Advertisement

Feed OneLtd (TSE:2060) Is Paying Out A Larger Dividend Than Last Year

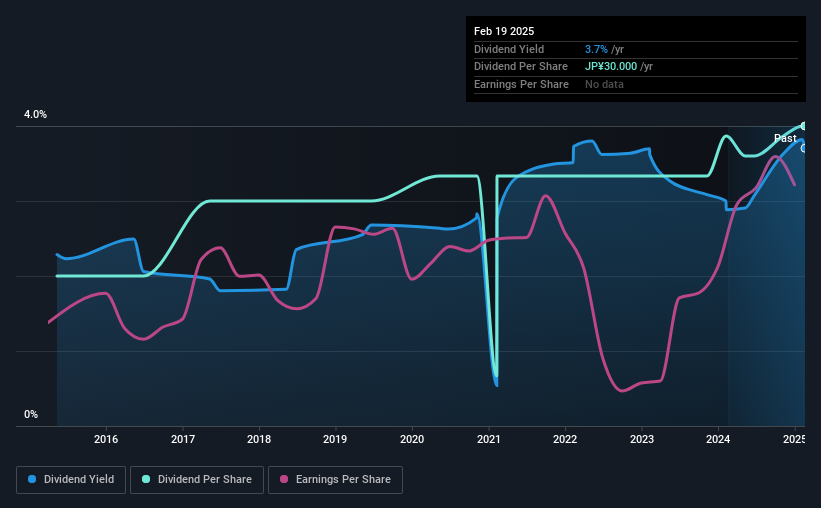

Feed One Co.,Ltd.'s (TSE:2060) dividend will be increasing from last year's payment of the same period to ¥15.00 on 6th of June. This will take the annual payment to 3.7% of the stock price, which is above what most companies in the industry pay.

See our latest analysis for Feed OneLtd

Feed OneLtd's Projected Earnings Seem Likely To Cover Future Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. Feed OneLtd is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

If the trend of the last few years continues, EPS will grow by 10.5% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 19% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2015, the annual payment back then was ¥15.00, compared to the most recent full-year payment of ¥30.00. This works out to be a compound annual growth rate (CAGR) of approximately 7.2% a year over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Feed OneLtd might have put its house in order since then, but we remain cautious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. It's encouraging to see that Feed OneLtd has been growing its earnings per share at 10% a year over the past five years. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

Our Thoughts On Feed OneLtd's Dividend

In summary, while it's always good to see the dividend being raised, we don't think Feed OneLtd's payments are rock solid. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We don't think Feed OneLtd is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Feed OneLtd has 2 warning signs (and 1 which is concerning) we think you should know about. Is Feed OneLtd not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2060

Feed OneLtd

Feed One Co.,Ltd. procures, produces, processes, markets, and sells meat, egg, seafood, and compound feed in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor