Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:BMETRICS

Bombay Metrics Supply Chain Limited's (NSE:BMETRICS) Shares Bounce 50% But Its Business Still Trails The Market

Bombay Metrics Supply Chain Limited (NSE:BMETRICS) shares have had a really impressive month, gaining 50% after a shaky period beforehand. But the last month did very little to improve the 64% share price decline over the last year.

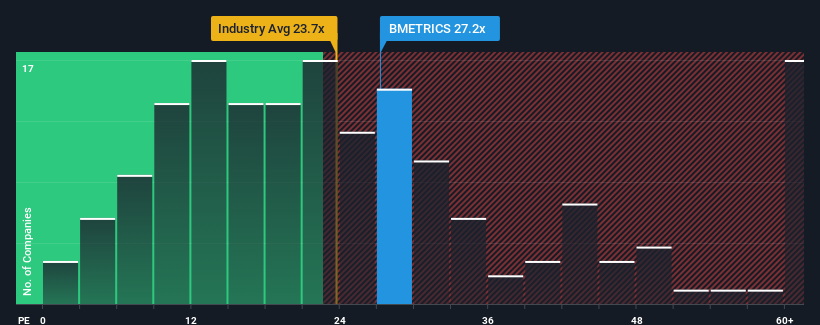

Although its price has surged higher, Bombay Metrics Supply Chain may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 27.2x, since almost half of all companies in India have P/E ratios greater than 31x and even P/E's higher than 59x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

The earnings growth achieved at Bombay Metrics Supply Chain over the last year would be more than acceptable for most companies. One possibility is that the P/E is low because investors think this respectable earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

See our latest analysis for Bombay Metrics Supply Chain

Is There Any Growth For Bombay Metrics Supply Chain?

There's an inherent assumption that a company should underperform the market for P/E ratios like Bombay Metrics Supply Chain's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 22% last year. The strong recent performance means it was also able to grow EPS by 79% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is predicted to deliver 24% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we can see why Bombay Metrics Supply Chain is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Key Takeaway

The latest share price surge wasn't enough to lift Bombay Metrics Supply Chain's P/E close to the market median. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Bombay Metrics Supply Chain revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 3 warning signs for Bombay Metrics Supply Chain (2 are concerning!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Bombay Metrics Supply Chain might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BMETRICS

Bombay Metrics Supply Chain

Together with its subsidiary, Metrics Vietnam Company Limited, provides manufacturing and trading of engineering tools and components, and supply chain management services in India and internationally.

Solid track record with moderate risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor