Stock Analysis

- India

- /

- Electrical

- /

- NSEI:KEI

Does KEI Industries' (NSE:KEI) CEO Salary Compare Well With The Performance Of The Company?

The CEO of KEI Industries Limited (NSE:KEI) is Anil Gupta, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether KEI Industries pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

View our latest analysis for KEI Industries

How Does Total Compensation For Anil Gupta Compare With Other Companies In The Industry?

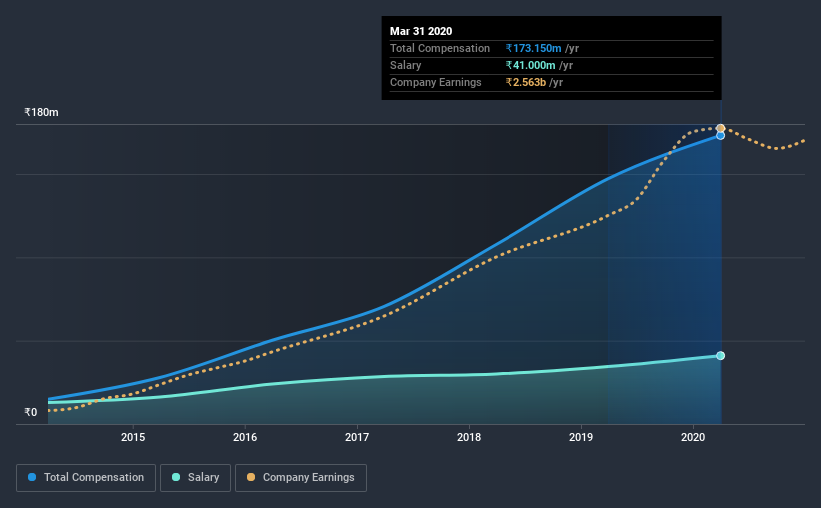

Our data indicates that KEI Industries Limited has a market capitalization of ₹45b, and total annual CEO compensation was reported as ₹173m for the year to March 2020. Notably, that's an increase of 18% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at ₹41m.

For comparison, other companies in the same industry with market capitalizations ranging between ₹29b and ₹116b had a median total CEO compensation of ₹33m. Hence, we can conclude that Anil Gupta is remunerated higher than the industry median. What's more, Anil Gupta holds ₹9.2b worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | ₹41m | ₹35m | 24% |

| Other | ₹132m | ₹113m | 76% |

| Total Compensation | ₹173m | ₹147m | 100% |

Talking in terms of the industry, salary represented approximately 94% of total compensation out of all the companies we analyzed, while other remuneration made up 6.2% of the pie. In KEI Industries' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at KEI Industries Limited's Growth Numbers

KEI Industries Limited has seen its earnings per share (EPS) increase by 14% a year over the past three years. In the last year, its revenue is down 14%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's always a tough situation when revenues are not growing, but ultimately profits are more important. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has KEI Industries Limited Been A Good Investment?

KEI Industries Limited has generated a total shareholder return of 31% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

As previously discussed, Anil is compensated more than what is normal for CEOs of companies of similar size, and which belong to the same industry. However, the EPS growth over three years is certainly impressive. Looking at the same time period, we think that the shareholder returns are respectable. You might wish to research management further, but on this analysis, considering the EPS growth, we wouldn't say CEO compensation problematic.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We've identified 2 warning signs for KEI Industries that investors should be aware of in a dynamic business environment.

Important note: KEI Industries is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

If you decide to trade KEI Industries, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether KEI Industries is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:KEI

Flawless balance sheet with reasonable growth potential.