Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:7916

Mitsumura Printing's (TSE:7916) Earnings Are Built On Soft Foundations

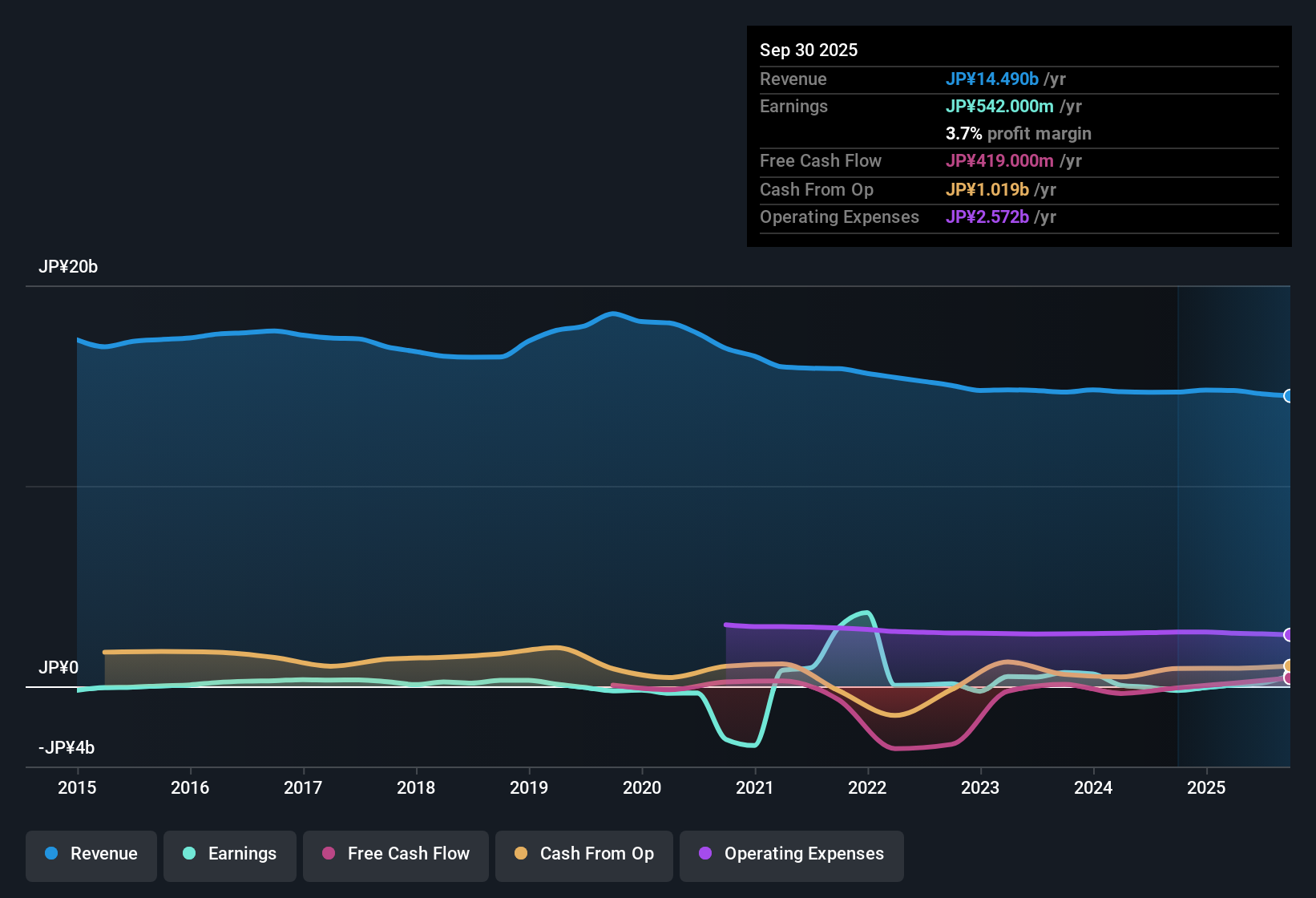

Mitsumura Printing Co., Ltd. (TSE:7916) posted some decent earnings, but shareholders didn't react strongly. Our analysis suggests they may be concerned about some underlying details.

The Impact Of Unusual Items On Profit

To properly understand Mitsumura Printing's profit results, we need to consider the JP¥238m gain attributed to unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. Mitsumura Printing had a rather significant contribution from unusual items relative to its profit to September 2025. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Mitsumura Printing.

An Unusual Tax Situation

Just as we noted the unusual items, we must inform you that Mitsumura Printing received a tax benefit which contributed JP¥178m to the bottom line. It's always a bit noteworthy when a company is paid by the tax man, rather than paying the tax man. We're sure the company was pleased with its tax benefit. And since it previously lost money, it may well simply indicate the realisation of past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. While we think it's good that the company has booked a tax benefit, it does mean that there's every chance the statutory profit will come in a lot higher than it would be if the income was adjusted for one-off factors.

Our Take On Mitsumura Printing's Profit Performance

In its last report Mitsumura Printing received a tax benefit which might make its profit look better than it really is on a underlying level. Furthermore, it also benefitted from a positive unusual item, which boosted the profit result even higher. For all the reasons mentioned above, we think that, at a glance, Mitsumura Printing's statutory profits could be considered to be low quality, because they are likely to give investors an overly positive impression of the company. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. In terms of investment risks, we've identified 2 warning signs with Mitsumura Printing, and understanding these should be part of your investment process.

Our examination of Mitsumura Printing has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7916

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor