Stock Analysis

MPS Limited Just Beat EPS By 8.3%: Here's What Analysts Think Will Happen Next

MPS Limited (NSE:MPSLTD) just released its latest quarterly results and things are looking bullish. Results were good overall, with revenues beating analyst predictions by 2.3% to hit ₹1.1b. Statutory earnings per share (EPS) came in at ₹7.47, some 8.3% above whatthe analyst had expected. This is an important time for investors, as they can track a company's performance in its report, look at what expert is forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analyst has changed their mind on MPS after the latest results.

View our latest analysis for MPS

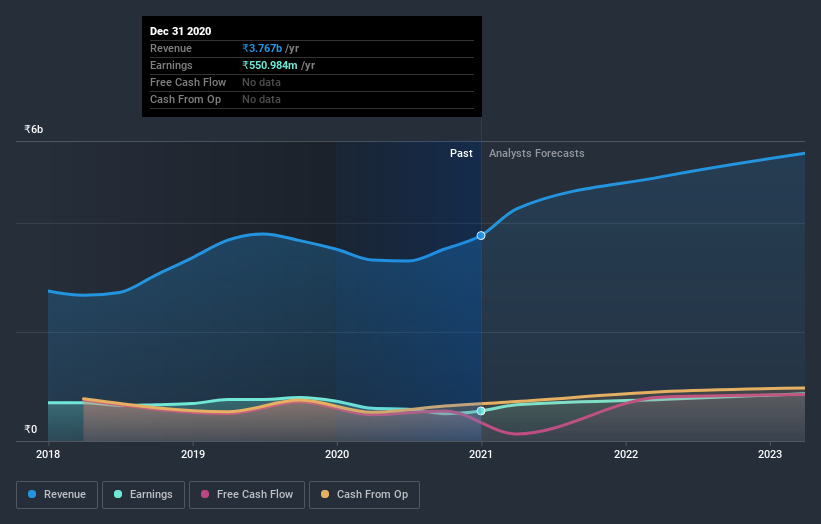

Taking into account the latest results, the current consensus from MPS' sole analyst is for revenues of ₹4.26b in 2021, which would reflect a solid 13% increase on its sales over the past 12 months. Per-share earnings are expected to jump 23% to ₹36.70. Yet prior to the latest earnings, the analyst had been anticipated revenues of ₹4.20b and earnings per share (EPS) of ₹33.00 in 2021. Although the revenue estimates have not really changed, we can see there's been a nice increase in earnings per share expectations, suggesting that the analyst has become more bullish after the latest result.

The consensus price target rose 67% to ₹550, suggesting that higher earnings estimates flow through to the stock's valuation as well.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the MPS' past performance and to peers in the same industry. The analyst is definitely expecting MPS' growth to accelerate, with the forecast 13% growth ranking favourably alongside historical growth of 7.9% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 15% next year. MPS is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around MPS' earnings potential next year. Happily, there were no real changes to sales forecasts, with the business still expected to grow in line with the overall industry. There was also a nice increase in the price target, with the analyst clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on MPS. Long-term earnings power is much more important than next year's profits. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

You should always think about risks though. Case in point, we've spotted 1 warning sign for MPS you should be aware of.

If you decide to trade MPS, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether MPS is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:MPSLTD

MPS

Provides platforms and services for content creation, full-service production, and distribution to the publishers, learning companies, corporate institutions, libraries, and content aggregators in India, Europe, the United States, and internationally.

Flawless balance sheet with high growth potential.