Advertisement

GTPL Hathway's (NSE:GTPL) Shareholders Will Receive A Bigger Dividend Than Last Year

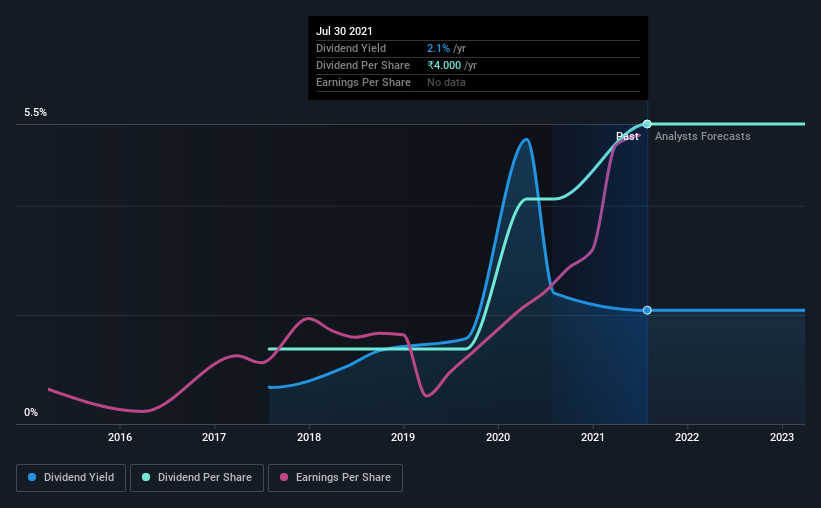

GTPL Hathway Limited (NSE:GTPL) has announced that it will be increasing its dividend on the 26th of September to ₹4.00. This takes the dividend yield from 2.1% to 2.1%, which shareholders will be pleased with.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that GTPL Hathway's stock price has increased by 48% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for GTPL Hathway

GTPL Hathway's Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. However, prior to this announcement, GTPL Hathway's dividend was comfortably covered by both cash flow and earnings. As a result, a large proportion of what it earned was being reinvested back into the business.

EPS is set to fall by 4.6% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio could be 36%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

GTPL Hathway Doesn't Have A Long Payment History

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 4 years, which isn't that long in the grand scheme of things. The dividend has gone from ₹1.00 in 2017 to the most recent annual payment of ₹4.00. This means that it has been growing its distributions at 41% per annum over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see GTPL Hathway has been growing its earnings per share at 87% a year over the past five years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

We Really Like GTPL Hathway's Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. If earnings do fall over the next 12 months, the dividend could be buffeted a little bit, but we don't think it should cause too much of a problem in the long term. All of these factors considered, we think this has solid potential as a dividend stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for GTPL Hathway that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

If you’re looking to trade GTPL Hathway, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:GTPL

GTPL Hathway

Provides digital cable television and broadband services in India.

Average dividend payer with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor