Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:OWAIS

Is Owais Metal and Mineral Processing (NSE:OWAIS) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Owais Metal and Mineral Processing Limited (NSE:OWAIS) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Owais Metal and Mineral Processing's Debt?

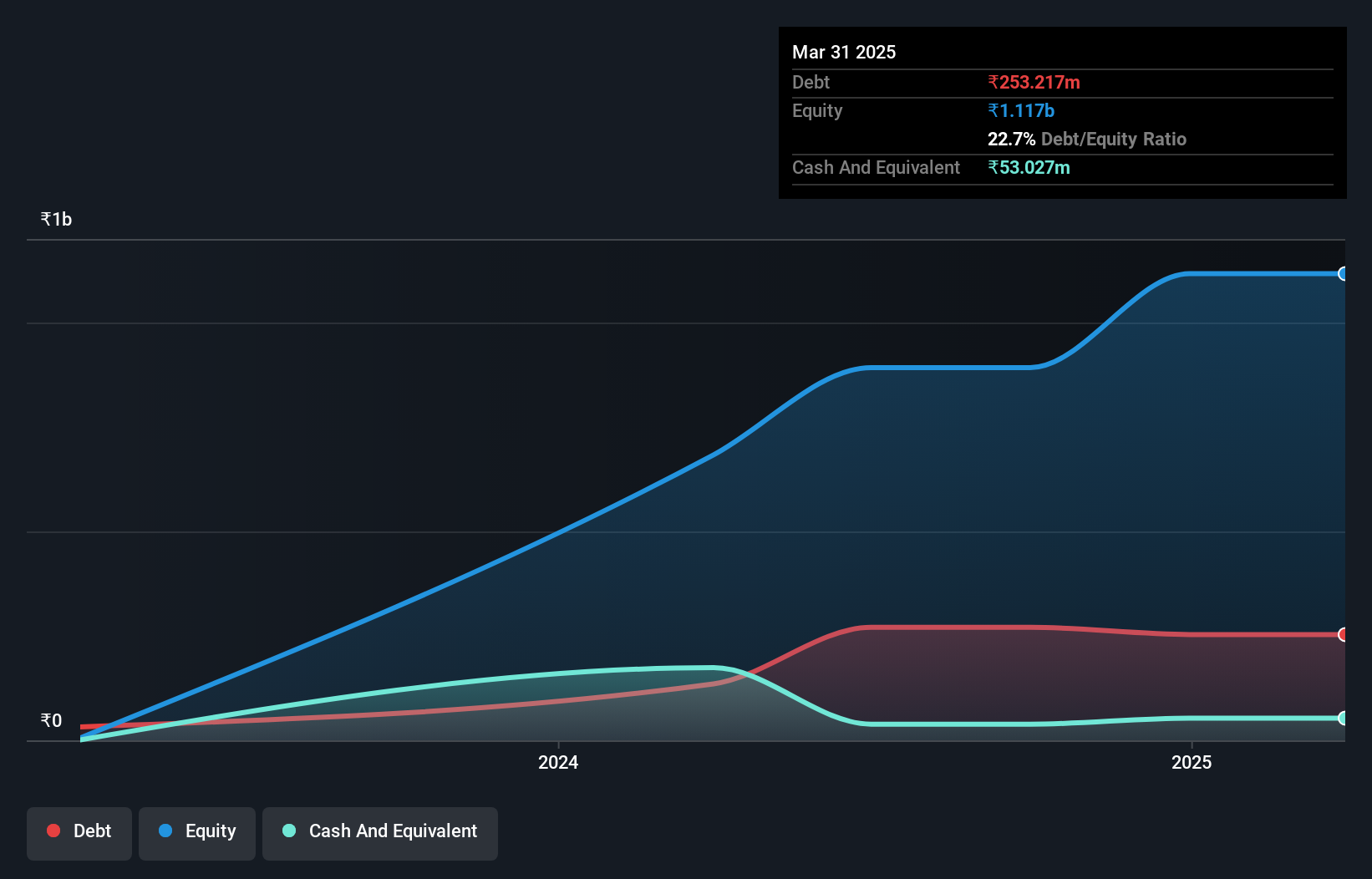

The image below, which you can click on for greater detail, shows that at March 2025 Owais Metal and Mineral Processing had debt of ₹253.2m, up from ₹135.1m in one year. However, because it has a cash reserve of ₹53.0m, its net debt is less, at about ₹200.2m.

How Healthy Is Owais Metal and Mineral Processing's Balance Sheet?

We can see from the most recent balance sheet that Owais Metal and Mineral Processing had liabilities of ₹669.3m falling due within a year, and liabilities of ₹191.9m due beyond that. Offsetting this, it had ₹53.0m in cash and ₹963.6m in receivables that were due within 12 months. So it actually has ₹155.4m more liquid assets than total liabilities.

Having regard to Owais Metal and Mineral Processing's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₹10.1b company is struggling for cash, we still think it's worth monitoring its balance sheet.

View our latest analysis for Owais Metal and Mineral Processing

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Owais Metal and Mineral Processing has a low net debt to EBITDA ratio of only 0.30. And its EBIT covers its interest expense a whopping 38.3 times over. So we're pretty relaxed about its super-conservative use of debt. Better yet, Owais Metal and Mineral Processing grew its EBIT by 196% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Owais Metal and Mineral Processing will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last two years, Owais Metal and Mineral Processing saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Owais Metal and Mineral Processing's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But the stark truth is that we are concerned by its conversion of EBIT to free cash flow. Taking all this data into account, it seems to us that Owais Metal and Mineral Processing takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Owais Metal and Mineral Processing has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:OWAIS

Owais Metal and Mineral Processing

Manufactures, processes, and sells various metals and minerals in India.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor