Advertisement

- Japan

- /

- Hospitality

- /

- TSE:9616

Kyoritsu Maintenance (TSE:9616): Evaluating Valuation After Strong Six-Month Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

Kyoritsu Maintenance (TSE:9616) just released its earnings for the six months ending September, posting a 7% rise in net sales and a 6% uptick in operating profit compared to last year.

See our latest analysis for Kyoritsu Maintenance.

Kyoritsu Maintenance’s upbeat results come after a steady climb in total shareholder return, now up 21.1% over the past year. The latest six-month performance adds momentum. Even as the share price has been a little choppy in recent weeks, this suggests investors are starting to recognize the company’s improved fundamentals and long-term growth trajectory.

If you’re wondering what other companies might catch the market’s attention next, this could be a perfect time to broaden your search and discover fast growing stocks with high insider ownership

With these healthy gains and a share price still well below analyst targets, the big question is whether Kyoritsu Maintenance remains undervalued and poised for more upside, or if the market has already priced in its future growth.

Price-to-Earnings of 14.8x: Is it justified?

Kyoritsu Maintenance’s current price-to-earnings (P/E) ratio of 14.8x places the shares well below both industry and peer group averages. This highlights a potential undervaluation at the last close of ¥2,939.

The price-to-earnings ratio is a widely used measure that compares a company's share price to its earnings per share. It reflects how much investors are willing to pay for each unit of profit. For a hospitality company like Kyoritsu Maintenance, this ratio can help investors gauge market expectations for growth and profitability compared to competitors.

Right now, the P/E of 14.8x is significantly lower than the average for the Japanese Hospitality industry, which sits at 23.1x. It is also below the calculated Fair Price-to-Earnings Ratio of 24.7x, a level the market could move towards if sentiment or results continue to improve. This discount suggests the market may be underpricing Kyoritsu’s future earnings potential, giving value-focused investors reason to watch for a possible re-rating.

Explore the SWS fair ratio for Kyoritsu Maintenance

Result: Price-to-Earnings of 14.8x (UNDERVALUED)

However, weaker short-term price momentum or a slowdown in revenue growth could challenge the current undervaluation thesis for Kyoritsu Maintenance.

Find out about the key risks to this Kyoritsu Maintenance narrative.

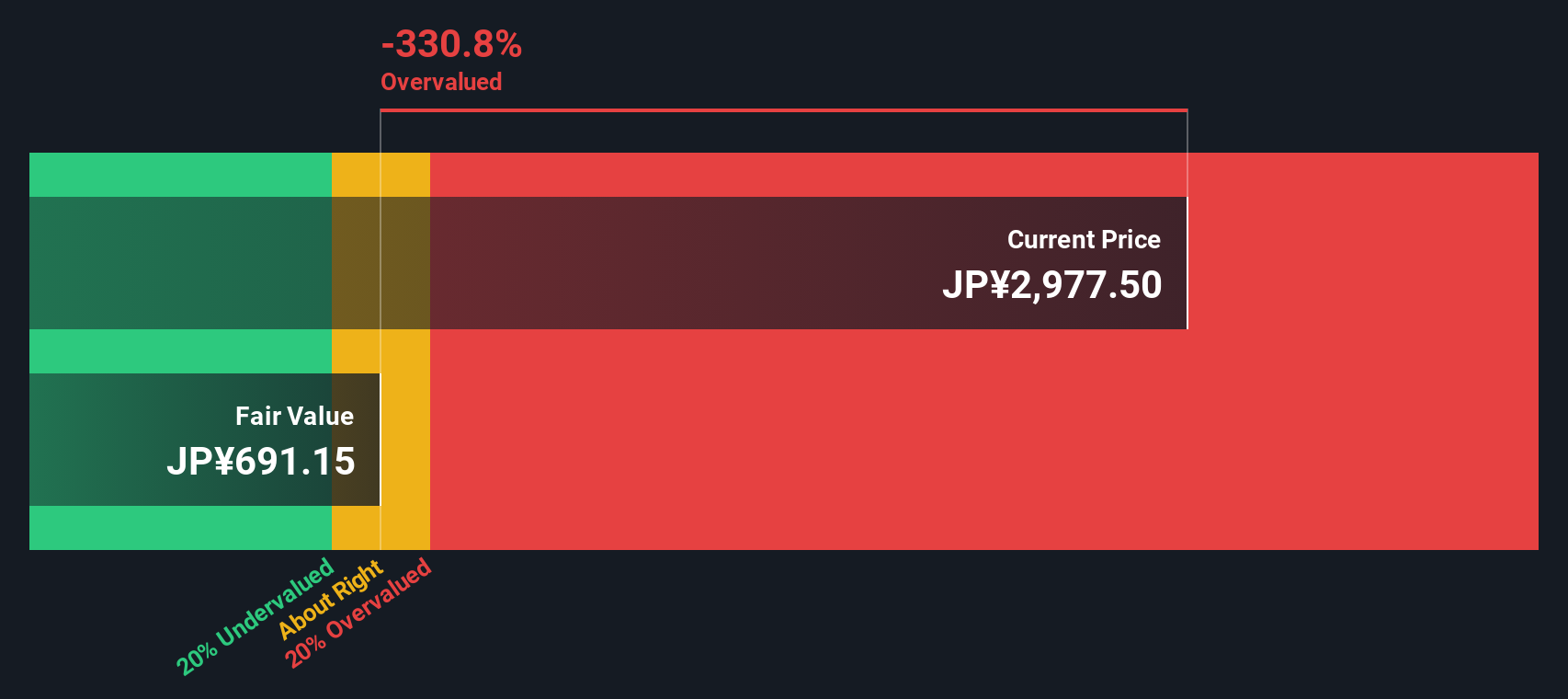

Another View: Discounted Cash Flow Says Shares May Be Overvalued

While the price-to-earnings ratio points to Kyoritsu Maintenance being undervalued, the SWS DCF model presents a more cautious picture. According to this method, the current share price is trading well above our estimate of fair value. So, is the market being too optimistic about the company's cash flow potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kyoritsu Maintenance for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 861 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Kyoritsu Maintenance Narrative

If some of these findings don’t fit your view, or you want to dig deeper yourself, you can easily build your own narrative in just a few minutes with Do it your way.

A great starting point for your Kyoritsu Maintenance research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let unique opportunities pass you by. The right screener could help put your next winning investment within reach. Choose your angle and get started below.

- Spot rising stars early by targeting companies that offer strong financials and future potential using these 3586 penny stocks with strong financials.

- Capitalize on future healthcare breakthroughs as AI transforms patient care and diagnostics with these 32 healthcare AI stocks.

- Boost your passive income strategy with access to reliable businesses that offer attractive payouts through these 17 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kyoritsu Maintenance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9616

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor