Advertisement

Macpower CNC Machines Limited (NSE:MACPOWER) Stocks Shoot Up 28% But Its P/S Still Looks Reasonable

Despite an already strong run, Macpower CNC Machines Limited (NSE:MACPOWER) shares have been powering on, with a gain of 28% in the last thirty days. The last 30 days were the cherry on top of the stock's 400% gain in the last year, which is nothing short of spectacular.

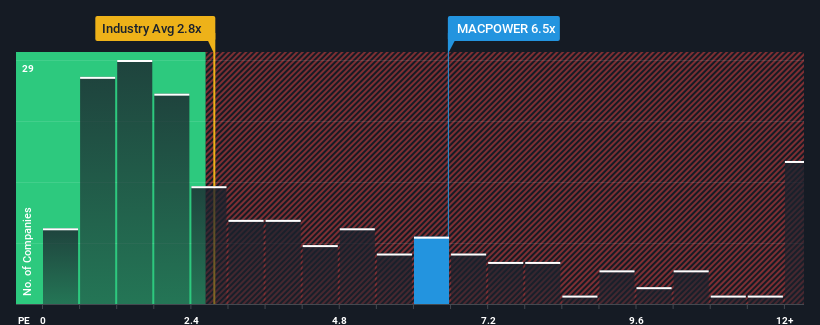

Since its price has surged higher, you could be forgiven for thinking Macpower CNC Machines is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 6.5x, considering almost half the companies in India's Machinery industry have P/S ratios below 2.8x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Macpower CNC Machines

What Does Macpower CNC Machines' Recent Performance Look Like?

Revenue has risen firmly for Macpower CNC Machines recently, which is pleasing to see. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Macpower CNC Machines will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Macpower CNC Machines' is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 173% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 12%, the most recent medium-term revenue trajectory is noticeably more alluring

With this in consideration, it's not hard to understand why Macpower CNC Machines' P/S is high relative to its industry peers. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the wider industry.

What We Can Learn From Macpower CNC Machines' P/S?

Shares in Macpower CNC Machines have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Macpower CNC Machines maintains its high P/S on the strength of its recent three-year growth being higher than the wider industry forecast, as expected. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Macpower CNC Machines with six simple checks will allow you to discover any risks that could be an issue.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MACPOWER

Macpower CNC Machines

Manufactures and sells computer numerical control (CNC) metal cutting machines in India.

Flawless balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor