- Japan

- /

- Auto Components

- /

- TSE:6995

Mitsubishi Corporation And 2 Other Leading Dividend Stocks On The Tokyo Exchange

Reviewed by Simply Wall St

Japan's stock markets have recently experienced a downturn, with the Nikkei 225 and TOPIX indices both declining amid uncertainty surrounding the country's upcoming general election and a weakening yen. Despite these challenges, dividend stocks continue to attract attention as potential investment opportunities due to their ability to provide steady income streams in uncertain market conditions.

Top 10 Dividend Stocks In Japan

| Name | Dividend Yield | Dividend Rating |

| Yamato Kogyo (TSE:5444) | 4.30% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.17% | ★★★★★★ |

| Globeride (TSE:7990) | 4.26% | ★★★★★★ |

| Intelligent Wave (TSE:4847) | 3.97% | ★★★★★★ |

| KurimotoLtd (TSE:5602) | 5.48% | ★★★★★★ |

| Innotech (TSE:9880) | 4.73% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.60% | ★★★★★★ |

| FALCO HOLDINGS (TSE:4671) | 6.56% | ★★★★★★ |

| E J Holdings (TSE:2153) | 3.82% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.61% | ★★★★★★ |

Click here to see the full list of 453 stocks from our Top Japanese Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

Okamoto Machine Tool Works (TSE:6125)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Okamoto Machine Tool Works, Ltd. manufactures and sells grinding machines, semiconductor, gear, and casting equipment in Japan and internationally with a market cap of ¥26.99 billion.

Operations: Okamoto Machine Tool Works, Ltd. generates revenue through its manufacturing and sales of grinding machines, semiconductor equipment, gear machinery, and casting equipment both domestically in Japan and on an international scale.

Dividend Yield: 4%

Okamoto Machine Tool Works offers a dividend yield of 3.96%, placing it in the top 25% of Japanese dividend payers. However, its dividends have been volatile and unreliable over the past decade, with periods of significant drops. Despite a low payout ratio of 30%, the company lacks free cash flow to sustain these payments, raising concerns about future stability. Additionally, shareholders experienced dilution in the past year, which may affect long-term value retention.

- Get an in-depth perspective on Okamoto Machine Tool Works' performance by reading our dividend report here.

- Upon reviewing our latest valuation report, Okamoto Machine Tool Works' share price might be too optimistic.

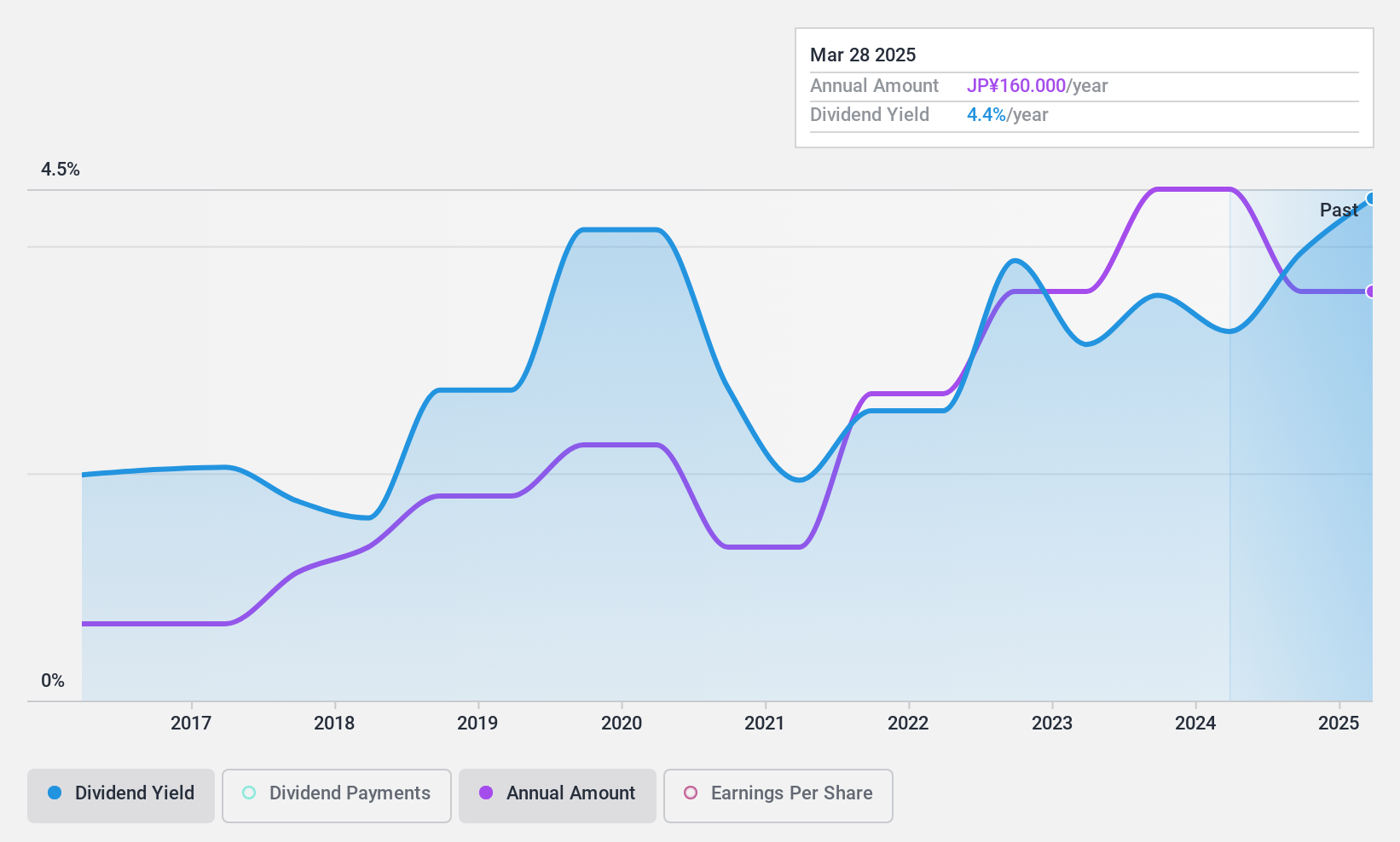

Tokai Rika (TSE:6995)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Tokai Rika Co., Ltd. manufactures and sells human interface systems, controls, security and safety systems, electronics, ornaments, and home devices across Japan, North America, Asia, and internationally with a market cap of ¥182.65 billion.

Operations: Tokai Rika Co., Ltd.'s revenue is primarily derived from its operations in Japan (¥310.81 billion), Asia (¥195.44 billion), and North America (¥170.88 billion).

Dividend Yield: 3.2%

Tokai Rika's dividend yield of 3.24% is below the top 25% in Japan, and its dividends have been volatile over the past decade. Despite this, the company maintains a low payout ratio of 27.9%, indicating dividends are well-covered by earnings and cash flows. Trading significantly below estimated fair value, Tokai Rika presents potential for capital appreciation. Recent earnings growth of 19.9% supports dividend sustainability, although historical instability remains a concern for investors seeking consistent income.

- Unlock comprehensive insights into our analysis of Tokai Rika stock in this dividend report.

- Upon reviewing our latest valuation report, Tokai Rika's share price might be too pessimistic.

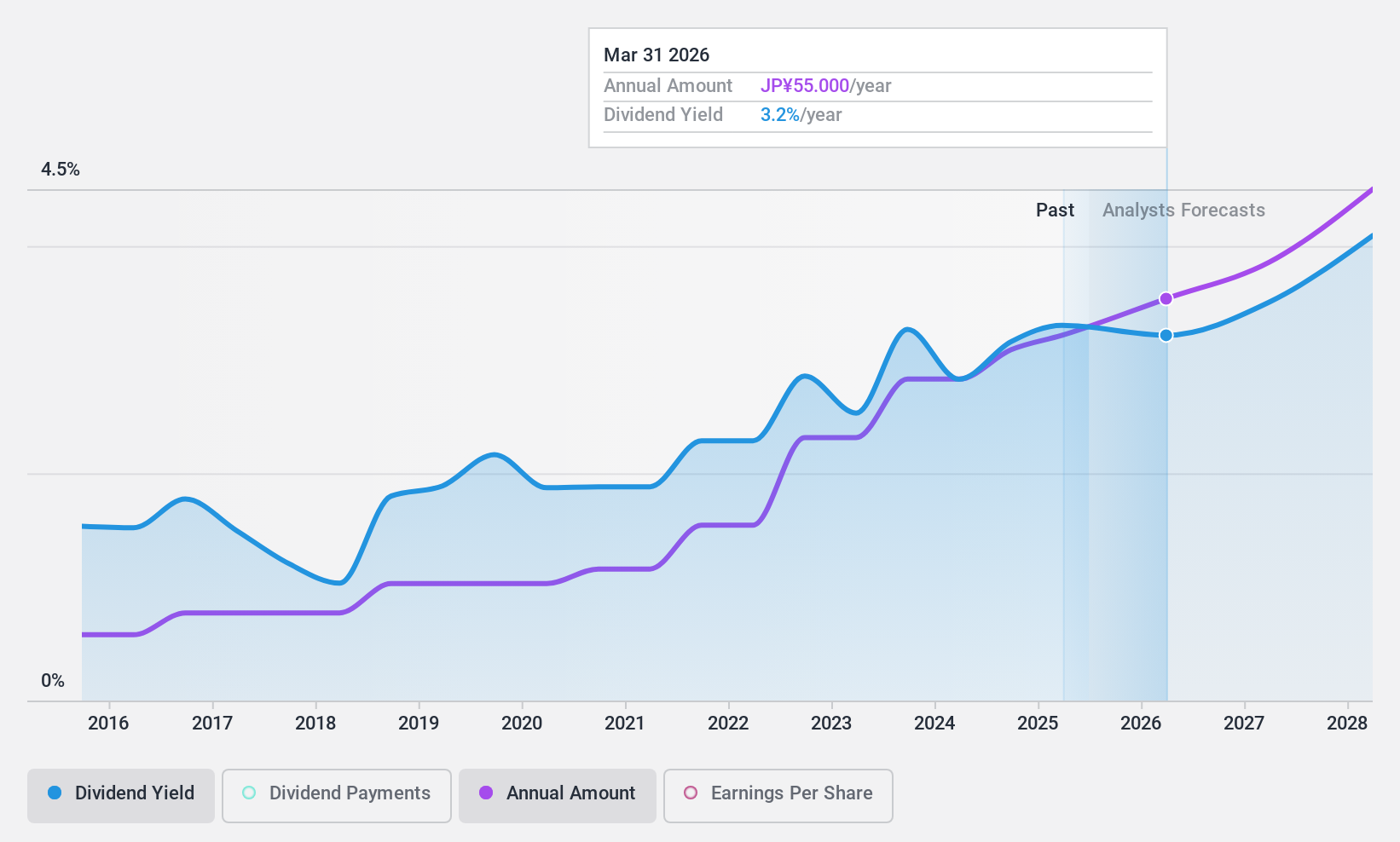

Shin-Etsu PolymerLtd (TSE:7970)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Shin-Etsu Polymer Co., Ltd. is a global manufacturer and seller of polyvinyl chloride (PVC) products, with a market capitalization of ¥129.30 billion.

Operations: Shin-Etsu Polymer Co., Ltd.'s revenue is primarily derived from its Electronic Device segment at ¥26.05 billion, Precision Molded Product segment at ¥50.10 billion, and Living Environment/Living Materials segment at ¥22.43 billion.

Dividend Yield: 3.1%

Shin-Etsu Polymer's dividend yield of 3.13% is below Japan's top quartile, yet dividends have been stable over the past decade. While earnings cover its payout ratio of 45.8%, free cash flow coverage is inadequate, raising sustainability concerns. The company trades at a significant discount to fair value, suggesting potential for capital gains. A recent share buyback program worth ¥900 million may enhance shareholder value but does not directly address dividend coverage issues.

- Delve into the full analysis dividend report here for a deeper understanding of Shin-Etsu PolymerLtd.

- The analysis detailed in our Shin-Etsu PolymerLtd valuation report hints at an deflated share price compared to its estimated value.

Where To Now?

- Navigate through the entire inventory of 453 Top Japanese Dividend Stocks here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tokai Rika might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6995

Tokai Rika

Engages in the manufacture and sale of human interface systems and controls, security systems, safety systems, electronics, ornaments, and home devices in Japan, North America, Asia, and internationally.

Flawless balance sheet with solid track record and pays a dividend.