Advertisement

St.Cousair (TSE:2937): One-Off Loss Drives Margin Miss, Heightening Doubt in Recovery Narratives

Simply Wall St

Reviewed by Simply Wall St

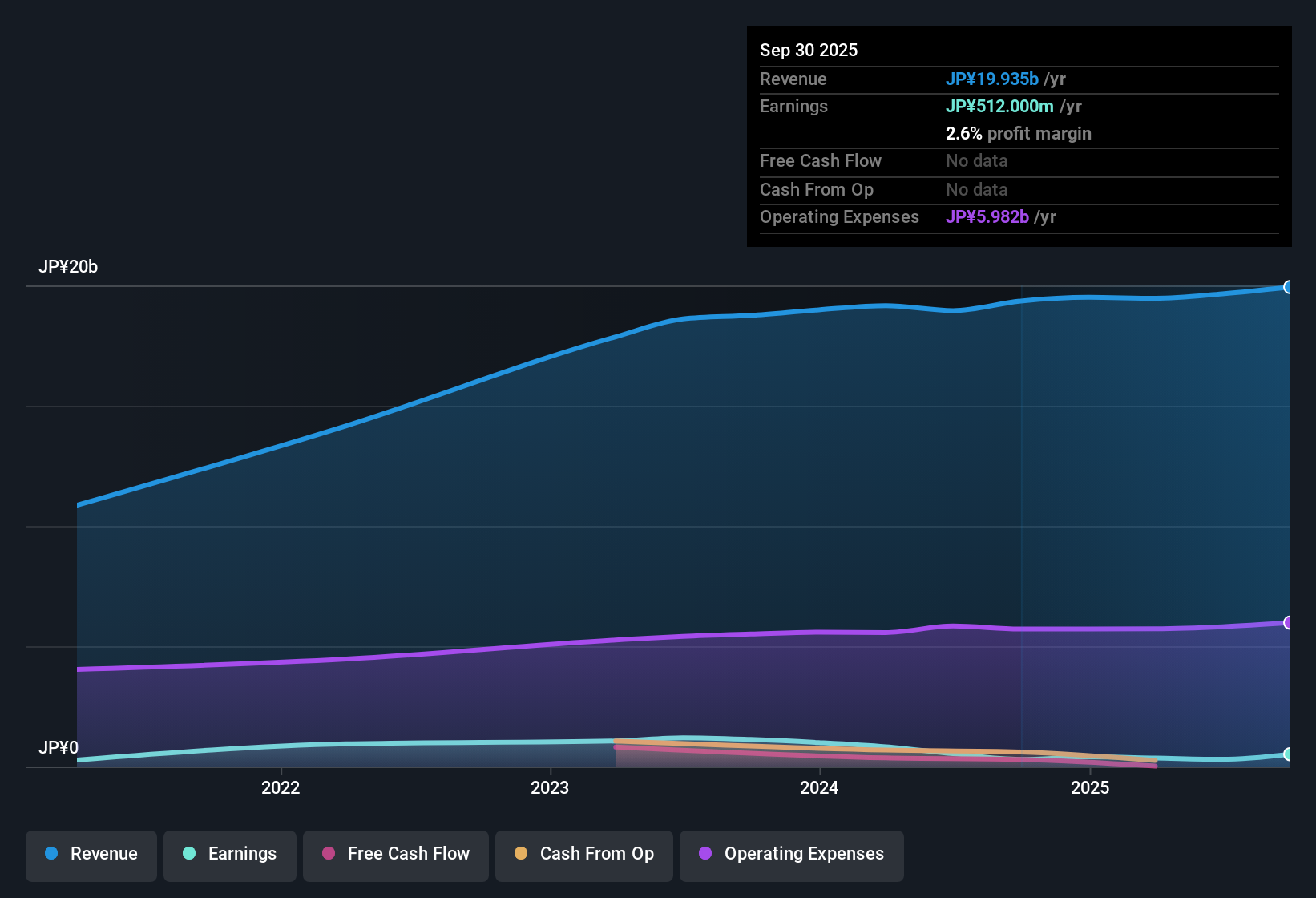

St.Cousair (TSE:2937) saw earnings decline by 13.2% annually over the past five years, with net profit margin falling to 1.5% from 2.8% a year earlier. For the latest period through September 30, 2025, the company was hit by a one-off ¥189.1 million loss, which amplified pressure on profitability. Shares currently trade at ¥1708, notably above the estimated fair value of ¥833.33. This results in a price-to-earnings ratio of 53x, much higher than both the Japanese food industry and peer group averages. Slimmer margins and elevated valuation multiples mean investors are likely to scrutinize future earnings recovery even more closely.

See our full analysis for St.Cousair.The real test is how these numbers stack up against the prevailing market narratives, as some perspectives may be reinforced while others face fresh challenges.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margin Pressure After One-Off Loss

- The latest net profit margin dropped to 1.5%, down from 2.8% the previous year. A notable one-off loss of ¥189.1 million weighed on overall profitability.

- Recent trends point to increasing vulnerability in bottom-line performance. The one-off loss has heightened attention on margin sustainability and earnings quality in the face of sector challenges.

- The ¥189.1 million special loss has intensified the contraction in margins and highlights the risk that profit improvements may be difficult without significant changes in cost or revenue structure.

- Although there is sector momentum toward premiumization, compressed profit margins may make investors cautious until there is clear evidence of a fundamental turnaround.

Profit Growth Trails Peer Standards

- Annual earnings have fallen by 13.2% on average over the past five years, indicating a prolonged struggle compared to peer companies in the broader Japanese food industry.

- The gap between St.Cousair and its peer group has become more pronounced, as the extended decline in profitability makes claims of sector leadership more difficult to support.

- Peers in the Japanese food sector are reporting stronger performance, while St.Cousair’s negative earnings growth raises questions about the potential pace of any recovery.

- The case for above-sector growth lacks clear financial evidence, highlighting how long-running declines in profitability challenge optimism about brand expansion or operational success.

Valuation Stretched Well Above DCF Fair Value

- Shares are trading at ¥1708, which is more than double the DCF fair value of ¥833.33. The price-to-earnings ratio of 53x is well above both the industry average (15.9x) and peer average (11.6x).

- Positive sentiment in news and retail forums points to interest in premium brands, but the magnitude of this valuation premium calls for rapid margin or revenue improvement if there are expectations for a rerating.

- Current valuation multiples may be difficult to justify unless structural improvements result in profit margins closer to sector norms.

- If growth or operational gains do not accelerate, the share price’s wide gap over fair value may sustain caution among value-focused investors.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on St.Cousair's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

With falling profit margins, prolonged earnings declines, and a share price far above fair value, St.Cousair faces heightened risks compared to industry peers.

If overvaluation concerns make you cautious, use these 840 undervalued stocks based on cash flows to target companies where the numbers suggest you are paying less for stronger fundamentals right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2937

St.Cousair

Engages in the manufacture and sale of food products primarily in Japan.

Adequate balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor