Advertisement

These 4 Measures Indicate That Esprinet (BIT:PRT) Is Using Debt Reasonably Well

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Esprinet S.p.A. (BIT:PRT) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Esprinet

What Is Esprinet's Debt?

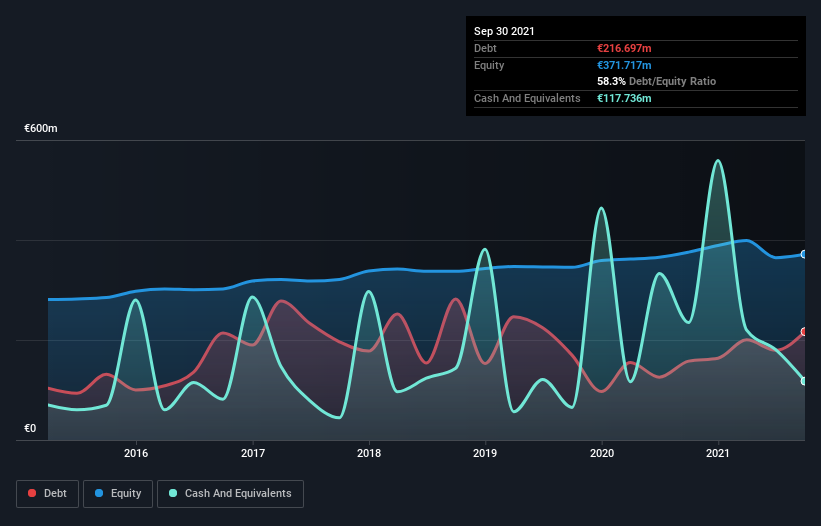

As you can see below, at the end of September 2021, Esprinet had €216.7m of debt, up from €157.8m a year ago. Click the image for more detail. On the flip side, it has €117.7m in cash leading to net debt of about €99.0m.

How Healthy Is Esprinet's Balance Sheet?

According to the last reported balance sheet, Esprinet had liabilities of €804.2m due within 12 months, and liabilities of €225.9m due beyond 12 months. Offsetting these obligations, it had cash of €117.7m as well as receivables valued at €485.0m due within 12 months. So its liabilities total €427.4m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of €575.6m, so it does suggest shareholders should keep an eye on Esprinet's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Esprinet has a low net debt to EBITDA ratio of only 1.3. And its EBIT covers its interest expense a whopping 12.7 times over. So we're pretty relaxed about its super-conservative use of debt. In addition to that, we're happy to report that Esprinet has boosted its EBIT by 40%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Esprinet's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Esprinet actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Esprinet's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But truth be told we feel its level of total liabilities does undermine this impression a bit. Taking all this data into account, it seems to us that Esprinet takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Esprinet (at least 1 which is concerning) , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Esprinet might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:PRT

Esprinet

Engages in the wholesale distribution of information technology (IT) products and consumer electronics in Italy, Spain, Portugal, and rest of Europe.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25367.6% overvalued

68 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

68 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.4% overvalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

YI

yiannisz on Etsy ·

Etsy Stock: Defending Differentiation in a World of Infinite Marketplaces

Fair Value:US$64.4511.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Align Technology ·

Align Technology Stock: Premium Orthodontics in a Cost-Sensitive World

Fair Value:US$154.620.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BO

BonSquid88 on Micron Technology ·

Micron Technology will experience a robust 16.5% revenue growth

Fair Value:US$40021.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

68 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25367.6% overvalued

68 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0225.4% undervalued

1018 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative

Trending Discussion

ST

StevenM on Excellon Resources ·

Interesting analysis, but the price trajectory assumed for the baseline metals is problematic. These assumptions form the foundation for the entire case, and when compared against historical pricing, don’t appear to be grounded in any reasonable precedent. Even accounting for past commodity super-cycles, inflationary periods, or supply constraints, the forecasted pricing for gold, silver, zinc, and lead are well outside what history would suggest is plausible over comparable timeframes. That creates a fragile premise as the conclusions are driven by aggressive inputs rather than underlying market behavior that is realistic. The analysis would be materially stronger if the price assumptions were anchored to historical ranges and prior cycle peaks, with explicit rationale where the model intentionally departs from those patterns. As it stands, the trajectory feels more aspirational than analytical.

1

|1