Advertisement

- Japan

- /

- Consumer Finance

- /

- TSE:7383

Some Net Protections Holdings, Inc. (TSE:7383) Shareholders Look For Exit As Shares Take 29% Pounding

Net Protections Holdings, Inc. (TSE:7383) shareholders that were waiting for something to happen have been dealt a blow with a 29% share price drop in the last month. Longer-term, the stock has been solid despite a difficult 30 days, gaining 24% in the last year.

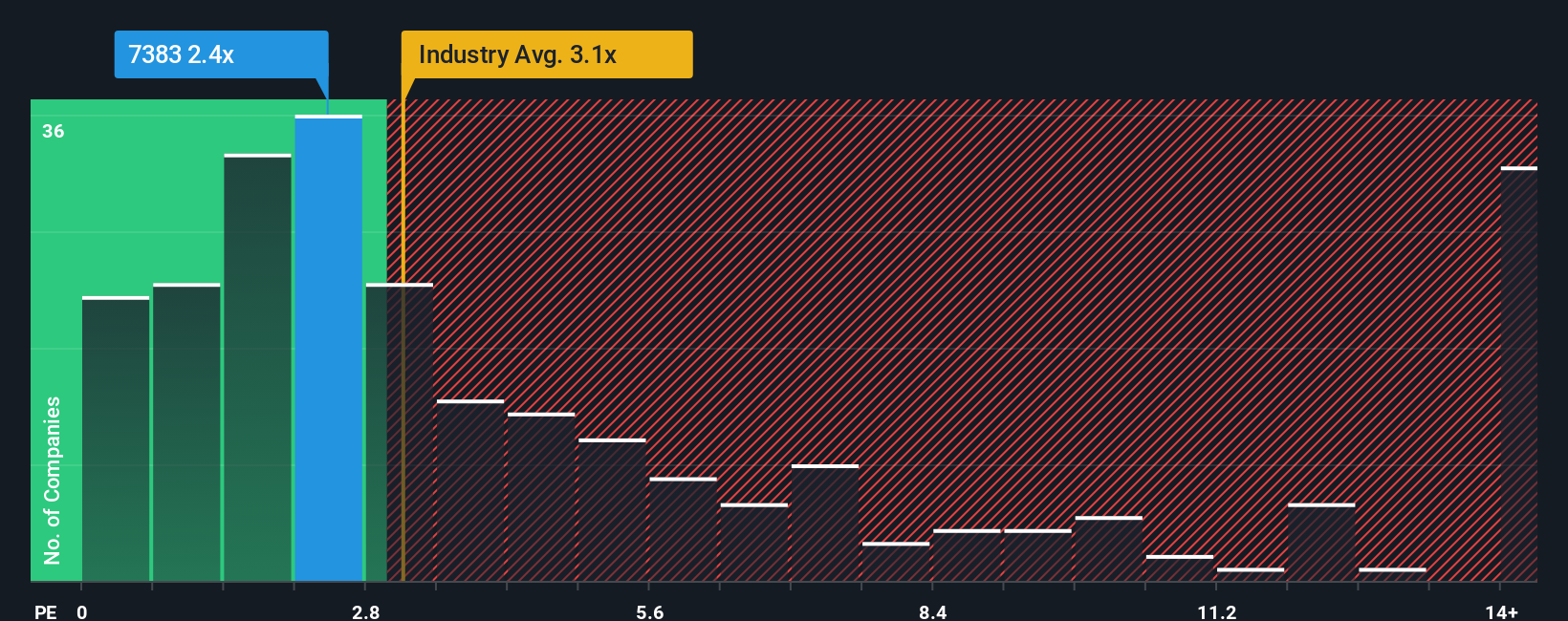

In spite of the heavy fall in price, when almost half of the companies in Japan's Consumer Finance industry have price-to-sales ratios (or "P/S") below 0.9x, you may still consider Net Protections Holdings as a stock probably not worth researching with its 2.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Net Protections Holdings

How Net Protections Holdings Has Been Performing

Recent times have been advantageous for Net Protections Holdings as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Net Protections Holdings will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The High P/S?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Net Protections Holdings' to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 13%. The latest three year period has also seen an excellent 31% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 15% per annum during the coming three years according to the four analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 25% per year, which is noticeably more attractive.

With this in consideration, we believe it doesn't make sense that Net Protections Holdings' P/S is outpacing its industry peers. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does Net Protections Holdings' P/S Mean For Investors?

Despite the recent share price weakness, Net Protections Holdings' P/S remains higher than most other companies in the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It comes as a surprise to see Net Protections Holdings trade at such a high P/S given the revenue forecasts look less than stellar. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

Having said that, be aware Net Protections Holdings is showing 1 warning sign in our investment analysis, you should know about.

If you're unsure about the strength of Net Protections Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Net Protections Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7383

Net Protections Holdings

Provides buy now pay later (BNPL) payment services in Japan and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor