Advertisement

- India

- /

- Consumer Durables

- /

- NSEI:STOVEKRAFT

Slowing Rates Of Return At Stove Kraft (NSE:STOVEKRAFT) Leave Little Room For Excitement

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. That's why when we briefly looked at Stove Kraft's (NSE:STOVEKRAFT) ROCE trend, we were pretty happy with what we saw.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Stove Kraft:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

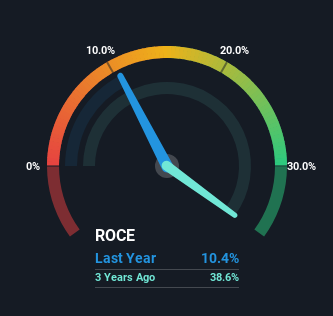

0.10 = ₹558m ÷ (₹11b - ₹5.2b) (Based on the trailing twelve months to December 2023).

Thus, Stove Kraft has an ROCE of 10%. In absolute terms, that's a pretty standard return but compared to the Consumer Durables industry average it falls behind.

Check out our latest analysis for Stove Kraft

In the above chart we have measured Stove Kraft's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Stove Kraft .

How Are Returns Trending?

The trend of ROCE doesn't stand out much, but returns on a whole are decent. The company has employed 244% more capital in the last five years, and the returns on that capital have remained stable at 10%. 10% is a pretty standard return, and it provides some comfort knowing that Stove Kraft has consistently earned this amount. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

One more thing to note, even though ROCE has remained relatively flat over the last five years, the reduction in current liabilities to 49% of total assets, is good to see from a business owner's perspective. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously. We'd like to see this trend continue though because as it stands today, thats still a pretty high level.

The Bottom Line On Stove Kraft's ROCE

The main thing to remember is that Stove Kraft has proven its ability to continually reinvest at respectable rates of return. However, despite the favorable fundamentals, the stock has fallen 24% over the last three years, so there might be an opportunity here for astute investors. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

If you'd like to know more about Stove Kraft, we've spotted 2 warning signs, and 1 of them can't be ignored.

While Stove Kraft may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:STOVEKRAFT

Stove Kraft

Manufactures and trades in kitchen and home appliances in India and internationally.

Reasonable growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|35.9% undervalued

JO

Community Contributor

Occidental Petroleum is set to achieve a 16% profit margin improvement

Fair Value US$55.05|15.6% undervalued

DZ

Community Contributor

Argan's Revenue Set to Soar with a 13.31% Growth in the Coming Decade

Fair Value US$284.68|23.4% undervalued

KE

Community Contributor

EU#1 - From German Startup to EU’s Biggest Company

Fair Value €248.62|2.5% overvalued

TO

Community Contributor