Advertisement

- India

- /

- Basic Materials

- /

- NSEI:ORIENTCEM

Orient Cement (NSE:ORIENTCEM) Is Paying Out Less In Dividends Than Last Year

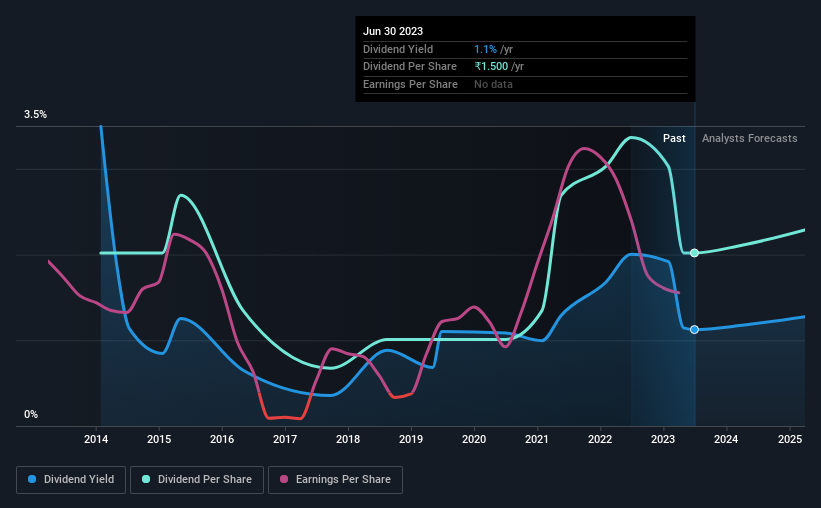

Orient Cement Limited's (NSE:ORIENTCEM) dividend is being reduced from last year's payment covering the same period to ₹1.00 on the 31st of August. The dividend yield of 1.1% is still a nice boost to shareholder returns, despite the cut.

See our latest analysis for Orient Cement

Orient Cement's Earnings Easily Cover The Distributions

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, Orient Cement was earning enough to cover the dividend, but free cash flows weren't positive. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Looking forward, earnings per share is forecast to rise by 122.0% over the next year. If the dividend continues on this path, the payout ratio could be 12% by next year, which we think can be pretty sustainable going forward.

Orient Cement's Dividend Has Lacked Consistency

Orient Cement has been paying dividends for a while, but the track record isn't stellar. This suggests that the dividend might not be the most reliable. The most recent annual payment of ₹1.50 is about the same as the annual payment 9 years ago. We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments the total shareholder return may be limited.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's encouraging to see that Orient Cement has been growing its earnings per share at 23% a year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Our Thoughts On Orient Cement's Dividend

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. While Orient Cement is earning enough to cover the payments, the cash flows are lacking. We don't think Orient Cement is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 2 warning signs for Orient Cement that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ORIENTCEM

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor