Everest Kanto Cylinder Limited's (NSE:EKC) Stock Is Going Strong: Is the Market Following Fundamentals?

Most readers would already be aware that Everest Kanto Cylinder's (NSE:EKC) stock increased significantly by 52% over the past three months. Since the market usually pay for a company’s long-term fundamentals, we decided to study the company’s key performance indicators to see if they could be influencing the market. In this article, we decided to focus on Everest Kanto Cylinder's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Everest Kanto Cylinder

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Everest Kanto Cylinder is:

15% = ₹839m ÷ ₹5.7b (Based on the trailing twelve months to December 2020).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.15 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Everest Kanto Cylinder's Earnings Growth And 15% ROE

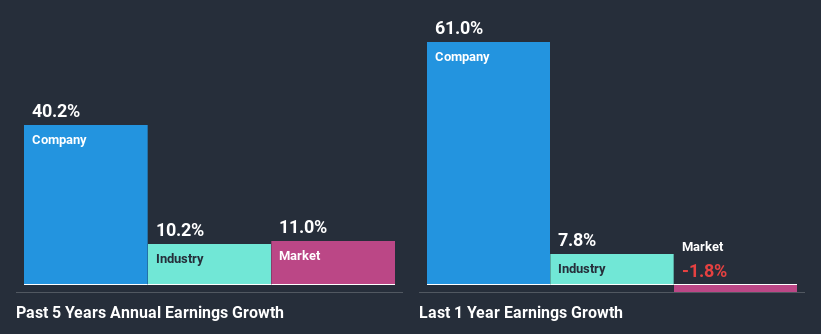

On the face of it, Everest Kanto Cylinder's ROE is not much to talk about. However, the fact that the its ROE is quite higher to the industry average of 10% doesn't go unnoticed by us. Especially when you consider Everest Kanto Cylinder's exceptional 40% net income growth over the past five years. Bear in mind, the company does have a moderately low ROE. It is just that the industry ROE is lower. So, there might well be other reasons for the earnings to grow. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

Next, on comparing with the industry net income growth, we found that Everest Kanto Cylinder's growth is quite high when compared to the industry average growth of 10% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. Is Everest Kanto Cylinder fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Everest Kanto Cylinder Making Efficient Use Of Its Profits?

Everest Kanto Cylinder doesn't pay any dividend to its shareholders, meaning that the company has been reinvesting all of its profits into the business. This is likely what's driving the high earnings growth number discussed above.

Summary

In total, we are pretty happy with Everest Kanto Cylinder's performance. In particular, it's great to see that the company has seen significant growth in its earnings backed by a respectable ROE and a high reinvestment rate. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. You can see the 2 risks we have identified for Everest Kanto Cylinder by visiting our risks dashboard for free on our platform here.

When trading Everest Kanto Cylinder or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Everest Kanto Cylinder might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:EKC

Flawless balance sheet and undervalued.