As global markets react to the recent U.S. election results and economic policy shifts, small-cap stocks have shown significant movement with the Russell 2000 Index leading gains despite not reaching record highs. In this dynamic environment, identifying promising small-cap stocks involves looking for companies that can capitalize on favorable regulatory changes and demonstrate resilience amid fluctuating economic indicators.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Systex | 31.69% | 12.06% | -1.88% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Rami Levi Chain Stores Hashikma Marketing 2006 (TASE:RMLI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Rami Levi Chain Stores Hashikma Marketing 2006 Ltd operates a chain of discount retail stores in Israel and has a market cap of ₪3.15 billion.

Operations: Rami Levi generates revenue primarily from its retail chains, amounting to ₪6.30 billion. The company experiences adjustments to consolidation of -₪30.34 million.

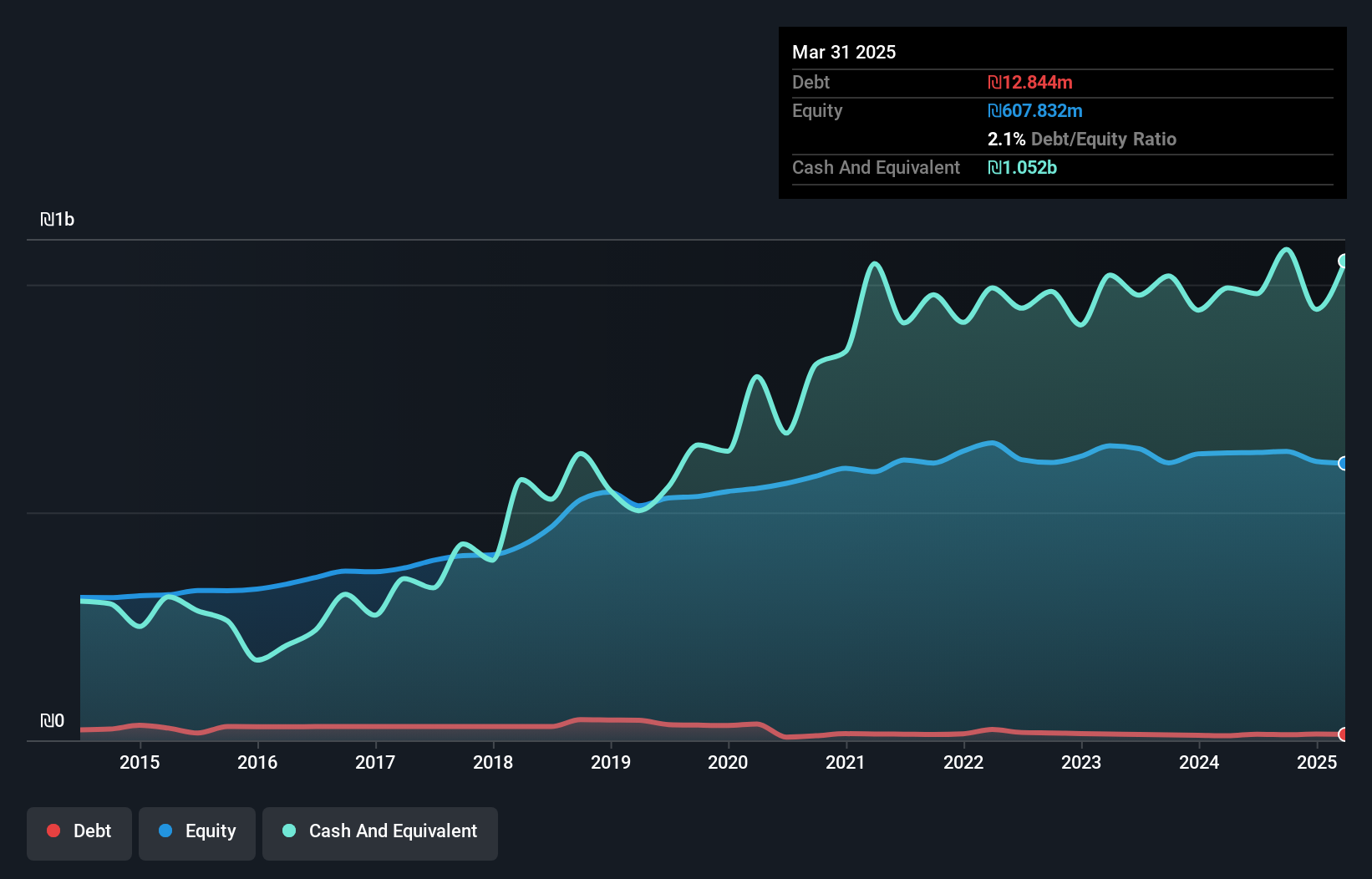

Rami Levi Chain Stores Hashikma Marketing 2006, a notable player in the retail sector, shows a strong financial position with its debt to equity ratio decreasing from 6.5 to 2.1 over five years. Despite earnings growth of 18.8% last year not matching the Consumer Retailing industry's pace, it still achieved a consistent annual earnings increase of 10.4% over five years. The company trades at an attractive valuation, reportedly at 64.6% below estimated fair value and maintains high-quality earnings with EBIT covering interest payments by a factor of 8.3x, underscoring its robust operational efficiency and potential for value appreciation.

- Delve into the full analysis health report here for a deeper understanding of Rami Levi Chain Stores Hashikma Marketing 2006.

Learn about Rami Levi Chain Stores Hashikma Marketing 2006's historical performance.

Nihon Nohyaku (TSE:4997)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nihon Nohyaku Co., Ltd. is engaged in the manufacturing and sale of agrochemicals both domestically in Japan and internationally, with a market cap of ¥55.40 billion.

Operations: The company generates revenue from manufacturing and selling agrochemicals in both domestic and international markets. With a market cap of ¥55.40 billion, its financial performance is influenced by the scale of operations across these regions.

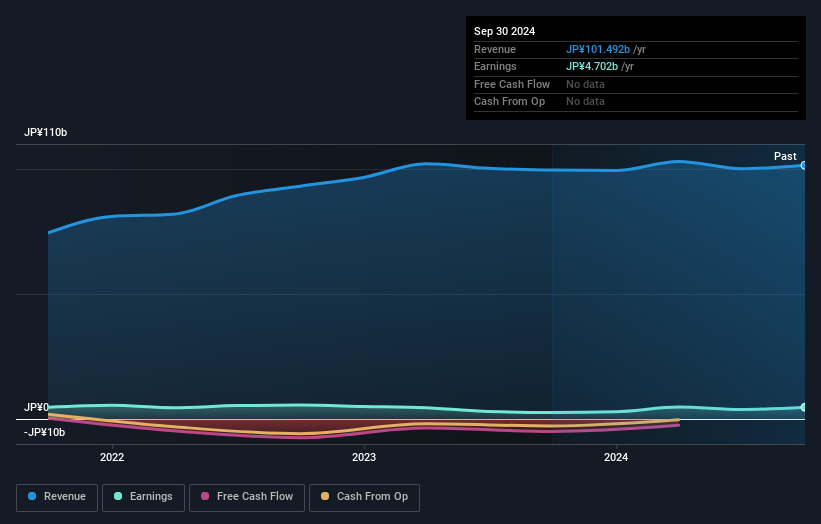

Nihon Nohyaku, a player in the chemicals sector, shows promise with an impressive earnings growth of 80% over the past year, outpacing the industry average of 14%. Its net debt to equity ratio stands at a satisfactory 11.9%, reflecting prudent financial management. The company’s interest payments are well covered by EBIT at 6.6 times coverage, indicating solid operational efficiency. Despite not being free cash flow positive recently, its price-to-earnings ratio of 11.8x remains attractive compared to the JP market's average of 13.4x, suggesting potential value for investors seeking growth opportunities in this niche segment.

- Dive into the specifics of Nihon Nohyaku here with our thorough health report.

Assess Nihon Nohyaku's past performance with our detailed historical performance reports.

SCI Pharmtech (TWSE:4119)

Simply Wall St Value Rating: ★★★★☆☆

Overview: SCI Pharmtech, Inc. focuses on the research and development, manufacture, and sale of active pharmaceutical ingredients, intermediates, and specialty chemicals with a market cap of NT$11.47 billion.

Operations: SCI Pharmtech generates revenue primarily from the sale of active pharmaceutical ingredients, intermediates, and specialty chemicals. The company's financial performance is reflected in its market capitalization of NT$11.47 billion.

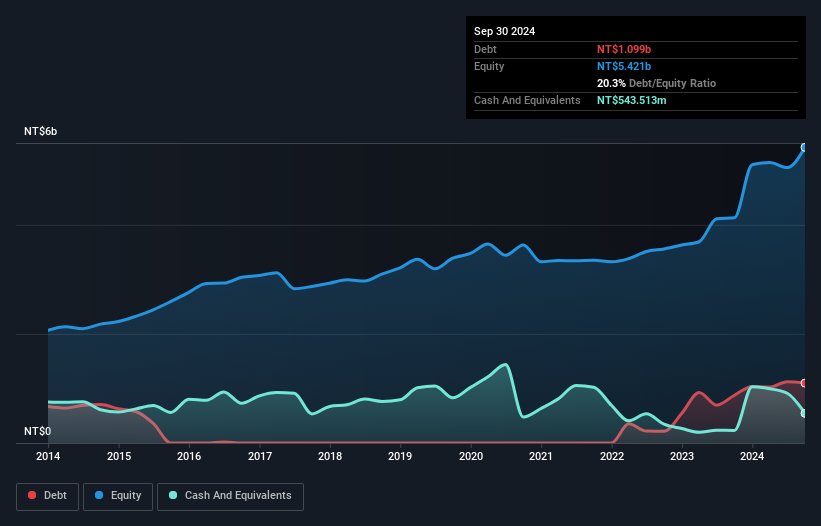

SCI Pharmtech, a dynamic player in the pharmaceuticals sector, has shown impressive growth with a TWD 419.29 million sales figure for Q3 2024, up from TWD 257.85 million a year earlier. Their net income surged to TWD 381.15 million compared to last year's TWD 35.38 million, reflecting strong operational performance and strategic positioning within the industry. The company's earnings per share also climbed significantly to TWD 3.19 from TWD 0.33 previously, indicating robust profitability improvements over the past year despite broader challenges in the market environment and an increased debt-to-equity ratio of around 20% over five years.

- Navigate through the intricacies of SCI Pharmtech with our comprehensive health report here.

Examine SCI Pharmtech's past performance report to understand how it has performed in the past.

Turning Ideas Into Actions

- Dive into all 4666 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:4119

SCI Pharmtech

Engages in the research and development, manufacture, and sale of active pharmaceutical ingredients (API), intermediates, and specialty chemicals.

Adequate balance sheet with acceptable track record.