Advertisement

Here's Why We Think Tainwala Chemicals and Plastics (India) (NSE:TAINWALCHM) Might Deserve Your Attention Today

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

In contrast to all that, many investors prefer to focus on companies like Tainwala Chemicals and Plastics (India) (NSE:TAINWALCHM), which has not only revenues, but also profits. Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Tainwala Chemicals and Plastics (India) with the means to add long-term value to shareholders.

See our latest analysis for Tainwala Chemicals and Plastics (India)

Tainwala Chemicals and Plastics (India)'s Improving Profits

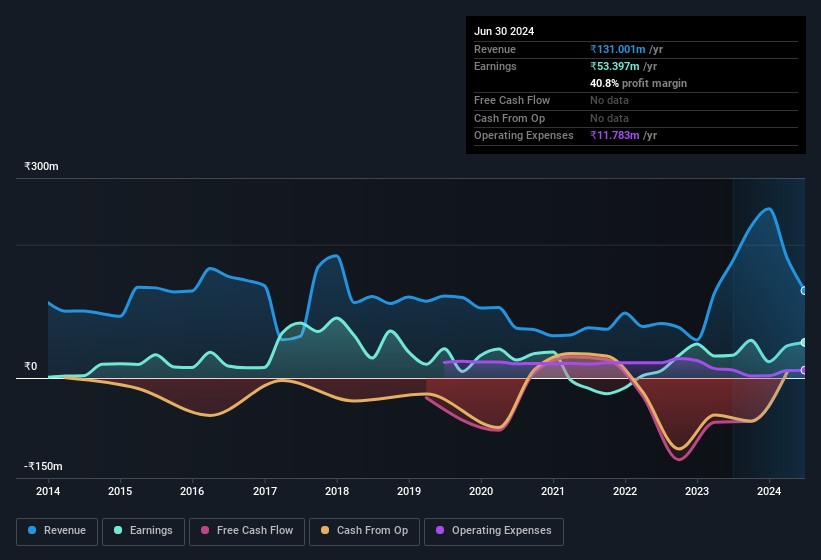

Over the last three years, Tainwala Chemicals and Plastics (India) has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. So it would be better to isolate the growth rate over the last year for our analysis. Tainwala Chemicals and Plastics (India)'s EPS shot up from ₹3.61 to ₹5.70; a result that's bound to keep shareholders happy. That's a fantastic gain of 58%.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. Unfortunately, Tainwala Chemicals and Plastics (India)'s revenue dropped 25% last year, but the silver lining is that EBIT margins improved from -33% to -1.5%. That's not a good look.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

Since Tainwala Chemicals and Plastics (India) is no giant, with a market capitalisation of ₹2.6b, you should definitely check its cash and debt before getting too excited about its prospects.

Are Tainwala Chemicals and Plastics (India) Insiders Aligned With All Shareholders?

Theory would suggest that it's an encouraging sign to see high insider ownership of a company, since it ties company performance directly to the financial success of its management. So those who are interested in Tainwala Chemicals and Plastics (India) will be delighted to know that insiders have shown their belief, holding a large proportion of the company's shares. To be exact, company insiders hold 53% of the company, so their decisions have a significant impact on their investments. Intuition will tell you this is a good sign because it suggests they will be incentivised to build value for shareholders over the long term. To give you an idea, the value of insiders' holdings in the business are valued at ₹1.4b at the current share price. That should be more than enough to keep them focussed on creating shareholder value!

Should You Add Tainwala Chemicals and Plastics (India) To Your Watchlist?

For growth investors, Tainwala Chemicals and Plastics (India)'s raw rate of earnings growth is a beacon in the night. Further, the high level of insider ownership is impressive and suggests that the management appreciates the EPS growth and has faith in Tainwala Chemicals and Plastics (India)'s continuing strength. On the balance of its merits, solid EPS growth and company insiders who are aligned with the shareholders would indicate a business that is worthy of further research. You should always think about risks though. Case in point, we've spotted 3 warning signs for Tainwala Chemicals and Plastics (India) you should be aware of.

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in IN with promising growth potential and insider confidence.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Tainwala Chemicals and Plastics (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TAINWALCHM

Tainwala Chemicals and Plastics (India)

Engages in the manufacture and sale of extruded plastic sheets in India.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor