Advertisement

- Japan

- /

- Household Products

- /

- TSE:7956

Pigeon (TSE:7956): Assessing Valuation Following Strong Third Quarter Growth and Steady Full-Year Outlook

Simply Wall St

Reviewed by Simply Wall St

Pigeon (TSE:7956) recently posted strong third quarter results, highlighting solid year-on-year growth in net sales and earnings. Management kept its full-year forecast unchanged, which signals continued confidence in the company's performance and outlook.

See our latest analysis for Pigeon.

Since the start of 2024, Pigeon’s share price has climbed 25.5 percent, reflecting renewed optimism following strong quarterly numbers and management’s upbeat tone on future growth. However, the five-year total shareholder return remains deeply negative, making it clear that the long-term recovery still has ground to make up.

If Pigeon’s resurgence has you looking for more opportunities beyond the household sector, now is a good time to broaden your search and discover fast growing stocks with high insider ownership

With solid quarterly growth and shares up sharply this year, is Pigeon trading at a discount to its true value? Or has the recent rally already factored in all of its future potential?

Price-to-Earnings of 22.8x: Is it justified?

Pigeon shares currently trade at a price-to-earnings (P/E) ratio of 22.8x, which is higher than both the industry average and its predicted fair P/E. At today’s closing price of ¥1,795.5, investors are effectively paying a substantial premium for each yen of earnings compared to industry peers.

The P/E ratio measures how much investors are willing to pay for a company’s earnings power. In the household products sector, a high P/E often signals expectations for above-average growth, profitability, or business resilience. For Pigeon, the market seems to be pricing in optimism for sustained profit momentum, despite only moderate growth forecasts ahead.

Compared to the fair price-to-earnings estimate of 21.2x, Pigeon's current ratio remains elevated and is also above both the Asian Household Products industry average (20.2x) and the peer average (16.2x). This premium reflects the market’s view that Pigeon’s recent earnings rebound may continue, but also suggests limited room for upside if profit growth disappoints.

Explore the SWS fair ratio for Pigeon

Result: Price-to-Earnings of 22.8x (OVERVALUED)

However, if profit growth slows or the market reduces its optimism, Pigeon's premium valuation could face pressure and this may impact short-term investor sentiment.

Find out about the key risks to this Pigeon narrative.

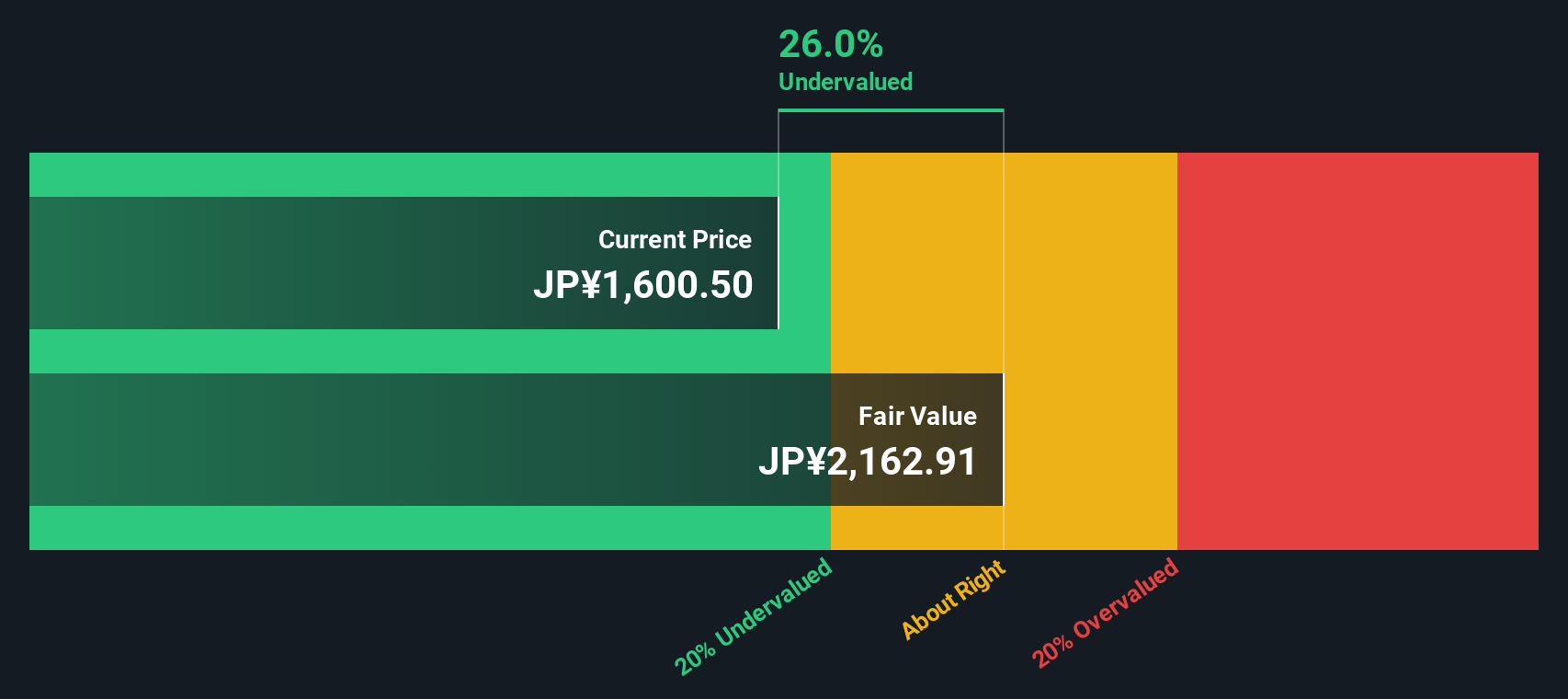

Another View: Discounted Cash Flow Model

While Pigeon looks expensive based on its earnings ratio, our DCF model suggests a different story. According to this approach, shares are trading approximately 17 percent below the estimated fair value. This points to potential undervaluation. Is the market missing something, or is this a case of conflicting signals?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pigeon for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 848 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Pigeon Narrative

If you have a different perspective or enjoy investigating the details firsthand, you can uncover your own insights in just a few minutes, and Do it your way.

A great starting point for your Pigeon research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let your search end here. Now is the perfect moment to energize your portfolio with fresh opportunities using the Simply Wall Street Screener.

- Capture high yields and steady cash flow by checking out these 17 dividend stocks with yields > 3% that consistently reward shareholders with impressive dividends above 3 percent.

- Expand your technology horizon and spot the next innovation wave with these 25 AI penny stocks accelerating breakthroughs in artificial intelligence.

- Seize value plays by targeting these 848 undervalued stocks based on cash flows currently trading below their intrinsic cash-flow estimates for maximum upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7956

Pigeon

Engages in the manufacture, sale, import, and export of baby and child-care products, maternity items, women’s care products, home healthcare products, and nursing care products in Japan and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor