Stock Analysis

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

In contrast to all that, many investors prefer to focus on companies like HCL Technologies (NSE:HCLTECH), which has not only revenues, but also profits. Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide HCL Technologies with the means to add long-term value to shareholders.

View our latest analysis for HCL Technologies

How Fast Is HCL Technologies Growing Its Earnings Per Share?

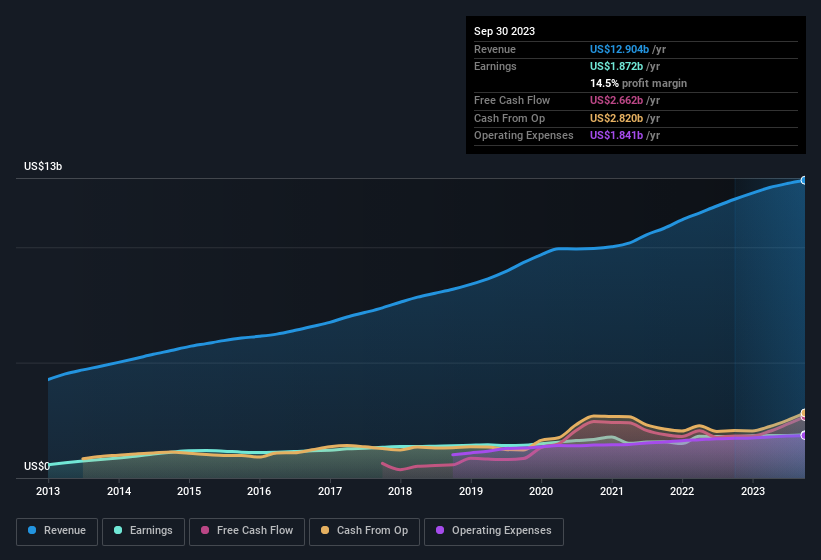

Even with very modest growth rates, a company will usually do well if it improves earnings per share (EPS) year after year. So it's easy to see why many investors focus in on EPS growth. Over the last year, HCL Technologies increased its EPS from US$0.66 to US$0.69. That's a fair increase of 4.6%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. HCL Technologies maintained stable EBIT margins over the last year, all while growing revenue 6.8% to US$13b. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of HCL Technologies' forecast profits?

Are HCL Technologies Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a ₹3.6t company like HCL Technologies. But we do take comfort from the fact that they are investors in the company. To be specific, they have US$3.3b worth of shares. This considerable investment should help drive long-term value in the business. Despite being just 0.09% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Does HCL Technologies Deserve A Spot On Your Watchlist?

One important encouraging feature of HCL Technologies is that it is growing profits. To add an extra spark to the fire, significant insider ownership in the company is another highlight. That combination is very appealing. So yes, we do think the stock is worth keeping an eye on. Even so, be aware that HCL Technologies is showing 1 warning sign in our investment analysis , you should know about...

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're helping make it simple.

Find out whether HCL Technologies is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HCLTECH

HCL Technologies

HCL Technologies Limited offers software development, business process outsourcing, and infrastructure management services worldwide.

Flawless balance sheet established dividend payer.