Advertisement

Is Chambal Fertilisers and Chemicals (NSE:CHAMBLFERT) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Chambal Fertilisers and Chemicals Limited (NSE:CHAMBLFERT) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

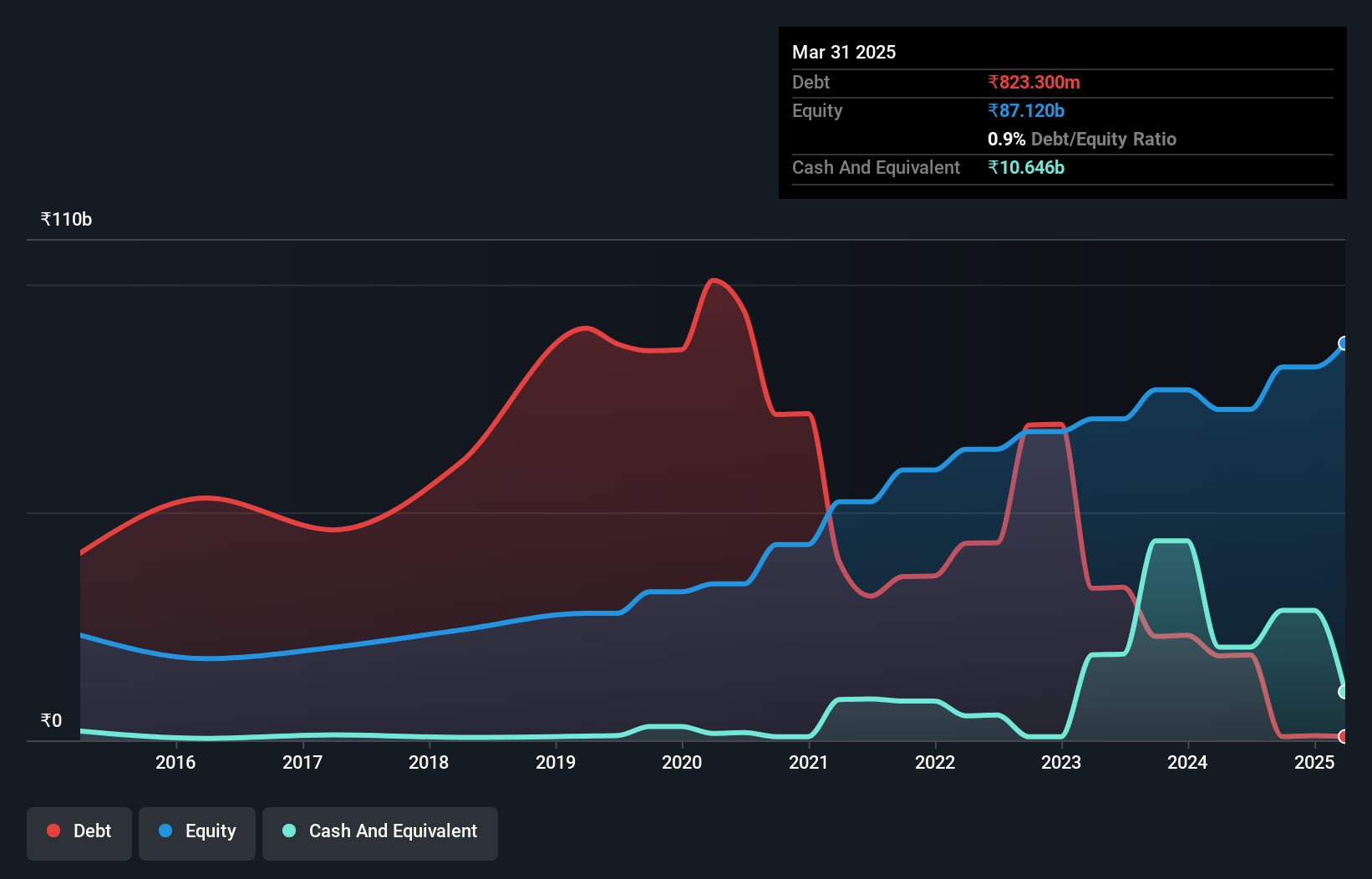

What Is Chambal Fertilisers and Chemicals's Net Debt?

The image below, which you can click on for greater detail, shows that Chambal Fertilisers and Chemicals had debt of ₹823.3m at the end of March 2025, a reduction from ₹18.5b over a year. But on the other hand it also has ₹10.6b in cash, leading to a ₹9.82b net cash position.

How Healthy Is Chambal Fertilisers and Chemicals' Balance Sheet?

We can see from the most recent balance sheet that Chambal Fertilisers and Chemicals had liabilities of ₹11.7b falling due within a year, and liabilities of ₹15.2b due beyond that. Offsetting this, it had ₹10.6b in cash and ₹3.68b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹12.6b.

Since publicly traded Chambal Fertilisers and Chemicals shares are worth a total of ₹220.6b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Chambal Fertilisers and Chemicals also has more cash than debt, so we're pretty confident it can manage its debt safely.

Check out our latest analysis for Chambal Fertilisers and Chemicals

Also positive, Chambal Fertilisers and Chemicals grew its EBIT by 23% in the last year, and that should make it easier to pay down debt, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Chambal Fertilisers and Chemicals's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Chambal Fertilisers and Chemicals has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Chambal Fertilisers and Chemicals actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

We could understand if investors are concerned about Chambal Fertilisers and Chemicals's liabilities, but we can be reassured by the fact it has has net cash of ₹9.82b. And it impressed us with free cash flow of ₹8.2b, being 119% of its EBIT. So we don't think Chambal Fertilisers and Chemicals's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Chambal Fertilisers and Chemicals has 1 warning sign we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CHAMBLFERT

Chambal Fertilisers and Chemicals

Produces and sells fertilizers primarily in India.

Very undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor