Advertisement

Persistent Systems Limited (NSE:PERSISTENT) Just Released Its First-Quarter Results And Analysts Are Updating Their Estimates

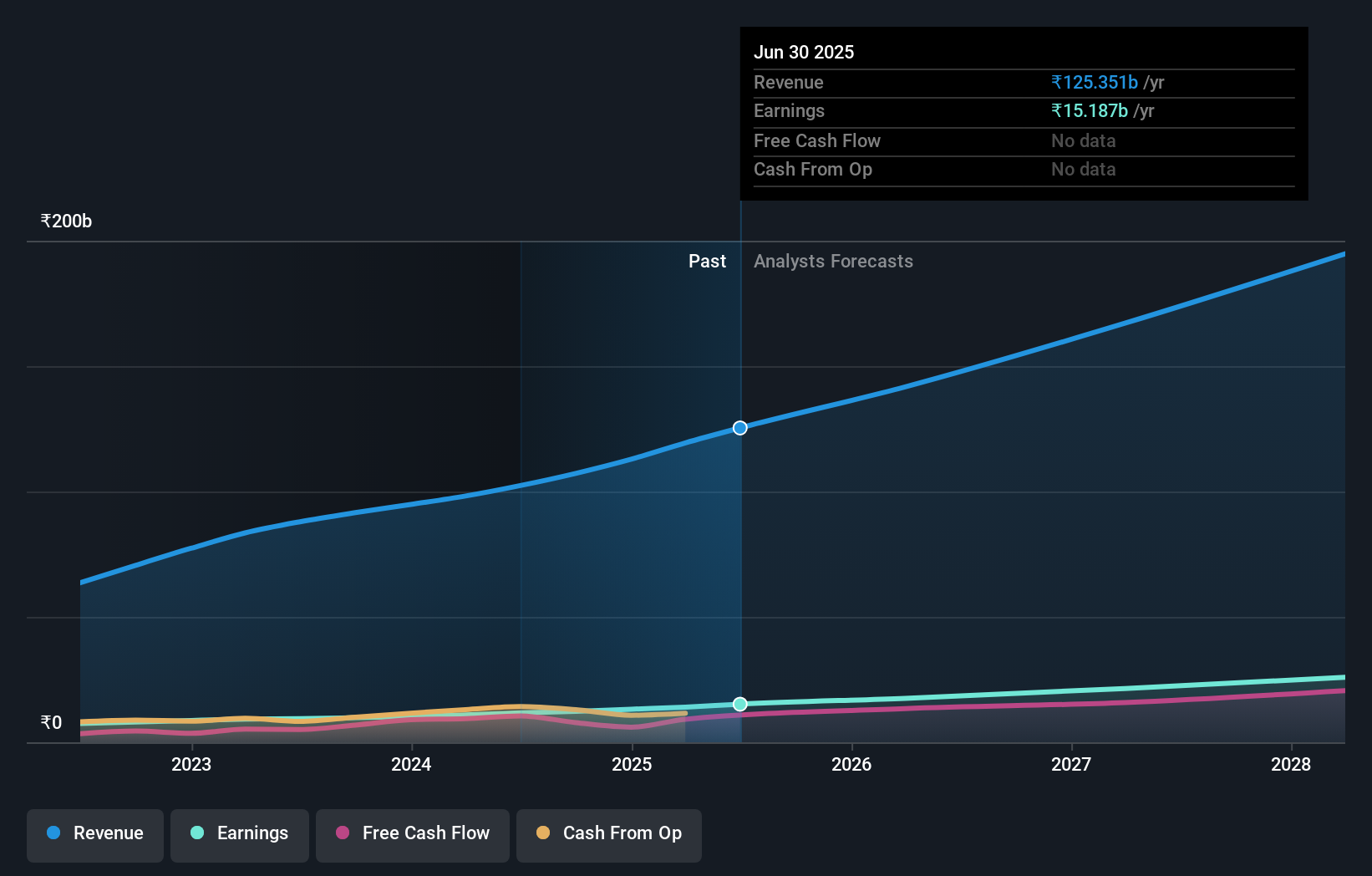

Persistent Systems Limited (NSE:PERSISTENT) shareholders are probably feeling a little disappointed, since its shares fell 7.2% to ₹5,151 in the week after its latest quarterly results. Persistent Systems reported in line with analyst predictions, delivering revenues of ₹33b and statutory earnings per share of ₹27.21, suggesting the business is executing well and in line with its plan. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Persistent Systems after the latest results.

Following the latest results, Persistent Systems' 34 analysts are now forecasting revenues of ₹141.7b in 2026. This would be a meaningful 13% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to step up 11% to ₹113. Before this earnings report, the analysts had been forecasting revenues of ₹142.5b and earnings per share (EPS) of ₹113 in 2026. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

Check out our latest analysis for Persistent Systems

There were no changes to revenue or earnings estimates or the price target of ₹5,848, suggesting that the company has met expectations in its recent result. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Persistent Systems at ₹7,536 per share, while the most bearish prices it at ₹3,675. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Persistent Systems' revenue growth will slow down substantially, with revenues to the end of 2026 expected to display 18% growth on an annualised basis. This is compared to a historical growth rate of 25% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 6.6% annually. So it's pretty clear that, while Persistent Systems' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at ₹5,848, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Persistent Systems going out to 2028, and you can see them free on our platform here..

You can also see our analysis of Persistent Systems' Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PERSISTENT

Persistent Systems

Provides software products, services, and technology solutions in India, North America, and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3448.6% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7100.7% overvalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.650.7% undervalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.0% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

BE

Betsareoff on PROCEPT BioRobotics ·

PROCEPT BioRobotics sees 17.69% revenue growth and aims for 12.94% profit margin

Fair Value:US$25.2617.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on UUE Holdings Berhad ·

UUE Holdings Trading at Deep Value Despite Strong Growth Prospects

Fair Value:RM 0.745.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PU

Pure_Research on Micron Technology ·

Strategic and Financial Blueprint of Micron Technology: Resolving the Memory Wall in the Gen-AI Era

Fair Value:US$2.02k48.3% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.3% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.7% undervalued

57 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.6% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

BE

Betsareoff on PROCEPT BioRobotics ·

I have been an investor in PRCT since before IPO. The wild fluctuations in share price recently make...

0

|0