Advertisement

Here's Why Nihon Seimitsu (TSE:7771) Has A Meaningful Debt Burden

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Nihon Seimitsu Co., Ltd. (TSE:7771) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

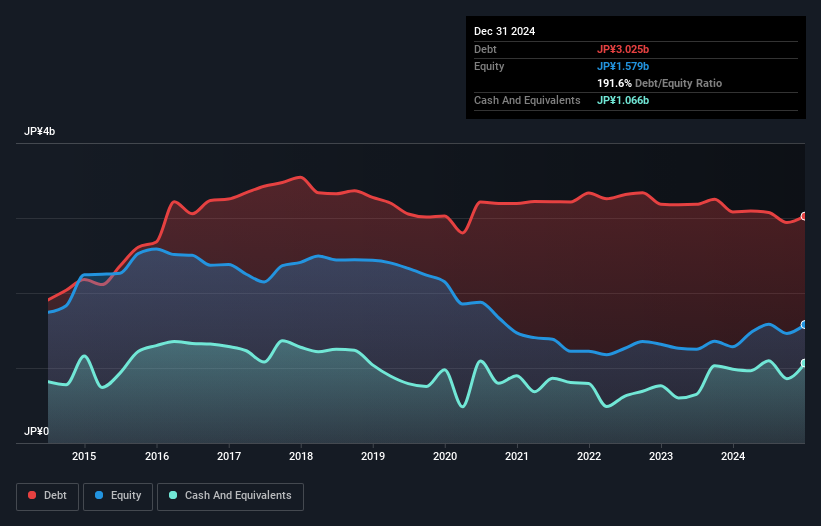

What Is Nihon Seimitsu's Debt?

The chart below, which you can click on for greater detail, shows that Nihon Seimitsu had JP¥3.03b in debt in December 2024; about the same as the year before. However, because it has a cash reserve of JP¥1.07b, its net debt is less, at about JP¥1.96b.

How Healthy Is Nihon Seimitsu's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Nihon Seimitsu had liabilities of JP¥3.90b due within 12 months and liabilities of JP¥476.0m due beyond that. Offsetting these obligations, it had cash of JP¥1.07b as well as receivables valued at JP¥652.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by JP¥2.65b.

This deficit casts a shadow over the JP¥1.39b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Nihon Seimitsu would likely require a major re-capitalisation if it had to pay its creditors today.

See our latest analysis for Nihon Seimitsu

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Nihon Seimitsu has a debt to EBITDA ratio of 3.5 and its EBIT covered its interest expense 5.6 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Notably, Nihon Seimitsu's EBIT launched higher than Elon Musk, gaining a whopping 272% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is Nihon Seimitsu's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend .

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Nihon Seimitsu recorded free cash flow worth a fulsome 92% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

We feel some trepidation about Nihon Seimitsu's difficulty level of total liabilities, but we've got positives to focus on, too. To wit both its conversion of EBIT to free cash flow and EBIT growth rate were encouraging signs. Looking at all the angles mentioned above, it does seem to us that Nihon Seimitsu is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Nihon Seimitsu (of which 2 are a bit unpleasant!) you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Nihon Seimitsu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7771

Nihon Seimitsu

Manufactures and sells watch bands and exterior parts, spectacle frames, and other products in Japan.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor