As Japan's stock markets experience a downturn, with the Nikkei 225 Index and TOPIX Index both declining, investors are closely watching for opportunities amid easing domestic inflation and shifting monetary policies. In this environment, identifying stocks with strong fundamentals and growth potential becomes crucial for those looking to navigate the complexities of Japan's evolving economic landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Ryoyu Systems | NA | 1.08% | 8.08% | ★★★★★★ |

| Central Forest Group | NA | 7.05% | 14.29% | ★★★★★★ |

| ITOCHU-SHOKUHIN | NA | -0.08% | 12.04% | ★★★★★★ |

| Toukei Computer | NA | 5.46% | 12.14% | ★★★★★★ |

| Maezawa Kasei Industries | 0.81% | 2.01% | 18.42% | ★★★★★★ |

| MIRARTH HOLDINGSInc | 266.33% | 3.00% | -2.40% | ★★★★☆☆ |

| GakkyushaLtd | 23.64% | 5.03% | 18.56% | ★★★★☆☆ |

| Ogaki Kyoritsu Bank | 139.93% | 2.20% | -0.27% | ★★★★☆☆ |

| GENOVA | 0.93% | 33.82% | 30.22% | ★★★★☆☆ |

| Nippon Sharyo | 61.34% | -1.68% | -17.07% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

NJS (TSE:2325)

Simply Wall St Value Rating: ★★★★★★

Overview: NJS Co., Ltd., with a market cap of ¥38.58 billion, operates in the construction consultancy sector both domestically and internationally through its subsidiaries.

Operations: NJS generates revenue primarily from domestic operations, amounting to ¥19.11 billion, and overseas operations contributing ¥3.56 billion. The company's focus on construction consultancy services across these regions forms the core of its revenue streams.

NJS, a promising name in Japan's market, has recently been added to the S&P Global BMI Index. The company is debt-free and shows robust earnings growth of 113.9% over the past year, outpacing its industry peers. Despite this impressive growth, a ¥1.2 billion one-off gain has skewed recent financial results. Trading at 23.7% below estimated fair value suggests potential undervaluation for investors to consider. NJS anticipates net sales of ¥22.5 billion and operating profit of ¥2.9 billion for fiscal year-end 2024, alongside an increased dividend payout from last year’s figures, reflecting confidence in its future prospects.

- Get an in-depth perspective on NJS' performance by reading our health report here.

Gain insights into NJS' historical performance by reviewing our past performance report.

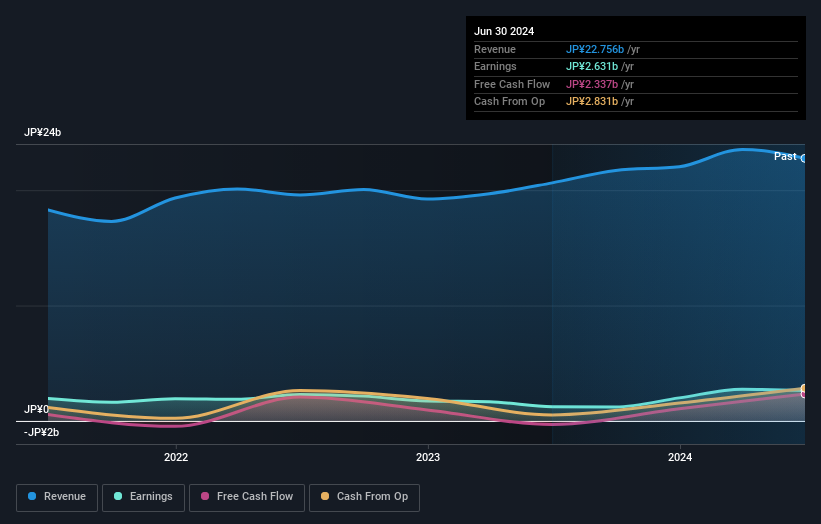

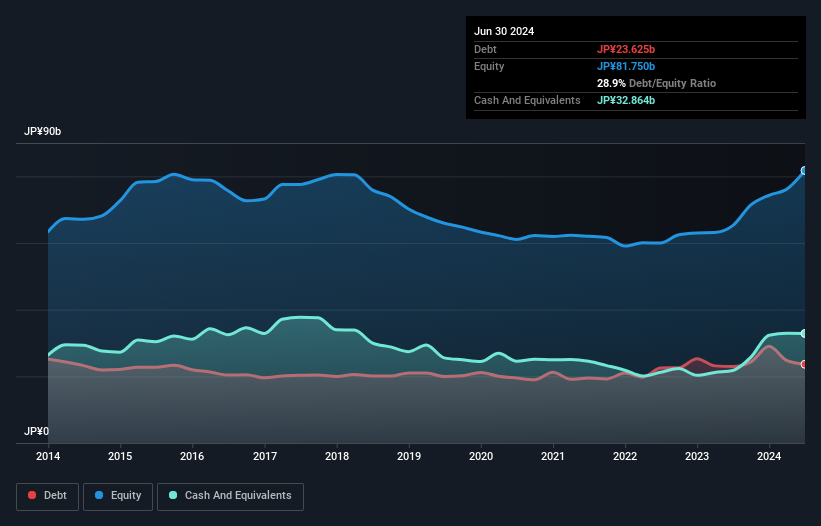

Chugoku Marine Paints (TSE:4617)

Simply Wall St Value Rating: ★★★★★★

Overview: Chugoku Marine Paints, Ltd. is a company that specializes in the production and sale of functional coatings on a global scale, with a market capitalization of ¥104.04 billion.

Operations: Chugoku Marine Paints generates revenue primarily from the sale of functional coatings globally. The company's net profit margin has shown variability, with recent figures indicating a trend worth noting.

Chugoku Marine Paints, a smaller player in the chemicals sector, has shown impressive earnings growth of 117% over the past year, outpacing the industry average of 14%. The company trades at approximately 33% below its estimated fair value, suggesting potential undervaluation. Financially robust, it boasts more cash than total debt and a reduced debt-to-equity ratio from 30.2% to 28.9% over five years. Despite these strengths, future earnings are expected to decline by an average of 11.5% annually for the next three years, which could impact long-term prospects if not addressed strategically.

- Navigate through the intricacies of Chugoku Marine Paints with our comprehensive health report here.

Evaluate Chugoku Marine Paints' historical performance by accessing our past performance report.

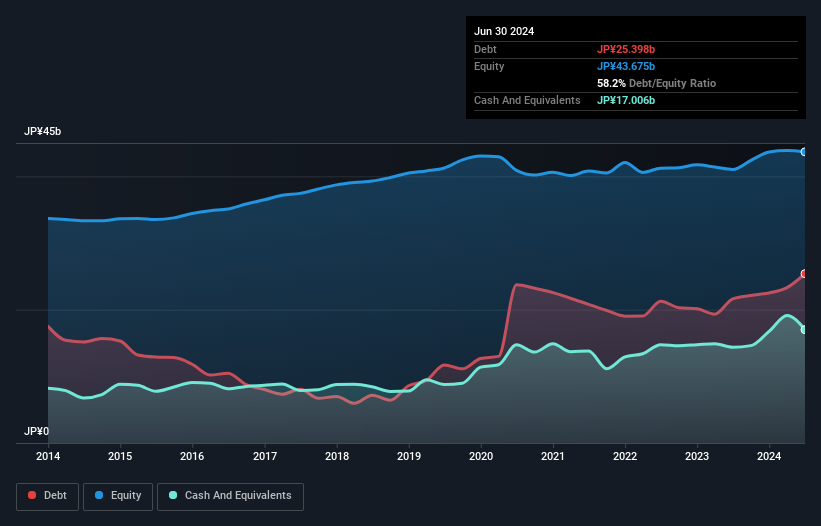

Matsuya Foods Holdings (TSE:9887)

Simply Wall St Value Rating: ★★★★★☆

Overview: Matsuya Foods Holdings Co., Ltd. owns and operates restaurants in Japan, China, and Taiwan, with a market capitalization of ¥130.78 billion.

Operations: The primary revenue stream for Matsuya Foods Holdings comes from its Food and Beverage Business, generating ¥133.77 billion. The company's financial performance is influenced by its operational costs, which impact the overall profitability.

Matsuya Foods Holdings, a nimble player in Japan's hospitality sector, has demonstrated remarkable earnings growth of 658% over the past year, outpacing the industry's average of 28.3%. Despite a significant one-off loss of ¥1.3 billion impacting recent results, the company remains free cash flow positive and its interest payments are well covered by EBIT at 54 times coverage. The net debt to equity ratio stands at a satisfactory 19.2%, although it has risen from 28.4% to 58.2% over five years, suggesting careful monitoring is prudent for future financial stability and growth potential in this dynamic market space.

- Click to explore a detailed breakdown of our findings in Matsuya Foods Holdings' health report.

Explore historical data to track Matsuya Foods Holdings' performance over time in our Past section.

Summing It All Up

- Explore the 722 names from our Japanese Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4617

Flawless balance sheet 6 star dividend payer.