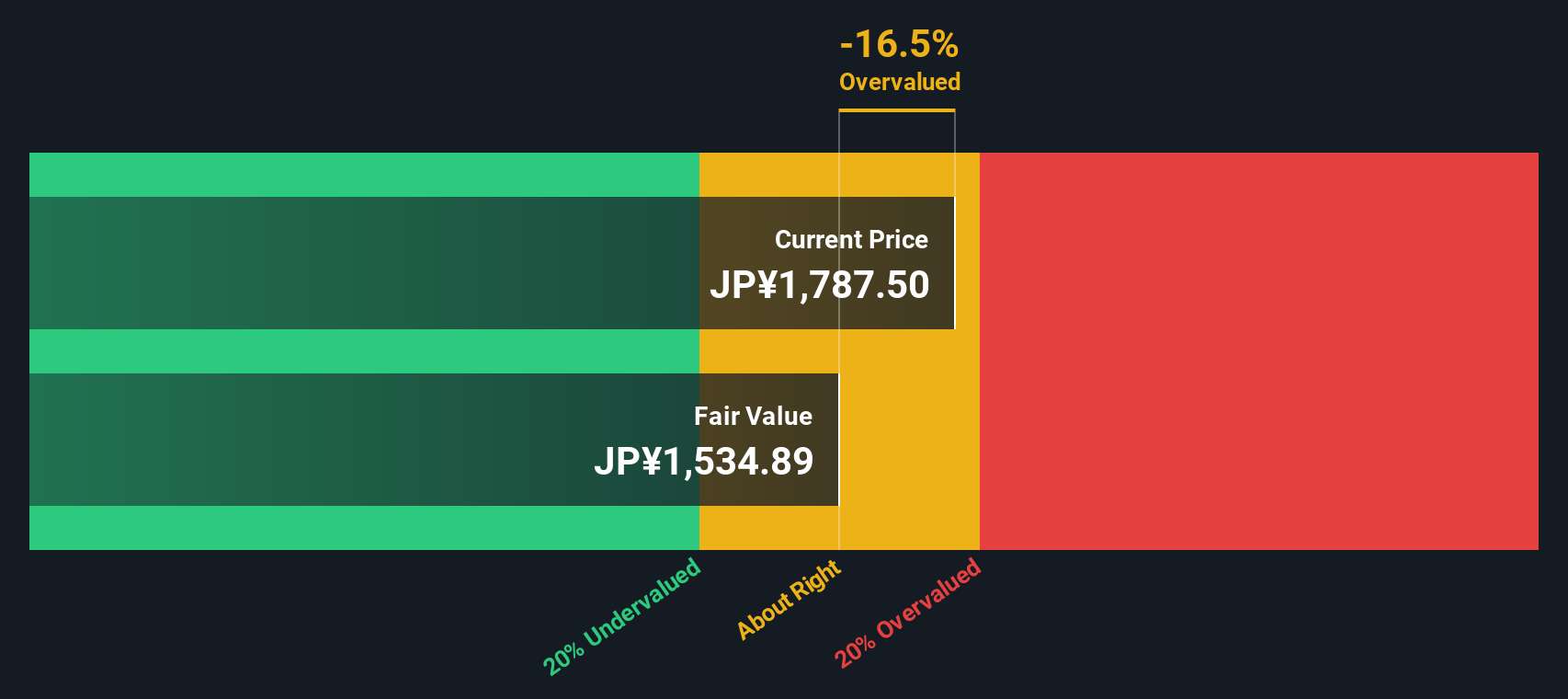

Another View: DCF Model Challenges the Premium

Looking at JFE Holdings through the lens of our DCF model paints a different picture. Despite the market assigning a higher price-to-earnings ratio, the SWS DCF model suggests the stock is currently overvalued, with shares trading about 19% above our estimate of fair value. This stands in stark contrast to the optimism built into current prices. Could longer-term fundamentals force a rethink, or will market confidence persist?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out JFE Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 836 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own JFE Holdings Narrative

If you see the story unfolding differently or want to dig deeper into the numbers yourself, it only takes a few minutes to generate your own perspective. So why not Do it your way?

A great starting point for your JFE Holdings research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

If you want your money to work harder, now’s the ideal time to hunt for exceptional stocks using proven, data-driven screens trusted by top investors.

- Unlock capital growth by targeting these 836 undervalued stocks based on cash flows identified as trading far below their intrinsic value. This could give you a head start on tomorrow’s winners.

- Grow your passive income by selecting these 20 dividend stocks with yields > 3% that deliver reliable yields over 3 percent, built for strong cash flow and financial stability.

- Seize opportunities in game-changing industries by checking out these 25 AI penny stocks on the frontier of artificial intelligence and automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5411

JFE Holdings

Through its subsidiaries, engages in steel, engineering, and trading businesses in Japan and internationally.

Average dividend payer with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor