Advertisement

FDC Limited (NSE:FDC) Just Recorded An Earnings Miss And Analysts Are Updating Their Numbers

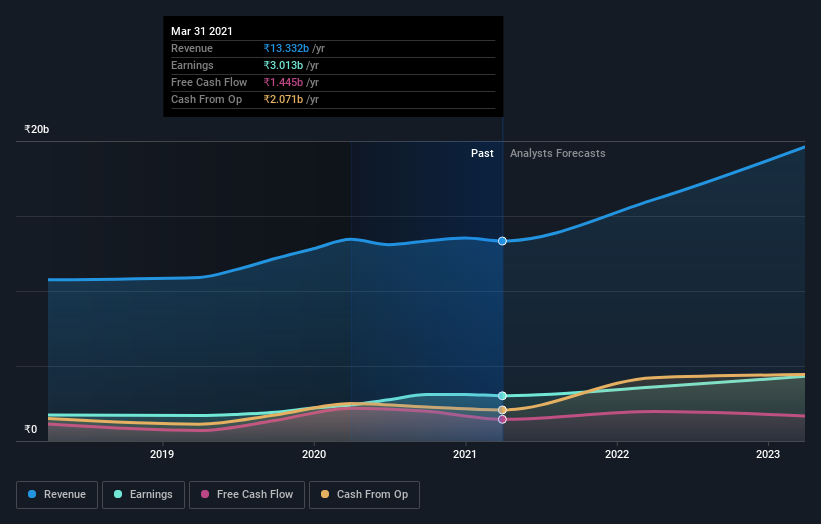

FDC Limited (NSE:FDC) missed earnings with its latest full-year results, disappointing overly-optimistic forecasts. Results look to have been somewhat negative - revenue fell 8.8% short of analyst estimates at ₹13b, and statutory earnings of ₹17.72 per share missed forecasts by 7.7%. This is an important time for investors, as they can track a company's performance in its report, look at what expert is forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimate to see what could be in store for next year.

View our latest analysis for FDC

Taking into account the latest results, the consensus forecast from FDC's lone analyst is for revenues of ₹16.1b in 2022, which would reflect a substantial 21% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to leap 20% to ₹21.30. Yet prior to the latest earnings, the analyst had been anticipated revenues of ₹16.9b and earnings per share (EPS) of ₹22.50 in 2022. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a minor downgrade to earnings per share estimates.

What's most unexpected is that the consensus price target rose 9.3% to ₹470, strongly implying the downgrade to forecasts is not expected to be more than a temporary blip.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that FDC's rate of growth is expected to accelerate meaningfully, with the forecast 21% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 6.9% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 10% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analyst also expect FDC to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analyst downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Regrettably, they also downgraded their revenue estimates, but the latest forecasts still imply the business will grow faster than the wider industry. There was also a nice increase in the price target, with the analyst clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

You can also see our analysis of FDC's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

When trading FDC or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:FDC

FDC

Manufactures and trades in pharmaceutical products in India, the United States, and internationally.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor