Advertisement

Morinaga Milk Industry (TSE:2264): Valuation Insights Following Upgraded Profit Outlook

Simply Wall St

Reviewed by Simply Wall St

Morinaga Milk Industry (TSE:2264) just updated its earnings outlook for the year, raising its operating profit forecast while slightly trimming net sales expectations. This kind of profit revision can draw fresh attention from investors.

See our latest analysis for Morinaga Milk Industry.

Morinaga Milk Industry’s upbeat profit outlook and steady dividend plans come as the share price enjoys strong momentum, notching a year-to-date return of 31.6% and an impressive 1-year total shareholder return of 32.7%. That kind of sustained growth suggests investors are recognizing both recent profit upgrades and longer-term improvements. Momentum here is clearly building, hinting at renewed confidence in the company’s direction.

If Morinaga’s momentum has you curious about other stories of market leadership, now’s a prime opportunity to discover fast growing stocks with high insider ownership

With shares trading near their highs after a strong rally and improved profit guidance, the question becomes whether Morinaga’s growth is fully reflected in the current price or if another buying opportunity is emerging for keen investors.

Price-to-Earnings of 29.9x: Is it justified?

Morinaga Milk Industry is commanding a price-to-earnings (P/E) ratio of 29.9x against its most recent closing price, pushing its valuation notably above both peer and industry averages.

The P/E ratio measures how much investors are willing to pay for each yen of earnings. For companies like Morinaga, which operate in food manufacturing, this metric reflects expectations for future profit growth and perceived stability in earnings.

This elevated multiple suggests the market is pricing in stronger growth or higher quality than peers. However, it is considerably above the JP Food industry P/E of 16.3x and the peer average of 29.5x. Compared to an estimated fair price-to-earnings ratio of 22.2x, the stock currently sits in expensive territory. This level may be difficult to justify without standout future performance.

Explore the SWS fair ratio for Morinaga Milk Industry

Result: Price-to-Earnings of 29.9x (OVERVALUED)

However, slower revenue growth or a change in profit momentum could quickly challenge Morinaga’s premium valuation and investor optimism.

Find out about the key risks to this Morinaga Milk Industry narrative.

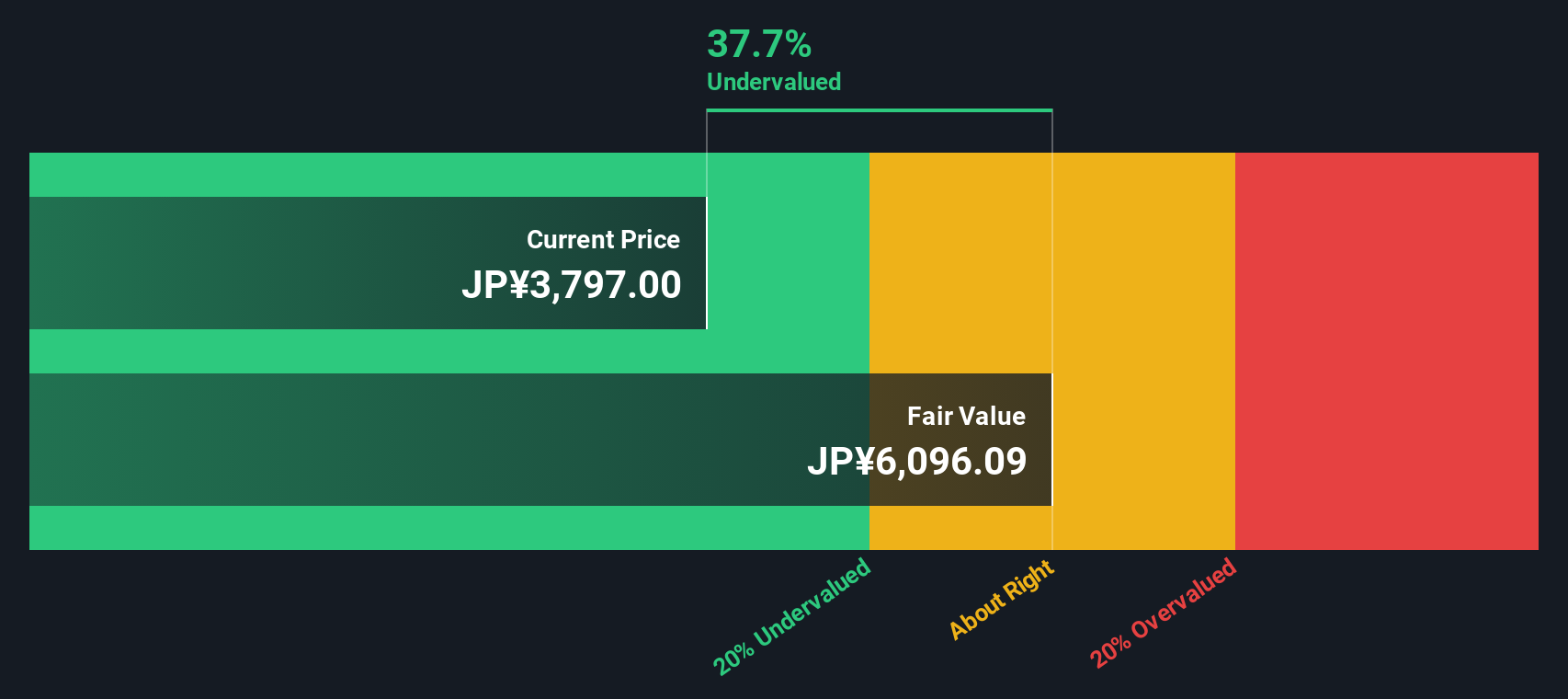

Another Perspective: Discounted Cash Flow Says Undervalued

While the market is assigning Morinaga Milk Industry a high price-to-earnings ratio, our SWS DCF model paints a very different picture. The shares are trading about 38% below the estimated fair value of ¥6,096 per share, which suggests potential undervaluation according to this approach. Which view will the market follow?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Morinaga Milk Industry for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 905 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Morinaga Milk Industry Narrative

If you see the numbers differently or want to dig into Morinaga Milk Industry’s story yourself, shaping your own perspective takes just a few minutes, so why not Do it your way

A great starting point for your Morinaga Milk Industry research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t wait for the next hot tip. Unlock fresh opportunities right now by checking out standout themes that other investors are acting on today.

- Capture high yields and consistent income by starting with these 18 dividend stocks with yields > 3% delivering 3% or greater returns for your portfolio.

- Get ahead of the curve as artificial intelligence transforms industries. Scan these 27 AI penny stocks redefining automation, analytics, and productivity worldwide.

- Capitalize on untapped upside by reviewing these 905 undervalued stocks based on cash flows that the market hasn’t fully noticed yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2264

Morinaga Milk Industry

Engages in the production and sale of various dairy products in Japan and internationally.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor