Advertisement

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. That's why when we briefly looked at Expleo Solutions' (NSE:EXPLEOSOL) ROCE trend, we were very happy with what we saw.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Expleo Solutions is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

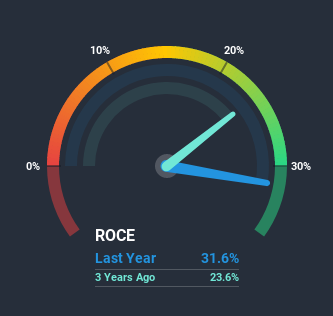

0.32 = ₹591m ÷ (₹2.4b - ₹559m) (Based on the trailing twelve months to September 2020).

Thus, Expleo Solutions has an ROCE of 32%. In absolute terms that's a great return and it's even better than the IT industry average of 11%.

View our latest analysis for Expleo Solutions

Historical performance is a great place to start when researching a stock so above you can see the gauge for Expleo Solutions' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Expleo Solutions, check out these free graphs here.

The Trend Of ROCE

It's hard not to be impressed by Expleo Solutions' returns on capital. The company has consistently earned 32% for the last five years, and the capital employed within the business has risen 55% in that time. With returns that high, it's great that the business can continually reinvest its money at such appealing rates of return. If these trends can continue, it wouldn't surprise us if the company became a multi-bagger.

The Key Takeaway

In short, we'd argue Expleo Solutions has the makings of a multi-bagger since its been able to compound its capital at very profitable rates of return. Yet over the last five years the stock has declined 45%, so the decline might provide an opening. For that reason, savvy investors might want to look further into this company in case it's a prime investment.

Expleo Solutions does have some risks, we noticed 3 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

When trading Expleo Solutions or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Expleo Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:EXPLEOSOL

Expleo Solutions

Primarily provides software validation and verification services to the banking, financial services, and insurance industries worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor